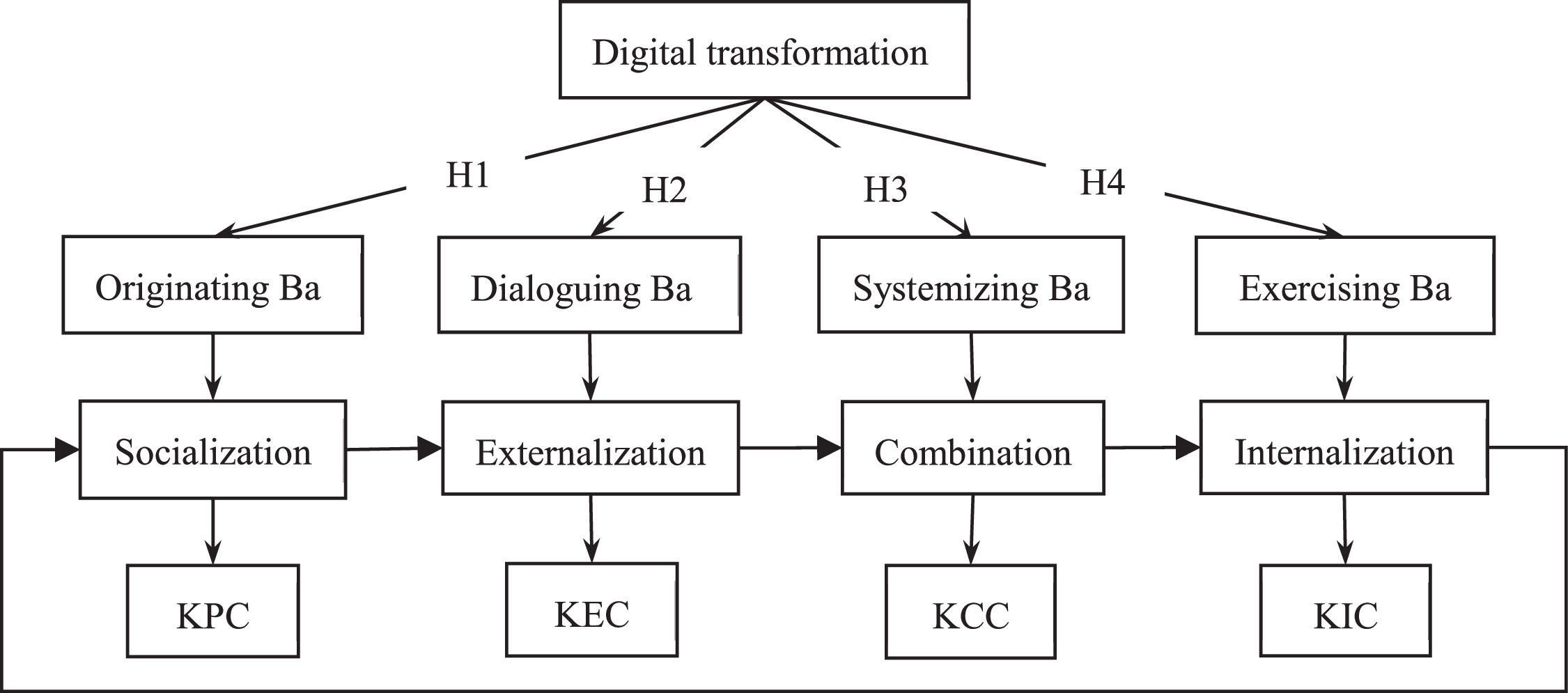

Knowledge creation is the foundation for indigenous innovation in manufacturing enterprises; however, the effects of digital transformation on knowledge creation are still not well understood. Nonaka put forward the model of knowledge creation, which includes four processes: socialization, externalization, combination, and internalization, known as the famous SECI model. Based on the SECI model, this study analyzes the effects of digital transformation on four knowledge creation processes, using panel data from Chinese listed manufacturing enterprises from 2007 to 2020. The study provides several novel findings. First, digital transformation positively affects all knowledge creation processes, with the effects on knowledge combination capability being particularly notable. Second, the effects of digitalization inputs on externalization and combination are insignificant but exert a negative impact on socialization and internalization. Third, a heterogeneity analysis reveals that the facilitating effect of digital transformation is more significant in state-owned and large enterprises. Moreover, it primarily acts as the "cherry on top," significantly benefiting enterprises that already have strong knowledge creation capabilities. A low level of digital technology development in the region where an enterprise is located will inhibit the role of digital transformation in promoting knowledge socialization. Furthermore, enterprise innovation culture and regional innovation environments play positive moderating roles. This study contributes to further understanding of how digital transformation affects enterprises’ knowledge creation activities.

With the rapid development and application of digital technologies, digital transformation has emerged as a key strategy for enterprises to adapt to changes and enhance their competitiveness (Skare & Soriano, 2021; Zaki, 2019). Digital transformation is a process by which digital technology gradually penetrates enterprises, transforms the enterprise operation process comprehensively, and reshapes an enterprise's business model (Appio et al., 2021; Ritter & Pedersen, 2020). Digital transformation is important for enterprises, particularly for those in the manufacturing sector. It not only improves production efficiency and product quality but also drives enterprises toward intelligent manufacturing, thereby maintaining their competitive advantage in the global market (Yang, 2022). Manufacturing enterprises are the main force behind innovation-driven development and the backbone of China's national economy. For Chinese manufacturing enterprises, seizing the opportunities of digital transformation and achieving innovation-driven development are urgent and practical issues.

Previous research has explored the economic consequences of digital transformation in the manufacturing sector, focusing primarily on its effects on productivity, innovation, and performance. For example, Wang and Shao (2024) found that digital transformation has a significant positive impact on the productivity of manufacturing enterprises, while Sui et al. (2024) confirm that digital transformation enhances competitiveness by improving enterprises’ total factor productivity. Digital transformation also promotes investment in innovation activities in manufacturing enterprises (Wen et al., 2022). It enhances both process innovation performance and product innovation performance (Liang & Li, 2022), particularly when combined with servitization (Shen et al., 2021). Scholars have found that digital transformation improves the environmental, social and governance (ESG) responsibility performance (Wang et al., 2023) and sustainable performance (Xu et al., 2023) of manufacturing enterprises. Furthermore, Zhang et al. (2023) found that both exploitative and explorative digital transformation positively affect enterprise performance. As for other outcomes for manufacturing enterprises, current research has explored factors such as labor (Xie et al., 2021), risk-taking levels (Luo et al., 2024), and carbon emissions (Zhou & Liu, 2024). However, limited research has focused on the knowledge creation capabilities of enterprises undergoing digital transformation.

In the era of knowledge economy, knowledge has become a critical resource for enterprises, and knowledge creation has become the foundation for enterprises to improve their indigenous innovation capabilities. As digital technology advances rapidly and becomes widely applied, more enterprises are integrating it into their innovation processes (Sjödin et al., 2023, 2021), transforming how knowledge is created within organizations. Studies have shown that digital technology has altered traditional forms of knowledge, greatly changing its carriers, dissemination, and speed of flow (Cheng et al., 2023). Furthermore, the application of digital technology is gradually changing the work logic of enterprises and significantly affecting activities related to knowledge creation. Previous research has predominantly focused on how digital technology influences enterprise innovation performance, considering knowledge creation activities and capabilities as mediating factors such as knowledge coupling (Tian et al., 2023), knowledge search (Yin & Yu, 2022), knowledge flow (Chen & Kim, 2023), knowledge creation (Bag et al., 2021; Chiu & Lin, 2022), and knowledge absorption capacity (Yang et al., 2023). In addition, some scholars have theoretically elaborated on the role of digital technology in supporting knowledge management (Jarrahi et al., 2023).

However, existing research has paid insufficient attention to how enterprise digital transformation affects knowledge creation, and the exploration of knowledge creation as a dynamic process is scarce. Thus, an in-depth exploration is warranted in the digital era. Therefore, this study aims to address the following research questions: (1) Does enterprise digital transformation positively influence the knowledge creation process? (2) Are there differences in the effects of digital transformation on different processes of knowledge creation? (3) If there are positive effects, do the effects vary for different types of enterprises?

This study's possible marginal contributions to the existing literature focus on several aspects. First, the existing literature lacks sufficient research on the effects of digital transformation on knowledge creation. This study addresses this gap by conceptualizing knowledge creation as a dynamic process based on the SECI model. Knowledge creation capability is decomposed into knowledge perception capability (KPC), knowledge externalization capability (KEC), knowledge combination capability (KCC), and knowledge internalization capability (KIC). Each dimension is quantified to empirically investigate the effects of digital transformation. Second, this study examines the heterogeneity in the relationship between digital transformation and knowledge creation among different enterprises and discusses the roles of enterprise size, ownership nature, industry affiliation, and geographical location in the effects of digital transformation on knowledge creation capabilities. Finally, this study extends the existing literature by analyzing the impact factors of knowledge creation capabilities, such as research and development (R&D) investment, government subsidies, and innovation culture, as well as the interrelationships among different knowledge creation capabilities.

The remainder of this paper is organized as follows. Section 2 presents the literature review and research hypotheses. Section 3 details the research design, including variable measurement and model construction. Section 4 presents the empirical results. Section 5 includes further analysis, encompassing the heterogeneity analysis, and examines the moderating effects of innovation culture and environment. Section 6 discusses conclusions, policy implications, and future research directions.

Literature review and hypothesis developmentLiterature reviewKnowledge creationThe concept of knowledge creation lacks consensus, regarding the definition with scholars offering diverse interpretations. From a capability perspective, Nonaka (1994) has proposed that organizational knowledge creation involves an organization's capability to generate, disseminate, and embody new knowledge within products, services, and systems. Alternatively, some studies suggest that knowledge creation entails the capability to exchange and combine knowledge (Shu et al., 2011). Moreover, research has extended knowledge creation capabilities to specific contexts. For example, Menguc et al. (2013) argued that customer knowledge creation capability refers to a firm's capability to collect, analyze, interpret, and reconstruct customer-related knowledge. From a process perspective, Nonaka has made significant contributions that serve as the theoretical foundation for several studies (Allal-Chérif & Makhlouf, 2016; Bartolacci et al., 2016; Kao & Wu, 2016). Nonaka has described organizational knowledge creation as the mutual transformation between tacit and explicit knowledge at the individual, team, and organizational levels, leading to four forms of knowledge conversion: tacit to tacit (socialization), tacit to explicit (externalization), explicit to explicit (combination), and explicit to tacit (internalization). Collectively, these forms are known as the SECI model, which constitutes the process of knowledge creation.

Knowledge creation requires a shared space, referred to as "Ba". Ba can be physical (e.g., business spaces, studios), virtual (e.g., web conferences, email), psychological (e.g., shared experiences, ideas), or any combination thereof (Nonaka & Konno, 1998). Ba provides a platform and environment for knowledge assets and exploration processes within organizations, manifesting in personal interactions, project teams, ad hoc meetings, emails, online conferences, and real-world interactions with customers. In the SECI model, each knowledge creation process corresponds to a Ba (Nonaka et al., 2000).

