To address global climate change and achieve high-quality development, China has to reach carbon peaking and carbon neutrality targets as objective requirements. Based on data from 30 Chinese provinces from 2011 to 2021, this study used a two-factor fixed effects and a mechanism model to test the effects and mechanisms of digital finance on carbon performance. The findings imply that the development of digital finance has a nonlinear effect of the "first inhibit, then promote" principle on carbon performance. Meanwhile, both the coverage breadth and usage depth of digital finance have a more significant impact on carbon performance. Digital financing can improve regional carbon performance through green technology innovation, industrial upgrades, and energy structure optimization. In addition, this effect exhibited significant heterogeneity. Specifically, the higher the level of marketization and the lower the urban–rural income gap, the more significant the nonlinear effect. The eastern region has the advantage of being rich in resources and technology, and the effect in the eastern region is more obvious compared to central and western regions. Therefore, China should accelerate the integration of financial services with modern digital technologies to achieve low-carbon development based on local conditions.

In the context of global warming, green and low-carbon development has become a common goal for everyone in the world, and achieving high-quality development has been pursued in China. In September 2020, the Chinese government first proposed the “dual carbon goals,” with the goal of peaking carbon emissions by 2030 and achieving carbon neutrality by 2060. Low-carbon development is China's long-term goal. Simultaneously, China's digital economy has entered a new stage, and digitally enabled financing has created new opportunities for the development of China's finance industry. Digital finance is characterized by convenient transactions diversified services, and extensive coverage that have greatly improved financial accessibility and reduced financing costs. As the lifeblood of society, finance plays an indispensable role in the process of economic development and is also a key supporting element for achieving carbon peaking and carbon neutrality.

In recent years, scholars have paid sufficient attention to digital finance and explored its economic effects(Ahluwalia et al., 2020; Deng & Liu, 2022). Digital finance is characterized by convenient transactions, diversified services, and wide coverage, which greatly improve financial accessibility and reduce financing costs, and further promoting the rapid development of enterprises and the social economy(Tang et al., 2022; Tang & Geng, 2024). Some scholars also pay attention to its environmental benefits, believing that the development of digital finance can have a beneficial impact on the environment and improve carbon performance by promoting technological innovation and improving production efficiency (Cao et al., 2021; Ma, 2023). However, digital finance may not only have a promoting effect on carbon performance improvement. Digital finance will promote carbon dioxide emissions by increasing industry scale and leading to more energy consumption (Sadorsky, 2010). Scholars' research on the impact of digital finance development on carbon performance has not reached a consistent conclusion. More research is needed to support the role and mechanism of digital finance in carbon performance.

What role does digital finance play in low-carbon development? Digital finance can alleviate enterprises’ financing constraints. With improvements in financing constraints, enterprises can use more funds to expand their production scale, which is called the scale effect. However, when enterprises have sufficient funds, they are more likely to increase their research and development (R&D) investment and promote technological innovation (Lin & Ma, 2022), which can be referred to as the technology effect. The scale effect often accompanies an increase in material resource consumption and carbon emissions, and it has a suppressive effect on carbon performance. Technological effects can improve carbon performance by enhancing production efficiency and reducing unit energy consumption. The joint influence of the "scale effect" and "technology effect" (Fan & Feng, 2022) indicates that digital finance may have a positive and negative impact on carbon performance, depending on the dominating effect. Therefore, the dominant effects vary at different stages, and digital finance exhibits nonlinear effects on carbon performance.

Based on the above analysis, this study uses panel data of Chinese provinces from 2011 to 2021 to analyze the impact of digital finance on China's carbon performance under the dual effects of scale and technology, and empirically tests this nonlinear effect. Compared with existing research, the marginal contribution of this study lies in the fact that the existing literature on digital finance and carbon performance mainly focuses on exploring the impact of carbon emissions, and empirical research on carbon performance is still insufficient. Meanwhile, most scholars test the impact of digital finance development on carbon performance based on single linear thinking, whereas this study deepens and supplements the relationship between the two based on nonlinear thinking. In addition, this study analyzes the mechanism of digital finance's impact on carbon performance, revealing a black box between the two from the perspectives of industrial structure upgrading, green technology innovation, and energy structure improvement. This study examines the heterogeneity of this effect based on different levels of marketization and urban–rural disparities, further enriching the theoretical understanding of the economic effects of digital finance on carbon performance and providing policy recommendations for promoting the achievement of China's "carbon peak and carbon neutrality" goals.

The remainder of the paper is organized as follows. First, we evaluated all relevant research and propose research hypotheses based on it. Then, we introduce the research design and conduct an empirical test on the effects and mechanisms of digital finance development on carbon performance. Further analysis was conducted to examine the heterogeneity of effects. Finally, research conclusions and policy recommendations are provided.