The originating Ba serves as a venue for fostering socialization with tacit knowledge, which involves the flow and transformation of tacit knowledge among knowledge entities. Owing to the difficulty in formalizing tacit knowledge and the frequent need for specific spaces, it is typically acquired through shared experiences or interactions, such as apprentices gaining tacit knowledge through firsthand experience working with a master craftsperson. During such interactions, the shared environment of spending time or living together initiates the Ba. Dialoguing Ba functions as a platform for promoting the externalization of tacit knowledge. Externalization is the process of embodying tacit knowledge through tangible expressions, which individuals utilize their linguistic consciousness to rationalize and articulate their surroundings, often encoding them, such as through language, text, or symbols. In this context, Ba represents a virtual interaction space, whether it involves self-dialogue or dialogue with others. Systematizing Ba serves as a venue for achieving the combination of explicit knowledge. Combination involves integrating existing explicit knowledge from both internal and external sources and then re-editing and processing it to generate new systematic explicit knowledge. The creative utilization of computer communication networks and large-scale databases can facilitate this knowledge transformation process. In this scenario, the environment in which employees utilize databases becomes a systematizing Ba. Finally, exercising Ba supports knowledge internalization, which is the process of absorbing and understanding explicit knowledge and transforming it into new tacit knowledge. The environment in which employees learn and apply knowledge during this process can be referred to as an exercising Ba.

Digital transformation and knowledge creationThe influence of technology on knowledge creation has long been a subject of interest to researchers. Baba and Nobeoka (1998) found that the utilization of 3D CAD systems could enhance the deductive, inductive, and retrospective processes of engineers and organizations, thereby improving their knowledge creation capabilities. Similarly, Kaschig et al. (2016) discovered that information technology support can facilitate organizational knowledge collection and knowledge linking activities, thereby promoting knowledge creation. These findings highlight the supportive role of information technology. Additionally, some scholars have analyzed the differentiated effects of technology or systems on knowledge creation (Arling & Chun, 2011; Tyagi et al., 2015). However, digital transformation encompasses more than the application of digital technology alone. It also involves significant changes in management, business models, organizational structures, business processes, and production factors. Consequently, further research has shown that the extensive enabling technologies brought about by enterprise digital transformation enhance enterprises’ capabilities in identifying, acquiring, and utilizing complex information and knowledge, thereby creating new learning opportunities for businesses (Hullova et al., 2016; Wang & Hitch, 2017). Moreover, it enables the proactive search and utilization of external knowledge, thereby preventing enterprises from falling into knowledge lock-in traps and cognitive redundancies (Buciuni & Pisano, 2018) and accelerating the processes of knowledge creation and accumulation.

Although some research exists on the relationship between digital transformation and knowledge creation, further exploration is required from several perspectives. First, the research on how digital transformation affects knowledge creation is not systematic enough. Current studies often focus on singular knowledge activities without considering knowledge creation as a process. Thus, they fail to fully investigate how digital transformation affects this process and its effectiveness during different processes. Second, existing research has not included a sufficiently deep exploration of contexts and their elements in relation to the effects of digital transformation on knowledge creation, which requires further explanation of how different conditions affect various knowledge creation processes. Therefore, this study adopts a capability perspective corresponding to the SECI model, in which the four processes are equated with four capabilities: KPC, KEC, KCC, and KIC. It explores the relationships between digital transformation and these capabilities, as well as the heterogeneity under different conditions.

Hypothesis developmentDigital transformation and KPCEnterprises require a significant amount of external tacit knowledge to meet their internal knowledge conversion requirements (Ryu et al., 2022). Digital transformation blurs the traditional boundaries of knowledge creation, creating a more multidimensional and interactive network of knowledge creators for enterprises, and incorporating consumers, competitors, and collaborators into the enterprise socialization process (Guo et al., 2021; Liu & Hansen, 2022). The originating Ba provides a favorable environment for facilitating the effective flow of tacit knowledge, which has traditionally been believed to require knowledge entities to share the same time and place to experience and perceive tacit knowledge collectively. However, the formation of knowledge-creator networks alleviates temporospatial constraints on the originating Ba, thus expanding its coverage. Within this scope, companies can actively or passively acquire valuable tacit knowledge, facilitate its effective flow, and further enhance their KPC. However, digital transformation may also weaken interpersonal relationships. Compared to in the past, when employees relied on interpersonal relationships and traditional communication methods to solve problems or obtain information, modern employees are more dependent on technology and tools for work. This reduces opportunities for face-to-face communication and interaction and for collaboration among employees. The weakening of traditional face-to-face interactions may hinder the flow of tacit knowledge that originates from Ba functionalities.

H1a

Digital transformation has a significant positive effect on enterprises’ KPC.

H1b

Digital transformation has a negative effect on enterprises’ KPC.

Digital transformation and KECWith the wide application of digital technology, information and knowledge can coexist in digital form, which further strengthens the coexistence of data and tacit knowledge. Therefore, tools that promote data collation, knowledge identification, and the successful transformation of tacit knowledge into explicit knowledge have become key support factors for externalization. In this context, digital transformation provides a more intelligent externalization means in the dialoguing Ba. Using digital technology and various algorithms, enterprises can efficiently integrate, mine, and analyze massive amounts of data, effectively transform data into information; and facilitate the evolution of information into knowledge. Digital transformation enhances data availability, opens new possibilities for the transformation of tacit knowledge to explicit knowledge, and ultimately improves enterprises’ KEC. However, with the advancement of digital transformation, companies may generate large amounts of similar or redundant information, particularly in the generation of large-scale data and automated processes. This homogenized information content may make it difficult for employees to differentiate and identify valuable knowledge, as a significant portion of the information may be repetitive, ineffective, or outdated, rather than genuinely innovative and valuable knowledge. If employees wish to externalize valuable knowledge, they need to continually reflect, sift through, and organize vast amounts of information in the dialogue Ba, thereby hindering knowledge externalization.

H2a

Digital transformation has a significant positive effect on enterprises’ KEC.

H2b

Digital transformation has a negative effect on enterprises’ KEC.

Digital transformation and KCCThe knowledge repository of an enterprise is no longer a simple collection of its knowledge elements (Guan & Liu, 2016), but a special social network composed of knowledge elements as nodes and the coupling relationship between knowledge elements as connections, called a knowledge network (Schillebeeckx et al., 2020). In essence, an enterprise knowledge repository is a knowledge network that captures the commonalities of the technical topics of different knowledge elements, providing guidance for the recombination of potential knowledge elements. The digital transformation of enterprises strengthens the force of systematizing Ba by building a more intelligent and efficient knowledge base. Explicit knowledge can be transmitted to various knowledge creators within the enterprise in a timely manner to realize the flow. Simultaneously, it can quickly respond to and integrate existing knowledge, reduce knowledge islands, tap the potential for re-combination among knowledge elements, to open new opportunities to use explicit knowledge. Overall, enterprise digital transformation has improved the capability of knowledge resource management and KCC. From another perspective, digital transformation often results in a vast amount of knowledge being digitized and stored; however, this knowledge is often fragmented and dispersed across different systems, platforms, and applications. This fragmentation may make it difficult for employees to access and utilize knowledge when needed, requiring them to spend more time and effort searching for and integrating relevant information in systematic Ba, rather than accessing the required content directly from a cohesive and comprehensive knowledge system. Consequently, this may have a negative impact on an organization's knowledge integration capabilities.

H3a

Digital transformation has a significant positive effect on enterprises’ KCC.

H3b

Digital transformation has a negative effect on enterprises’ KCC.

Digital transformation and KICDigital transformation provides a favorable exercising Ba for organizational members. Learning is an important internalization process. Digital transformation optimizes the business process of human resources and promotes the formation of enterprise learning mechanisms through digital technology; thus, employees can easily perform autonomous or organized learning activities from internal and external communication networks and both enterprise and inter-organizational knowledge bases (Lartey et al., 2021). Simultaneously, because knowledge is decomposable and reconfigurable, digital transformation diversifies the carriers and forms of knowledge, thereby further reducing the learning threshold. Practice is also an important means of promoting internalization. Applying digital twins and other technologies expands the exercising Ba from the limited real world to a broader virtual world. This transformation significantly decreases the trial-and-error costs of internalization, lowers obstacles to understanding and absorbing knowledge, promotes the transformation of explicit knowledge to tacit knowledge, and further enhances enterprises’ KIC. Knowledge internalization necessitates those specific contexts and backgrounds be considered; however, technology may constrain employees' opportunities to acquire knowledge in real-life situations. For example, although online courses or video conferences offer abundant knowledge, employees often fail to fully simulate real work scenarios and interactive contexts. Consequently, employees may be unable to apply, and experience learned knowledge in authentic work environments, which will constrain knowledge internalization process.

H4a

Digital transformation has a significant positive effect on enterprises’ KIC.

H4b

Digital transformation has a negative effect on enterprises’ KIC.

According to the above theoretical derivation and hypotheses, this study develops the research framework shown in Fig. 1.

Methods and dataModel setting

This study examines the effects of digital transformation on enterprises’ knowledge creation capabilities and reveals the mechanism and characteristics of its influence on knowledge creation. Combined with the above theoretical analysis, this study constructs the following measurement model to verify the effect of digital transformation on enterprises’ knowledge creation capabilities:

Where, capabilityit denotes the knowledge creation capability of enterprise i in year t, subdivided into KPC, KEC, KCC and KIC. DIGit denotes the degree of digital transformation of enterprise i in year t. Z is the set of control variables, including age, size, governance, human capital, capital structure, management cost, profitability, current ratio, market demand, technical level, and industry competitive intensity; α and β are coefficients and coefficient vectors to be estimated. η is the fixed effect, including firm, year, and province, and εit is a random disturbance term.

Variable selection and indicator measurementDigital transformationMost studies employ text analysis methods that involve extracting digitally related keywords from annual company reports and generating indicators to measure enterprise digital transformation based on the frequency of these keywords (Cheng et al., 2024a; Leng & Zhang, 2024; Zhao, 2024). Text analysis methods leverage machine learning to explore the level of digital development within an enterprise. Among the existing methods for measuring digital transformation, text analysis is better suited for measuring the degree of digital transformation at the enterprise level. However, annual reports may have problems such as false advertising and selective disclosure, potentially leading to bias when relying solely on word frequencies from annual reports. This study considers enterprise digital transformation to be a systematic process involving the comprehensive integration of various elements with digital technologies at a deep level. Furthermore, it encompasses multiple aspects of enterprise production and operation. Drawing on previous research (Chen et al., 2024; Hou & Yang, 2024), this study constructs a framework for indicators of enterprise digital transformation from four aspects and calculates the enterprise digital transformation level using principal component analysis.

(1) The digitalization strategy (DIG_S) reflects a company's operational concept and strategic intent regarding digital transformation. The keywords and expressions used in annual reports are important indicators of a company's operational development direction (Sun, 2024; Sui et al., 2024); therefore, this study utilizes Python to analyze the text of the management analysis and discussion sections in the annual reports of listed companies, counting the frequencies of keywords such as artificial intelligence, big data, cloud computing, the Internet of Things, blockchain, and digital technology applications. To eliminate the influence of the length of the annual report, the proportion of word frequencies is used to measure the degree of the enterprise's digitalization strategy. (2) Digitalization input (DIG_I) reflects an enterprise's actual digital technology inputs, measured by the proportion of the amount related to digital transformation in the detail on intangible assets at the end of the year to the total amount of intangible assets (Jiang et al., 2022). Specifically, when the details on intangible assets include keywords such as "software," "network," "client," "management system," or "intelligent platform,", the item is classified as "intangible assets of digital technology." (3) The key steps in enterprise digital transformation require strong leadership (Montero Guerra et al., 2023); thus, whether positions such as "Chief Information Officer" or "Data Center Manager" have been established within the executive team of a listed company serves as a measure of the level of digitalization management in the enterprise (DIG_M). (4) Digitalization application (DIG_A) reflects the actual use of digital technology within enterprises. Patents filed by enterprises often indicate the potential application in further production and manufacturing processes (Liu et al., 2021; Wang, 2023). Therefore, for each patent filed by an enterprise, a value of 1 is assigned if digital technology-related keywords are present in its text. These values are then summed up to evaluate the overall digitalization application level.

Knowledge perception capabilityKPC focuses on the capability of knowledge creators to receive tacit knowledge effectively. Therefore, in the socialization process, an enterprise's perception of new knowledge and its own knowledge base are important factors (Dufva & Ahiqvist, 2015). The mental model of the knowledge creator shapes this perception. R&D personnel, as core innovators, possess high knowledge-processing capabilities, keen understanding, and are receptive to new knowledge, which makes them more likely to share and enrich tacit knowledge (Chen et al., 2024). An enterprise's knowledge base reflects the field and scope of knowledge that it can understand, which is determined by its breadth of knowledge (KB) and depth of knowledge (KD) (Farazi et al., 2019). Therefore, this study argues that the collaborative interaction between R&D personnel and knowledge base jointly shapes enterprises’ KPC. The specific calculation method is as follow:

Where, RDp represents the normalized number of internal R&D personnel in the enterprise. The enterprise knowledge base is calculated using patent data, based on the existing literature (Shi et al., 2023; Zhou & Li, 2012). KB is measured using the information entropy index, where greater entropy reflects a larger volume of information within the system, indicating that an enterprise covers a wider range of knowledge domains (Krafft et al., 2011). Here, k represents the IPC (4-digit) subclass, N denotes the number of IPC (4-digit) subclasses, and fikt represents the proportion of patents in subclass k out of the total patents applied for in a given year. KD is calculated using the Herfindahl index; a higher index indicates greater concentration, implying a higher degree of mastery over the core knowledge domain. Pit represents the number of patents for enterprise i belonging to subclass k in year t.

Knowledge externalization capabilityKEC denotes an organization's proficiency in effectively transforming tacit knowledge into explicit knowledge. Explicit knowledge takes the form of structured knowledge that can be objectively stored within organizations, including manuals, regulations, patents, and papers. Among these, patents represent tangible knowledge outcomes that exhibit both high quality and value characteristics. They serve as valuable indicators of an organization's capacity to externalize knowledge. Furthermore, patents offer quantifiable and comparable measures, making them suitable for analysis. Therefore, considering the results of knowledge externalization, this study uses the logarithm of the number of patents applied for by the enterprise each year as the measurement. The larger the value, the stronger the KEC.

Knowledge combination capabilityKCC represents an organization's competence in systemizing and generating explicit knowledge. In this study, we adopt a knowledge element perspective by leveraging social network theory (Lin et al., 2022). Specifically, the IPC (4-digit) subclass is employed to reflect the co-occurrence relationship between knowledge elements within the same patent; thus, a comprehensive knowledge element network for enterprises can be constructed (Zakaryan, 2023). Within the knowledge element network, edges symbolize connections between knowledge elements, and the overall number of edges indicates the total connections across the network. A higher number of edges signifies greater utilization of knowledge element combinations by the company, implying a more profound integration experience with diverse types of explicit knowledge and, consequently, heightened KCC. To account for the effect of scale, this weighted approach is applied to the number of edges by utilizing the following formula:

Where, Nit represents the number of knowledge element categories that company i possesses in year t. Vit represents the number of isolated nodes in the knowledge element network. Lit represents the actual number of associations between the various knowledge elements generated by company i in year t.

Knowledge internalization capabilityKIC represents an organization's aptitude to learn from explicit knowledge and comprehend the underlying valuable tacit knowledge, ultimately leading to the generation of new tacit knowledge. Given the inherent challenge of objectively measuring tacit knowledge, this study adopted an extrapolation approach from explicit knowledge to assess the extent of an organization's tacit knowledge absorption and generation. When an organization genuinely comprehends and assimilates new tacit knowledge, this is highly likely to manifest as future explicit knowledge outcomes. From a knowledge element perspective, this implies that the more knowledge elements an organization employs, the deeper its comprehension of past explicit knowledge. Consequently, this study uses the logarithm of the number of IPC (4-digit) subclasses in the invention patents of an enterprise for the next three years as a proxy variable for the organization's KIC.

Control variablesTo eliminate interference, this study selects the following control variables: company age (Age), calculated using the year the company was listed; company size (Size), measured as the natural logarithm of the total assets of the company at year-end; human capital (HR), measured by the natural logarithm of the number of employees in the company plus one; capital structure (Capital), measured by the proportion of the company's liabilities to total assets at year-end; management costs (Mcost), measured by the proportion of management expenses to a company's main operating income; current ratio (CR), measured by the proportion of current assets to total assets at year-end; profitability (Roa), measured by the company's proportion of net profits to total assets; market demand (MD), measured by the natural logarithm of a company's main operating income. Other control variables include technological level (TL), which is measured using the difference between the total factor productivity calculated using the LP method for the company and industry average because technologically advanced companies are more likely to be high-productivity enterprises. Enterprise governance level (Governance) is assessed referring to previous research (Cheng et al., 2024; Miloud, 2024), and principal component analysis method is used to select basic indicators to measure enterprise governance levels, including executive compensation as a proportion of executive shareholding, proportion of independent directors, board size, proportion of institutional shareholding, ownership balance (sum of the shareholding proportions of the second to fifth largest shareholders divided by the shareholding proportion of the controlling shareholder), and whether the board chairperson and CEO roles are combined. Finally, the industry competitive intensity (Competition) is measured as the difference between 1 and the Herfindahl index calculated using total equity.

Data sourcesThis study uses data from Chinese A-share listed companies on the Shanghai and Shenzhen Stock Exchanges from 2007 to 2020 as an initial sample to investigate the impact of enterprise digital transformation on knowledge creation capability. Patent-related data are sourced from the Incopat database, whereas financial data are primarily sourced from the CSMAR database. Data on digital transformation and internal enterprise innovation culture are collected manually from the annual reports of listed companies. Regional and industry-related data are sourced from the China Statistical Yearbook, China Science and Technology Statistical Yearbook, and China High-Tech Industry Statistical Yearbook. The Urban Entrepreneurship and Innovation Index is sourced from Peking University's Open Research Data Platform. Subsequently, this study excludes samples of companies with abnormal operations such as ST status, and those samples with missing key variables. Additionally, bilateral 1 % trimming was applied to some continuous variables, resulting in a final dataset comprising 24,104 observations.

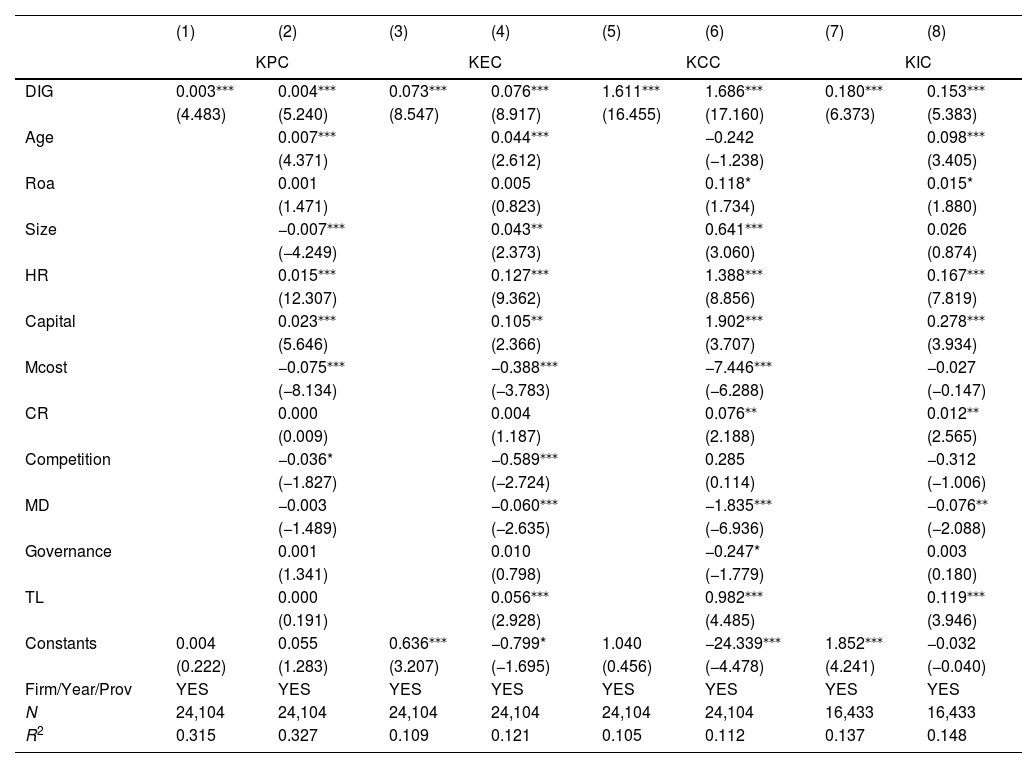

Analysis of empirical resultsBenchmark regression resultsTable 1 presents the baseline regression results. Controlling for firm-, year-, and region-fixed effects, Columns (1)–(8) reports the results on the effects of digital transformation on KPC, KEC, KCC, and KIC. The results indicate that regardless of whether control variables are included, the regression coefficients for digital transformation are significant at the 1 % level. In economic terms, a 1-percentage-point increase in the degree of digital transformation will lead to a 0.004 increase in KPC, representing an approximately 6.78 % increase relative to the sample period mean (0.004/0.059×100 %); a 0.076 increase in KEC, representing an approximately 6.99 % increase relative to the sample period mean (0.076/1.088×100 %); a roughly 1.686 increase in KCC, representing approximately a 34.25 % increase relative to the sample period mean (1.686/4.923×100 %); and a 0.153 increase in KIC, representing approximately a 6.95 % increase relative to the sample period mean (0.153/2.206×100 %). This demonstrates that the effects of digital transformation on KPC, KEC, KCC, and KIC are significantly positive, confirming that digital transformation enhances various aspects of knowledge creation capabilities, thus supporting Hypotheses 1a, 2a, 3a, and 4a. The more pronounced facilitating effect of digital transformation on KCC than on KPC, KIC, or KEC.

The effects of enterprises' degree of digital transformation on knowledge creation capabilities.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | |||||

| DIG | 0.003⁎⁎⁎ | 0.004⁎⁎⁎ | 0.073⁎⁎⁎ | 0.076⁎⁎⁎ | 1.611⁎⁎⁎ | 1.686⁎⁎⁎ | 0.180⁎⁎⁎ | 0.153⁎⁎⁎ |

| (4.483) | (5.240) | (8.547) | (8.917) | (16.455) | (17.160) | (6.373) | (5.383) | |

| Age | 0.007⁎⁎⁎ | 0.044⁎⁎⁎ | −0.242 | 0.098⁎⁎⁎ | ||||

| (4.371) | (2.612) | (−1.238) | (3.405) | |||||

| Roa | 0.001 | 0.005 | 0.118* | 0.015* | ||||

| (1.471) | (0.823) | (1.734) | (1.880) | |||||

| Size | −0.007⁎⁎⁎ | 0.043⁎⁎ | 0.641⁎⁎⁎ | 0.026 | ||||

| (−4.249) | (2.373) | (3.060) | (0.874) | |||||

| HR | 0.015⁎⁎⁎ | 0.127⁎⁎⁎ | 1.388⁎⁎⁎ | 0.167⁎⁎⁎ | ||||

| (12.307) | (9.362) | (8.856) | (7.819) | |||||

| Capital | 0.023⁎⁎⁎ | 0.105⁎⁎ | 1.902⁎⁎⁎ | 0.278⁎⁎⁎ | ||||

| (5.646) | (2.366) | (3.707) | (3.934) | |||||

| Mcost | −0.075⁎⁎⁎ | −0.388⁎⁎⁎ | −7.446⁎⁎⁎ | −0.027 | ||||

| (−8.134) | (−3.783) | (−6.288) | (−0.147) | |||||

| CR | 0.000 | 0.004 | 0.076⁎⁎ | 0.012⁎⁎ | ||||

| (0.009) | (1.187) | (2.188) | (2.565) | |||||

| Competition | −0.036* | −0.589⁎⁎⁎ | 0.285 | −0.312 | ||||

| (−1.827) | (−2.724) | (0.114) | (−1.006) | |||||

| MD | −0.003 | −0.060⁎⁎⁎ | −1.835⁎⁎⁎ | −0.076⁎⁎ | ||||

| (−1.489) | (−2.635) | (−6.936) | (−2.088) | |||||

| Governance | 0.001 | 0.010 | −0.247* | 0.003 | ||||

| (1.341) | (0.798) | (−1.779) | (0.180) | |||||

| TL | 0.000 | 0.056⁎⁎⁎ | 0.982⁎⁎⁎ | 0.119⁎⁎⁎ | ||||

| (0.191) | (2.928) | (4.485) | (3.946) | |||||

| Constants | 0.004 | 0.055 | 0.636⁎⁎⁎ | −0.799* | 1.040 | −24.339⁎⁎⁎ | 1.852⁎⁎⁎ | −0.032 |

| (0.222) | (1.283) | (3.207) | (−1.695) | (0.456) | (−4.478) | (4.241) | (−0.040) | |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 24,104 | 24,104 | 24,104 | 24,104 | 24,104 | 24,104 | 16,433 | 16,433 |

| R2 | 0.315 | 0.327 | 0.109 | 0.121 | 0.105 | 0.112 | 0.137 | 0.148 |

Note: * p < 0.1, ⁎⁎p < 0.05, ⁎⁎⁎p < 0.01. T statistics are in parentheses. If the remaining tables are not specifically described, they are the same.

This could be attributable to several factors. Explicit knowledge is generally more readily accessible than tacit knowledge, and the advent of intelligent technologies facilitated by digital transformation, such as artificial intelligence and machine learning, further reduces the difficulty in searching for, acquiring, and integrating explicit knowledge. In addition, under the pressure of market competition, enterprises are inclined to integrate their existing internal and external knowledge resources, with limited time and resources to generate new knowledge and thus sustain their competitive advantage.

Robustness checksTo ensure the consistency and stability of the evaluation results, this study complements other empirical methods, such as changing the explanatory variable, replacing the sample selection interval, controlling for the mutual influence between knowledge creation capabilities, and conducting a placebo test.

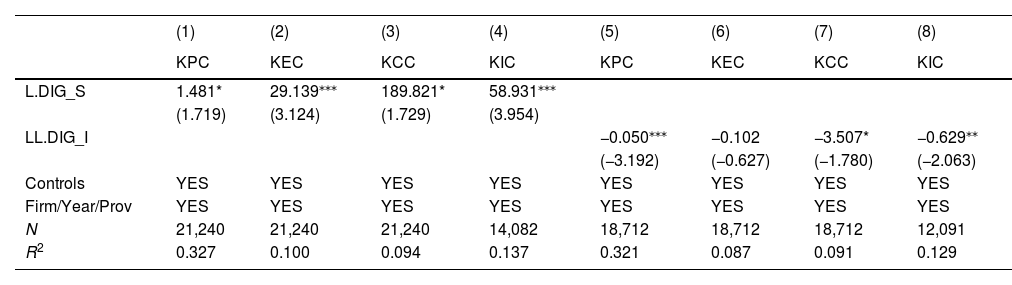

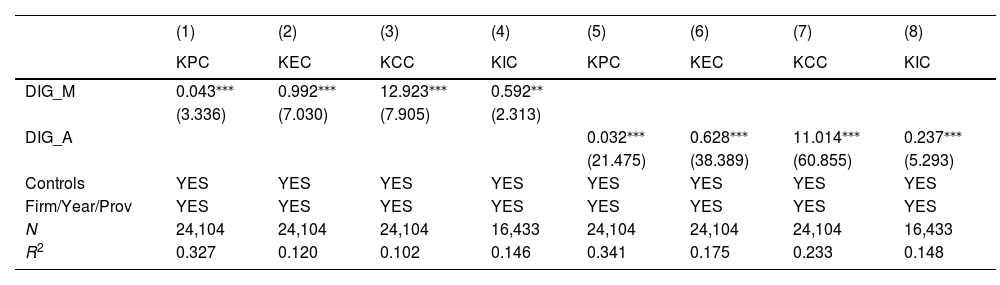

Changing variablesEnterprise digital transformation encompasses multidimensional changes, including digitalization strategy, digitalization input, digitalization management, and digitalization application. This study further examines the impact of key factors in digital transformation on knowledge creation capabilities as a robustness test. The regression results in Table 2 show that digitalization strategy has a promoting effect on knowledge creation capabilities. The regression results in Columns (5)–(8) of Table 2 demonstrate that digitalization input has significant negative effects on KPC and KIC, while its effects on KEC and KCC are not validated. This could be because digital transformation is not a short-term event but rather, requires long-term and sustained investment of key resources, such as funds, technology, and talent (Jia et al., 2024), which may squeeze the resources needed for knowledge creation. Moreover, according to resource dependence theory, excessive digital investment by enterprises may lead to overreliance on technological resources and neglect of other vital resources such as human resources and organizational culture, thereby resulting in a decline in knowledge creation capability. The regression results in Table 3 show that digitalization management and application both have significant positive effects on various knowledge creation capabilities.

The effects of digital strategy and digital investment on knowledge creation capabilities.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| L.DIG_S | 1.481* | 29.139⁎⁎⁎ | 189.821* | 58.931⁎⁎⁎ | ||||

| (1.719) | (3.124) | (1.729) | (3.954) | |||||

| LL.DIG_I | −0.050⁎⁎⁎ | −0.102 | −3.507* | −0.629⁎⁎ | ||||

| (−3.192) | (−0.627) | (−1.780) | (−2.063) | |||||

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 21,240 | 21,240 | 21,240 | 14,082 | 18,712 | 18,712 | 18,712 | 12,091 |

| R2 | 0.327 | 0.100 | 0.094 | 0.137 | 0.321 | 0.087 | 0.091 | 0.129 |

The effects of digital management and application on knowledge creation capabilities.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| DIG_M | 0.043⁎⁎⁎ | 0.992⁎⁎⁎ | 12.923⁎⁎⁎ | 0.592⁎⁎ | ||||

| (3.336) | (7.030) | (7.905) | (2.313) | |||||

| DIG_A | 0.032⁎⁎⁎ | 0.628⁎⁎⁎ | 11.014⁎⁎⁎ | 0.237⁎⁎⁎ | ||||

| (21.475) | (38.389) | (60.855) | (5.293) | |||||

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 24,104 | 24,104 | 24,104 | 16,433 | 24,104 | 24,104 | 24,104 | 16,433 |

| R2 | 0.327 | 0.120 | 0.102 | 0.146 | 0.341 | 0.175 | 0.233 | 0.148 |

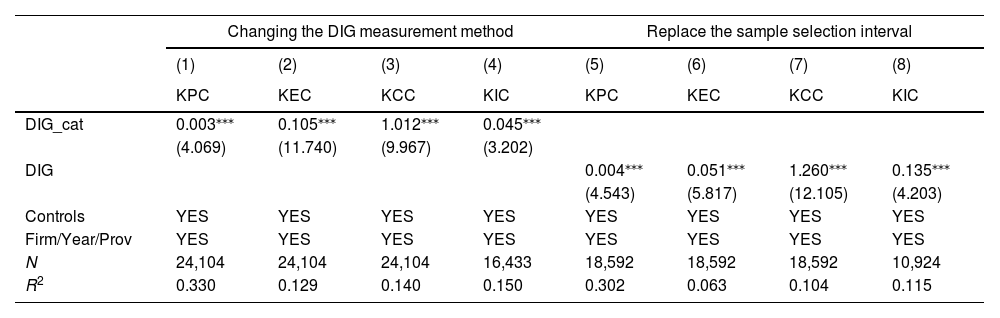

Furthermore, because employing different methods to measure explanatory variables may affect the robustness of the baseline regression results, this study modifies the measurement method for enterprise digital transformation. First, digitalization strategy, digitalization input, digitalization management, and digitalization application are assigned binary values of either 0 or 1. Second, these variables are aggregated into an ordinal multicategorical variable as the measurement indicator for enterprise digital transformation. Columns (1)–(4) of Table 4 replace the explanatory variable measurement methods and repeat the baseline regression tests. The results indicate that the relationship between enterprise digital transformation variables and various aspects of knowledge creation capabilities remains significantly positive. This further demonstrates the robustness of the baseline regression results.

The results of changing the DIG measurement method and replacing the sample selection interval.

| Changing the DIG measurement method | Replace the sample selection interval | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| DIG_cat | 0.003⁎⁎⁎ | 0.105⁎⁎⁎ | 1.012⁎⁎⁎ | 0.045⁎⁎⁎ | ||||

| (4.069) | (11.740) | (9.967) | (3.202) | |||||

| DIG | 0.004⁎⁎⁎ | 0.051⁎⁎⁎ | 1.260⁎⁎⁎ | 0.135⁎⁎⁎ | ||||

| (4.543) | (5.817) | (12.105) | (4.203) | |||||

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 24,104 | 24,104 | 24,104 | 16,433 | 18,592 | 18,592 | 18,592 | 10,924 |

| R2 | 0.330 | 0.129 | 0.140 | 0.150 | 0.302 | 0.063 | 0.104 | 0.115 |

The digital economy in China has experienced rapid development since 2012. Therefore, this study further narrows the sample period to 2012–2020. Table 4 presents the results of the tests conducted after changing the sample selection period, as shown in Columns (5)–(8). Simultaneously, controlling for individual-, year-, and industry- fixed effects, the coefficients of DIG are 0.004, 0.051, 1.260, and 0.135, respectively, and are all significant at the 5 % level, indicating the robustness of this study's conclusions.

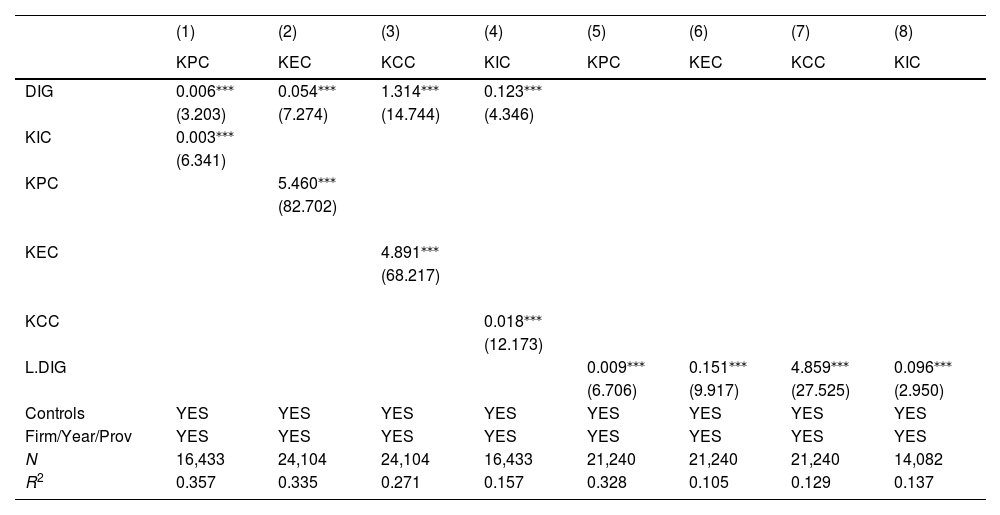

Control the mutual influence between knowledge creation capabilitiesOwing to the close interrelationships among the four knowledge creation processes, to further control for the mutual influences among knowledge creation capabilities, this study includes adjacent knowledge creation variables as control variables in the baseline regression model and conducts sequential tests. Columns (1)–(4) of Table 5 reports the results of these tests, with the regression coefficients for DIG being 0.006, 0.054, 1.314, and 0.123 respectively, all significant at the 1 % level, indicating the robustness of this study's conclusions. Furthermore, the regression coefficients for KIC, KPC, KEC, and KCC, which serve as control variables, are 0.003, 5.460, 4.891, and 0.018, respectively, and all significant at the 1 % level. This further validates that knowledge creation constitutes a cyclical and ongoing process, with significant positive interrelationships among knowledge creation capabilities.

The results of controlling the mutual influence between capabilities and lag processing of DIG.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| DIG | 0.006⁎⁎⁎ | 0.054⁎⁎⁎ | 1.314⁎⁎⁎ | 0.123⁎⁎⁎ | ||||

| (3.203) | (7.274) | (14.744) | (4.346) | |||||

| KIC | 0.003⁎⁎⁎ | |||||||

| (6.341) | ||||||||

| KPC | 5.460⁎⁎⁎ | |||||||

| (82.702) | ||||||||

| KEC | 4.891⁎⁎⁎ | |||||||

| (68.217) | ||||||||

| KCC | 0.018⁎⁎⁎ | |||||||

| (12.173) | ||||||||

| L.DIG | 0.009⁎⁎⁎ | 0.151⁎⁎⁎ | 4.859⁎⁎⁎ | 0.096⁎⁎⁎ | ||||

| (6.706) | (9.917) | (27.525) | (2.950) | |||||

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 16,433 | 24,104 | 24,104 | 16,433 | 21,240 | 21,240 | 21,240 | 14,082 |

| R2 | 0.357 | 0.335 | 0.271 | 0.157 | 0.328 | 0.105 | 0.129 | 0.137 |

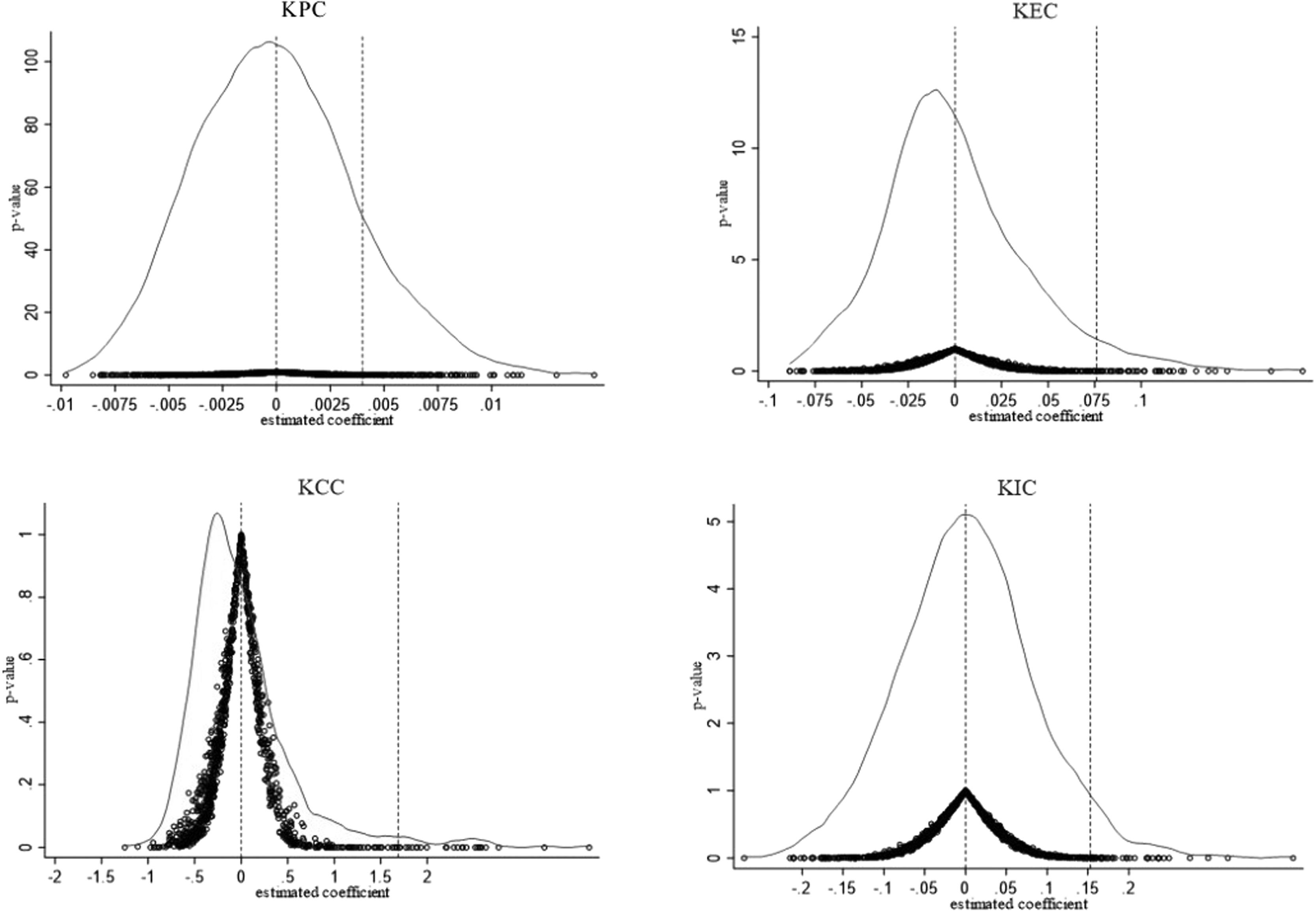

Although the results discussed above control for mutual influences among knowledge creation capabilities, other unobserved potential confounding factors may still exist. Thus, enterprises’ knowledge creation capabilities could potentially be driven by other unobserved factors. This study addresses this possibility by using a placebo test. Fig. 2 shows the results of 1000 placebo tests conducted through random matching. The estimated coefficients of KEC, KCC, and KIC in the baseline regression are all positioned to the right of the 5th percentile of the placebo test coefficient distribution, with values of 0.076 (> 0.072), 2.521 (> 1.119), and 0.153 (> 0.144), respectively. The estimated coefficient of KPC is not to the right of the 5th percentile, but is to the right of the 10th percentile, indicating that the baseline regression results represent a low-probability event in random experiments. Thus, the significant effects of digital transformation on KEC, KCC, and KIC are not demonstrated. Therefore, it can be concluded that the hypothesis of other unobserved potential factors driving knowledge creation capabilities is not supported and that digital transformation indeed enhances enterprises’ knowledge creation capabilities.

Dealing with endogeneity

Endogenous problems in the model, such as measurement errors, reverse causality, sample selection bias, and missing variables, must also be eliminated.

Control reverse causalityEndogeneity, in which explanatory and dependent variables mutually affect each other, is a potential concern in this study. To address this issue, lagged processing and instrumental variable methods are used for further examination.

Lagged Processing: Enterprise digital transformation lagged by one period is used as the core explanatory variable when running the regression again. Since knowledge creation capabilities in the current period cannot influence digital transformation in the previous period, this can partially mitigate the endogeneity issues arising from reverse causality. Columns (5)–(8) of Table 5 reports the regression results using the lagged explanatory variable (L.DIG), which reveals significantly positive regression coefficients.

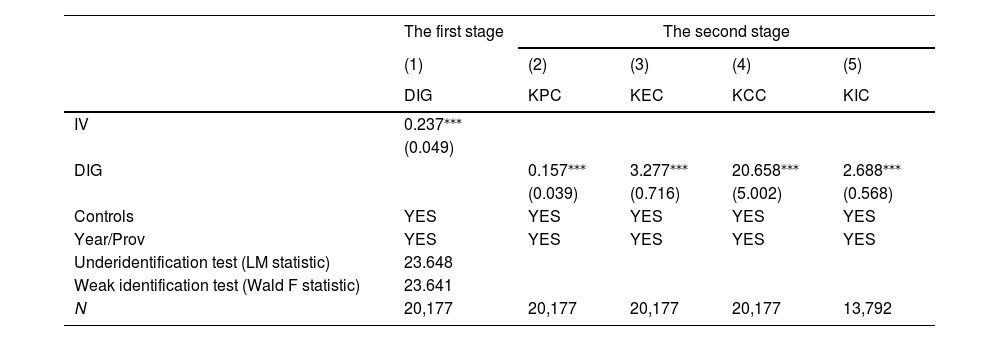

Instrumental Variable Method: The instrumental variable method was employed to overcome the interference of reverse causality. To select instrumental variables, this study refers to Wang (2023), using fixed telephone lines per capita in 1984 as an instrumental variable. However, considering that this variable does not change over time, making it unsuitable as a direct instrumental variable for panel data, the proportion of enterprises undergoing digital transformation in the city where the enterprise is located is introduced. This proportion is multiplied by fixed telephone lines per capita, forming an interaction term as the instrumental variable for enterprise digital transformation. The rationale for this is that digital transformation is a high-risk, high-cost, and complex project. Owing to the high uncertainty of digital transformation, many enterprises seek references from nearby replicable enterprises. Therefore, enterprise digital transformation is influenced by the digital transformation decisions of other local enterprises, which indirectly affect the enterprise's knowledge creation capabilities. Hence, this instrumental variable meets the requirements of relevance and exogeneity. Table 6 reports the instrumental variable regression results obtained using the two-stage least squares method. Column (1) shows that the regression coefficient of the instrumental variable is approximately 0.237, significant at the 1 % level, with no issues of instrumental variable under-identification or a weak instrument. Columns (2)–(5) present the results of the second stage of the instrumental variable regression, where the adjusted DIG regression coefficients are 0.157, 3.277, 20.658, and 2.688 respectively, all significant at the 1 % level. Thus, this study's conclusions remain robust.

The results of using the instrumental variable.

| The first stage | The second stage | ||||

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| DIG | KPC | KEC | KCC | KIC | |

| IV | 0.237⁎⁎⁎ | ||||

| (0.049) | |||||

| DIG | 0.157⁎⁎⁎ | 3.277⁎⁎⁎ | 20.658⁎⁎⁎ | 2.688⁎⁎⁎ | |

| (0.039) | (0.716) | (5.002) | (0.568) | ||

| Controls | YES | YES | YES | YES | YES |

| Year/Prov | YES | YES | YES | YES | YES |

| Underidentification test (LM statistic) | 23.648 | ||||

| Weak identification test (Wald F statistic) | 23.641 | ||||

| N | 20,177 | 20,177 | 20,177 | 20,177 | 13,792 |

Note: * p < 0.1, ⁎⁎p < 0.05, ⁎⁎⁎p < 0.01. Robust standard errors are in parentheses.

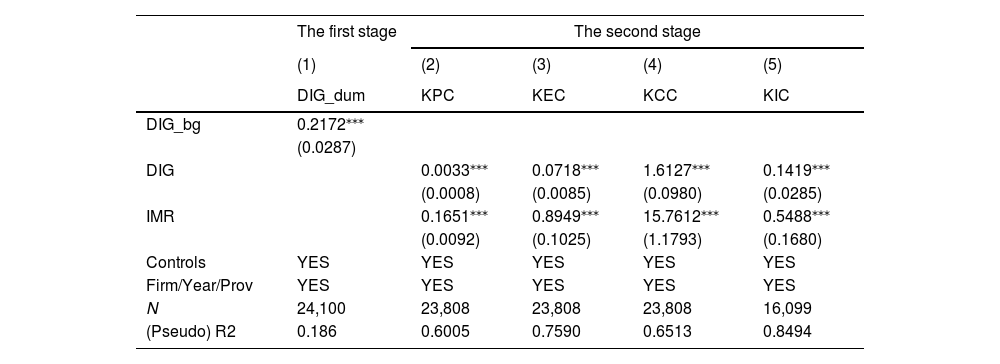

Considering that sample selection bias may also affect the estimation results, this study employs the Heckman two-step method to correct for potential biases. In the first stage, a probit model regression was conducted with a binary variable indicating whether the enterprise has undergone digital transformation (DIG_dum) as the dependent variable. Simultaneously, an exogenous variable, “the digital background of top management” (DIG_bg), is introduced. As enterprise digital transformation requires commitment and support from top management to establish a top-down overall design, the digital background of the top management team is an important factor influencing enterprise digital transformation decisions (Mirza et al., 2024; Müller et al., 2024). The measurement methods are adopted from Cai et al. (2024), using data on the personal characteristics of executive teams in listed companies to assign binary values based on whether the executive team has digital-related educational backgrounds and work experience. In the second stage, the inverse Mills ratio (IMR) is incorporated to correct for sample selection bias, considering the effects of digital transformation on enterprise knowledge creation capabilities after accounting for sample selection bias. Table 7 reports the results. The estimation results in the first stage show that the coefficient of the digital background of the top management team is significant at the 1 % level, indicating that enterprises with management teams that have digital backgrounds are more likely to undergo digital transformation, suggesting the rationality of the selection of the exogenous variable, in line with theoretical expectations. In the second stage, all IMR coefficients are significant and positive, confirming the existence of sample selection bias and validating the use of this method for estimation. After controlling for sample selection bias, the coefficient of enterprise DIG remains significant and positive. This further supports the robustness of the study's findings.

The results of the Heckman two-step method.

| The first stage | The second stage | ||||

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| DIG_dum | KPC | KEC | KCC | KIC | |

| DIG_bg | 0.2172⁎⁎⁎ | ||||

| (0.0287) | |||||

| DIG | 0.0033⁎⁎⁎ | 0.0718⁎⁎⁎ | 1.6127⁎⁎⁎ | 0.1419⁎⁎⁎ | |

| (0.0008) | (0.0085) | (0.0980) | (0.0285) | ||

| IMR | 0.1651⁎⁎⁎ | 0.8949⁎⁎⁎ | 15.7612⁎⁎⁎ | 0.5488⁎⁎⁎ | |

| (0.0092) | (0.1025) | (1.1793) | (0.1680) | ||

| Controls | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES |

| N | 24,100 | 23,808 | 23,808 | 23,808 | 16,099 |

| (Pseudo) R2 | 0.186 | 0.6005 | 0.7590 | 0.6513 | 0.8494 |

Note: * p < 0.1, ⁎⁎p < 0.05, ⁎⁎⁎p < 0.01. Standard errors are in parentheses.

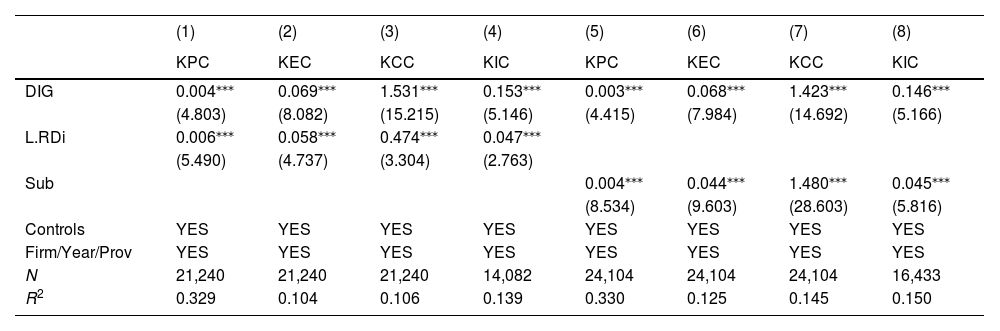

Despite addressing issues such as the measurement bias of core variables, reverse causality, and sample selection bias in the endogeneity tests, the empirical model may still be affected by endogeneity problems due to omitted variable bias. R&D investment provides enterprises with the material foundation and conditions necessary for innovation activities, serving as a crucial support for innovation. Therefore, the lag 1 variable of enterprise R&D investment (L.RDi) was included as the control variable. Table 8 reports the test results in Columns (1)–(4), which show that the regression coefficients of DIG are all significant at the 1 % level. Economic incentives also serve as an important innovation motivation. Governments provide economic incentives that they encourage enterprises to actively engage in innovation activities, thereby enhancing the momentum and enthusiasm for knowledge creation. Thus, considering that the enhancement of enterprise knowledge creation capabilities may be influenced by government intervention, this study includes government subsidies (Sub) as a potentially omitted control variable. Columns (5)–(8) of Table 8 report the results, showing that after incorporating government subsidies, the regression coefficients of DIG remain significant at the 1 % level.

The results of controlling the R&D investment and government subsidies.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| DIG | 0.004⁎⁎⁎ | 0.069⁎⁎⁎ | 1.531⁎⁎⁎ | 0.153⁎⁎⁎ | 0.003⁎⁎⁎ | 0.068⁎⁎⁎ | 1.423⁎⁎⁎ | 0.146⁎⁎⁎ |

| (4.803) | (8.082) | (15.215) | (5.146) | (4.415) | (7.984) | (14.692) | (5.166) | |

| L.RDi | 0.006⁎⁎⁎ | 0.058⁎⁎⁎ | 0.474⁎⁎⁎ | 0.047⁎⁎⁎ | ||||

| (5.490) | (4.737) | (3.304) | (2.763) | |||||

| Sub | 0.004⁎⁎⁎ | 0.044⁎⁎⁎ | 1.480⁎⁎⁎ | 0.045⁎⁎⁎ | ||||

| (8.534) | (9.603) | (28.603) | (5.816) | |||||

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 21,240 | 21,240 | 21,240 | 14,082 | 24,104 | 24,104 | 24,104 | 16,433 |

| R2 | 0.329 | 0.104 | 0.106 | 0.139 | 0.330 | 0.125 | 0.145 | 0.150 |

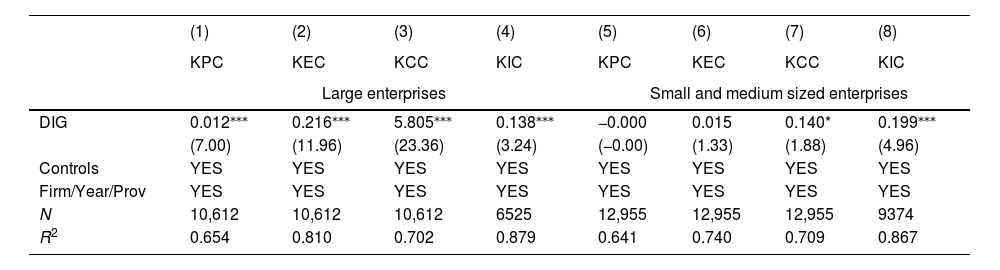

Extant literature indicates that enterprises require a certain level of innovation capability, sufficient innovation investment, and a large amount of technical talent to undergo digital transformation (Liao et al., 2024). Large enterprises endowed with abundant resources, demonstrate stronger digital transformation capabilities, whereas small and medium-sized enterprises (SMEs) exhibit weaker competitiveness, less attraction for external investments, and limited access to top-tier talent, rendering them more sensitive to the complexity and uncertainty of digital technologies (Jia et al., 2024). Consequently, SMEs often demonstrate relatively low efficiency in the digitization process. Therefore, a heterogeneity analysis is conducted based on enterprise size, categorizing enterprises with asset sizes exceeding the sample average as large enterprises and the rest as SMEs. Table 9 reports the regression results for sample subgroups based on enterprise size. For large enterprises, the estimated coefficients for digital transformation are significantly positive at the 1 % level. In contrast, for SMEs, the regression coefficients are significantly positive at the 1 % level for KIC, significant at the 10 % level for KCC, and not significant for KPC or KEC. This suggests that, because of the challenges of limited resources, SMEs may concentrate more on the accumulation and utilization of internal knowledge in their digital transformation efforts.

Heterogeneity analysis based on the size of enterprise.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| Large enterprises | Small and medium sized enterprises | |||||||

| DIG | 0.012⁎⁎⁎ | 0.216⁎⁎⁎ | 5.805⁎⁎⁎ | 0.138⁎⁎⁎ | −0.000 | 0.015 | 0.140* | 0.199⁎⁎⁎ |

| (7.00) | (11.96) | (23.36) | (3.24) | (−0.00) | (1.33) | (1.88) | (4.96) | |

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 10,612 | 10,612 | 10,612 | 6525 | 12,955 | 12,955 | 12,955 | 9374 |

| R2 | 0.654 | 0.810 | 0.702 | 0.879 | 0.641 | 0.740 | 0.709 | 0.867 |

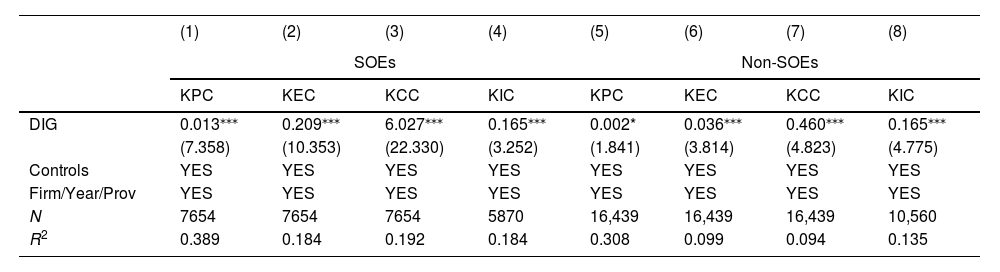

Extant literature suggests that compared to private enterprises, state-owned enterprises (SOEs) often have access to more resources and policy support, providing them with advantages in digital transformation (Kong et al., 2023; Liao et al., 2024; Wang, 2023). However, in competitive market environments where enterprises strive for profit maximization and risk avoidance, SOEs tend to engage more in applied research, leading to market failure in basic research (Ye et al., 2019). Therefore, the government will intervene in the innovation activities of SOEs by supervising their engagement in fundamental research through various mechanisms, thereby enhancing their knowledge creation capabilities. Accordingly, a heterogeneity analysis is conducted based on the differences in property rights for enterprises. Table 10 reports the regression results for SOEs and non-SOEs, showing that, except for the regression coefficient of KPC for SOEs, which is significant at the 10 % level, all other coefficients are significant at the 1 % level. Economically, for every increase of one percentage point in digital transformation for SOEs, knowledge creation capabilities compared to the sample mean increase by 28.26 %, 18.90 %, 102.59 %, and 7.54 %, respectively. In contrast, for non-SOEs, an increase of one percentage point in digital transformation results in knowledge creation capabilities compared to the sample mean increasing by 3.08 %, 3.34 %, 10.27 %, and 7.45 %, respectively. This indicates that, with non-SOEs, SOEs exhibit more pronounced promoting effects for knowledge creation capabilities through digital transformation. One possible reason is that SOEs, owing to their longer history and greater technological accumulation, can leverage the role and advantages of digital technology in the knowledge creation process.

The nature of property rights sub-sample regression results.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| SOEs | Non-SOEs | |||||||

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| DIG | 0.013⁎⁎⁎ | 0.209⁎⁎⁎ | 6.027⁎⁎⁎ | 0.165⁎⁎⁎ | 0.002* | 0.036⁎⁎⁎ | 0.460⁎⁎⁎ | 0.165⁎⁎⁎ |

| (7.358) | (10.353) | (22.330) | (3.252) | (1.841) | (3.814) | (4.823) | (4.775) | |

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 7654 | 7654 | 7654 | 5870 | 16,439 | 16,439 | 16,439 | 10,560 |

| R2 | 0.389 | 0.184 | 0.192 | 0.184 | 0.308 | 0.099 | 0.094 | 0.135 |

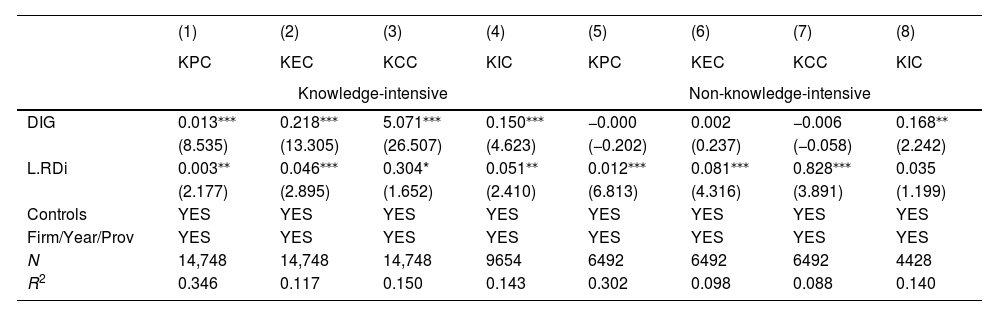

Knowledge-intensive enterprises are those in which knowledge resources play a critical role in performance. These enterprises exhibit characteristics of high knowledge scale, knowledge intensity, and R&D intensity, indicating an urgent demand for knowledge (Kotsopoulos et al., 2022; Liu et al., 2022). This study adopts the classification criteria published by the National Bureau of Statistics in the "Classification of Knowledge-Intensive Industries Based on Intellectual Property (Patent) Statistics (2019)" to classify enterprises based on whether they belong to knowledge-intensive industries. Group descriptive statistics show that, compared to knowledge-intensive enterprises, the average values of KPC, KEC, KCC, and KIC for non-knowledge-intensive enterprises are lower (0.045, 0.863, 4.350, and 1.933, respectively), highlighting the differences in knowledge creation capabilities between the two enterprise types. Considering these differences, a heterogeneity analysis is conducted. Table 11 reports the subsample regression results controlling for R&D investment, which show that, for knowledge-intensive enterprises, the DIG coefficients are significant at the 1 % level, whereas for non-knowledge-intensive enterprises, except for KIC which is significant at the 5 % level, the coefficients are not significant. This indicates that the promotion effect of enterprise digital transformation on knowledge creation capabilities is merely the "icing on the cake." Specifically, it is significant for enterprises with strong knowledge creation capabilities but not for those with weaker capabilities. This may be because enterprises with strong knowledge creation capabilities also possess strong learning capabilities, enabling them to quickly become familiar with and adapt to the digital transformation process, thereby rapidly integrating digital technologies into knowledge creation activities. Furthermore, Table 11 shows the impact of R&D investment on knowledge creation capabilities. For non-knowledge-intensive enterprises, the promoting effect of R&D investment is significant, as it not only provides essential funding for knowledge activities but also activates accumulated knowledge, thereby accelerating knowledge development.

Heterogeneity analysis based on the knowledge-intensive industry.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| Knowledge-intensive | Non-knowledge-intensive | |||||||

| DIG | 0.013⁎⁎⁎ | 0.218⁎⁎⁎ | 5.071⁎⁎⁎ | 0.150⁎⁎⁎ | −0.000 | 0.002 | −0.006 | 0.168⁎⁎ |

| (8.535) | (13.305) | (26.507) | (4.623) | (−0.202) | (0.237) | (−0.058) | (2.242) | |

| L.RDi | 0.003⁎⁎ | 0.046⁎⁎⁎ | 0.304* | 0.051⁎⁎ | 0.012⁎⁎⁎ | 0.081⁎⁎⁎ | 0.828⁎⁎⁎ | 0.035 |

| (2.177) | (2.895) | (1.652) | (2.410) | (6.813) | (4.316) | (3.891) | (1.199) | |

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 14,748 | 14,748 | 14,748 | 9654 | 6492 | 6492 | 6492 | 4428 |

| R2 | 0.346 | 0.117 | 0.150 | 0.143 | 0.302 | 0.098 | 0.088 | 0.140 |

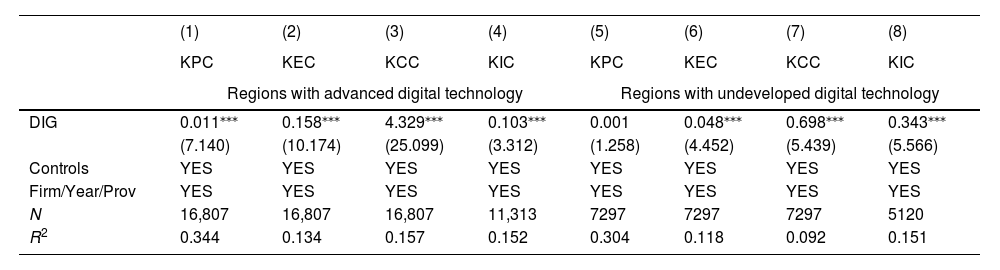

When considering the boundaries of the enterprise, Ba can be divided into "internal knowledge Ba" and "external knowledge Ba." Internal Ba has the most direct influence on the enterprises’ knowledge creation activities, while external Ba indirectly affects the enterprises’ knowledge creation behavior through energy transmission. Especially in the digital era, enterprises have seen their boundaries increasingly blurred, formed by complex networks of the internet and social relationships. The penetration of external Ba for enterprises is expanding both in breadth and depth. Therefore, enhancing knowledge creation capabilities through external Ba is equally important for enterprises. To investigate whether differences exist in the impact of external digital technology levels on various knowledge creation capabilities, this study conducts subsample regressions based on the digital technology development levels of the regions in which enterprises are located, dividing them into regions with advanced digital technology and regions with undeveloped digital technology. The digital technology level of each region is evaluated based on three aspects: the level of digital technology development, reserve of digital talents, and level of digital technology services. Comprehensive scores are calculated using the entropy weight method. In this study, regions that were consistently above the average level between 2010 and 2020 are defined as regions with advanced digital technology, whereas the other provinces are defined as regions with undeveloped digital technology. The results show that Beijing, Shanghai, Guangdong, Jiangsu, Zhejiang, Tianjin, Fujian, and Sichuan are regions with advanced digital technology, whereas the other provinces are regions with undeveloped digital technology. Table 12 reports the results of the sub-sample regression, in which the coefficients for all variables except KPC in regions with undeveloped digital technology are significant at the 1 % level, indicating that the level of external digital technology development has the most significant promoting effect on the socialization process through enterprise digital transformation. This may be because areas with underdeveloped digital technology lack digital infrastructure and talent reserves, limiting the capability of enterprises to engage in digital transformation as well as knowledge sharing and exchange.

Heterogeneity analysis based on the regions.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| Regions with advanced digital technology | Regions with undeveloped digital technology | |||||||

| DIG | 0.011⁎⁎⁎ | 0.158⁎⁎⁎ | 4.329⁎⁎⁎ | 0.103⁎⁎⁎ | 0.001 | 0.048⁎⁎⁎ | 0.698⁎⁎⁎ | 0.343⁎⁎⁎ |

| (7.140) | (10.174) | (25.099) | (3.312) | (1.258) | (4.452) | (5.439) | (5.566) | |

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 16,807 | 16,807 | 16,807 | 11,313 | 7297 | 7297 | 7297 | 5120 |

| R2 | 0.344 | 0.134 | 0.157 | 0.152 | 0.304 | 0.118 | 0.092 | 0.151 |

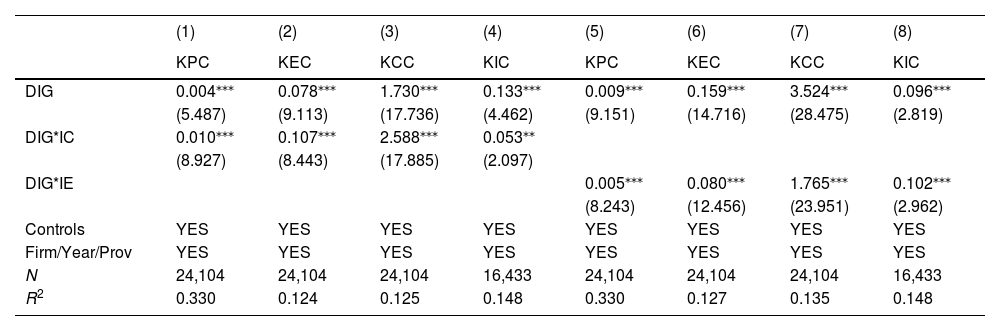

Innovation culture refers to the spirit and values displayed in an enterprise's innovation activities. It is a concept and consciousness formed by long-term accumulation within a company that possesses both guiding values and behavioral constraints, thus exerting an undeniable influence on the innovation development of the enterprise (Lee et al., 2017). Companies with a strong innovation culture demonstrate greater flexibility and an enhanced ability to adapt quickly to change and seize new opportunities during unstable periods (Salah & Ayyash, 2024). During the digital transformation process, employees must continuously learn and adapt to new technologies and tools. Therefore, driven by the promotion of innovation culture, employees are more likely to be actively engaged in learning, constantly enhancing their skills and knowledge levels, and thereby promoting knowledge creation and transformation.

Therefore, this study further analyzes the benchmark regression model by incorporating variables for innovation culture (IC), along with interaction terms with enterprise digital transformation. The innovation culture is represented by the frequency of terms such as "innovation" and "technological breakthrough" collected from annual reports to indicate the extent to which the enterprise values innovation culture. Columns (1)–(4) of Table 13 report the test results for internal innovation culture, in which the regression coefficients of DIG are all significant at the 1 % level and the interaction terms are also significant, indicating that the higher the internal innovation culture within the enterprise, the more significant the promoting effect of digital transformation on knowledge creation capability.

Further analysis considering innovation culture.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| KPC | KEC | KCC | KIC | KPC | KEC | KCC | KIC | |

| DIG | 0.004⁎⁎⁎ | 0.078⁎⁎⁎ | 1.730⁎⁎⁎ | 0.133⁎⁎⁎ | 0.009⁎⁎⁎ | 0.159⁎⁎⁎ | 3.524⁎⁎⁎ | 0.096⁎⁎⁎ |

| (5.487) | (9.113) | (17.736) | (4.462) | (9.151) | (14.716) | (28.475) | (2.819) | |

| DIG*IC | 0.010⁎⁎⁎ | 0.107⁎⁎⁎ | 2.588⁎⁎⁎ | 0.053⁎⁎ | ||||

| (8.927) | (8.443) | (17.885) | (2.097) | |||||

| DIG*IE | 0.005⁎⁎⁎ | 0.080⁎⁎⁎ | 1.765⁎⁎⁎ | 0.102⁎⁎⁎ | ||||

| (8.243) | (12.456) | (23.951) | (2.962) | |||||

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Firm/Year/Prov | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 24,104 | 24,104 | 24,104 | 16,433 | 24,104 | 24,104 | 24,104 | 16,433 |

| R2 | 0.330 | 0.124 | 0.125 | 0.148 | 0.330 | 0.127 | 0.135 | 0.148 |

If enterprises have an external environment that fosters a strong innovation culture, this will indicate a wealth of potential innovation resources available to those enterprises. These resources provide enterprises with more opportunities and support, facilitating the introduction and application of new technologies and methods required for digital transformation, thereby enhancing the knowledge creation capability of an enterprise. Moreover, such an atmosphere tends to stimulate employees' innovative potential, which will drive the advancement of innovation activities in turn.

Therefore, this study further analyzes the benchmark regression model by incorporating variables for the innovation environment (IE), along with interaction terms with enterprise digital transformation. IE is measured using the City Innovation and Entrepreneurship Index. Columns (5)–(8) of Table 13 report the test results for external innovation culture, in which the regression coefficients of DIG are all significant at the 1 % level, and the interaction terms are also significant, indicating the important moderating role of external innovation environment.

Conclusions, implications, and future research directionConclusionsThis study innovatively quantifies the four knowledge creation processes. Based on a sample of manufacturing companies listed on the A-share market in China from 2007 to 2020, empirical analysis is used to investigate the relationship between digital transformation and different knowledge creation capabilities. Furthermore, heterogeneity effects are considered, including factors such as enterprise size, ownership nature, geographical location, and industry type. The main findings of this study are described below.

First, enterprise digital transformation plays a significant role in promoting KPC, KEC, KCC and KIC, with KCC being the most significant. Enterprise digital transformation can better integrate existing knowledge to promote the generation of explicit knowledge, which coincides with the opinion proposed by Cadden et al. (2023). Moreover, positive interrelations among the different knowledge creation capabilities are confirmed. Socialization, externalization, combination, and internalization generate a spiral of knowledge creation, promote each other, and form a cycle. This confirms the conclusion of Nonaka (1994).

Second, digitalization input, as a subdimension of digital transformation, will have a negative impact on KPC and KIC; however, the effects on KEC and KCC are insignificant. This could be attributed to the fact that knowledge socialization and internalization heavily rely on creative employees and require strong human capital. However, digital transformation is a long-term project that requires continuous investment of funds, human resources, and other resources, which may crowd out the resources needed for socialization and internalization processes.

Finally, digital transformation primarily acts as the "cherry on top," exhibiting more significant effects on enterprises with stronger knowledge creation capability. For enterprises with weak knowledge creation capability, digital transformation can promote KIC; however, the effects on KPC, KEC and KCC are insignificant. Moreover, a weaker level of digital technology development in a region may constrain the promoting effect of digital transformation on knowledge socialization. Furthermore, the promoting effect of digital transformation on knowledge creation capabilities is more pronounced in large and state-owned enterprises. In SMEs, it has a significant promoting effect on KIC; however, the promoting effects of KCC, KPC and KEC are insignificant. Lastly, enterprise innovation culture and regional innovation environments positively moderate the relationship between digital transformation and knowledge creation.

Policy implicationsBased on this study's findings, we propose several policy implications as following.

First, from the governmental perspective, it is important to pay attention to the development environment of enterprises and help them with digital transformation and knowledge creation. To create a good digital environment, it is necessary to promote the construction of digital technology infrastructure, including providing a more universal and stable network environment, and increasing the investment in data centers, big data technology platforms, and cloud computing platforms. Furthermore, fostering a conducive innovation environment, such as investing in the construction of research institutes, incubators, and technology parks, would provide a favorable environment for research and entrepreneurship. In addition, it is necessary to provide enterprises with policy guidance and support for digital transformation. In particular, for resource-constrained enterprises, digital transformation is relatively difficult, with challenges faced in making a positive impact on knowledge creation capabilities. Therefore, governments should actively guide leading enterprises to open platforms and share resources, thereby providing support to SMEs. Meanwhile, it is also essential to guide financial institutions to strengthen cooperation with enterprises, expand financing channels for enterprises, and alleviate the shortage of funds.

Second, from enterprise perspective, they need to recognize the importance of digital transformation. Driving the extensive application of digital technologies such as big data, blockchain, the Internet, 5G, cloud computing, and artificial intelligence is essential in areas such as R&D, marketing services, and management decisions, as is further expanding the application scenarios of digital transformation in knowledge creation. Because digitalization inputs may have a negative effect on knowledge creation, for enterprises with limited resources; therefore, it is necessary to carefully evaluate the resource allocation between digital transformation and knowledge creation. For enterprises with weaker knowledge creation capabilities, they need to pay more attention to utilizing existing knowledge to promote the development of new products. Additionally, because innovation culture enhances the role of digital transformation in promoting knowledge creation capabilities, enterprises must strengthen the facilitation of an internal innovation culture, encourage employees to actively participate in knowledge creation activities, and foster a work atmosphere that encourages innovation and knowledge sharing.

Limitations and future research directionOur study has several limitations that should be addressed in future research. First, constrained by data availability, this study utilizes only patent data to measure knowledge creation capability, which has certain limitations. In future research, alternative measurement methods such as questionnaire surveys or interviews could be employed to enhance and complement the findings of this study. Second, our study focuses on the direct effects of digital transformation on knowledge creation. We should continue to deepen the theoretical discussion on the intermediate mechanism, explore the realization path, and empirically test its effect. Finally, considering the various stages of enterprise digital transformation, we can further investigate its effects on knowledge creation.

FundingThis research is funded by National Philosophy and Social Science Foundation of China (NO. 19ZDA122). This work also supported by the characteristic & preponderant discipline of key construction universities in Zhejiang province (Zhejiang Gongshang University-Statistics) and Collaborative Innovation Center of Statistical Data Engineering Technology & Application.

CRediT authorship contribution statementYufen Chen: Conceptualization, Funding acquisition, Supervision, Writing – review & editing. Xiaoyi Pan: Conceptualization, Data curation, Formal analysis, Methodology, Writing – original draft, Writing – review & editing. Pian Liu: Data curation, Supervision. Wim Vanhaverbeke: Supervision, Writing – review & editing.