Literature reviewStudies on digital financeDigital finance is a new form of business created through the integration of modern information technology and finance. It is also an upgrade to traditional financial products, services, business models, and technological frameworks in various aspects (Gomber et al., 2017). With the continuous development of digital finance, scholars have paid considerable attention to its economic impacts. Digital finance can improve the efficiency of financial institutions using methods such as big data and cloud computing. It supplements the traditional financing situation dominated by bank lending, expands financing channels for enterprises, and reduces financing costs (Xiong et al., 2023). The easing of financing constraints for enterprises helps in their research and innovation and enhances market competitiveness (Wu & Huang, 2022). In addition, the development of digital finance helps improve the efficiency of social resource allocation and promotes industrial transformation and upgrading by optimizing resource allocation (Zhang et al., 2022). Simultaneously, digital finance stimulates economic development by driving social demand and supplementing social resource supply, playing an important role in promoting high-quality development (Xie & Liu, 2022). With increasing attention to the environment, scholars have explored the environmental benefits of digital finance and found that digital finance can suppress pollution emissions and produce good environmental benefits by promoting innovation (Xu et al., 2023), optimizing resource allocation, and improving green total factor productivity (Cao et al., 2021). Scholars have found that digital finance can promote economic expansion, increase material resource consumption, and adversely affect low-carbon development (Bakirtas & Akpolat, 2018).

Studies on carbon performanceRecently, carbon performance has become a popular research topic. In order to better evaluate carbon performance, scholars have developed diversified methods to measure carbon performance. In terms of carbon performance measurement, some scholars start with carbon emission intensity (Yang et al., 2022) or connect it to certain value indicators for examination. For example, Ang and Choi (2002) use carbon intensity to measure the carbon performance COP by the carbon emissions per unit of GDP, while others employ the output-input model for the total factor Malmquist index (Ren & Sun, 2022) or the entropy method to construct comprehensive indicators to measure its environmental benefits from multiple dimensions (Tian et al., 2023).

In addition, scholars have conducted in-depth research on the factors influencing carbon performance. From a macro perspective, environmental investment (Jaana Rahko, 2023), financial development (Khan et al., 2020), and government environmental information disclosure (Peng et al., 2023) all contribute to the improvement of carbon performance. In addition, green finance agglomeration improves carbon emissions performance through capital formation, energy transformation, and technological progress (Zhang et al., 2024). At the micro level, most scholars have verified the positive effects of technological innovation on carbon performance. Technological innovation improves production efficiency and reduces material resource consumption, significantly affecting corporate carbon performance (Opazo-Basáez et al., 2024; Zhai & Liu, 2023).

Studies on the effect of digital finance on carbon performanceAt present, the relationship between financial development and carbon emissions has been fully explored by scholars, and the correlation between them has been affirmed; however, whether financial development plays a positive or negative role in the improvement of carbon performance, different scholars have reached different conclusions based on empirical results.

Some scholars believe that financial development has a positive effect on curbing carbon emissions. Tamazian et al. (2009) studied the BRIC countries (Brazil, Russia, India, and China) and found that financial development can promote technological R&D improvements and thus reduce carbon emissions. Using South Africa as an example,Shahbaz et al.’s (2013)show that financial development can lead to more funds flowing to environmentally friendly projects and ultimately reduce pollution emissions. Using Central and Eastern European economies as a study, Zioło et al. (2020) argue that green finance impacts greenhouse gas emissions by imposing carbon taxes on carbon-oriented projects and promoting R&D on low-carbon technologies. Some Chinese scholars have also empirically demonstrated through their studies that industrial upgrading and technological innovation brought about by financial development can help reduce China's carbon intensity and improve its carbon performance (Ji et al., 2022; Liu et al., 2022).

Some scholars have argued that financial development has an expansionary effect and may, therefore, act as an inverse promoter of carbon emissions. Sadorsky (2010) states that financial development increases the financing capacity of firms, which, in turn, increases production capacity and leads to the expansion of energy consumption. Charfeddine and Mrabet (2017) note that financial development reduces environmental quality in Qatar by increasing its ecological footprint in the short and long term. However, there is heterogeneity in the play of its role; Destek and Sarkodie (2019) also point out that the exertion of this effect was found to vary across countries.

Digital finance is a new trend in finance development, and scholars have focused on the unique benefits of digital finance development and studied its impact on carbon emissions. Some scholars have measured the impact of digital finance on carbon performance from the perspectives of carbon emissions and carbon intensity and affirmed the positive effect of digital finance in reducing carbon emissions and improving carbon performance (Gu, 2022). The inhibitory effect of digital finance development on carbon emissions is primarily due to the promotion of industrial progress (Lei et al., 2023), green technological innovation, and energy structure transformation (Wu et al., 2022). However, some scholars have also assumed a household perspective and found that the development of digital finance promotes household developmental consumption, thus contributing to an increase in carbon emissions (Wang et al., 2022). In addition, the scale and technology effects of digital finance differ at different stages of development; thus, the effects on carbon emissions are also different (Yin, 2022).

Evaluation of related literatureIn general, scholars have made rich studies and analyses on the relationship between finance development and carbon emissions. However, different scholars have drawn different conclusions based on their research results as to whether finance development has a positive or negative effect on carbon performance improvement. The difference in this effect is mainly caused by the joint influence of the scale and technology effect, and the effect could be heterogeneous for different countries and regions, which needs to be further verified according to the actual situation in China.

Additionally, the impact of digital finance on carbon performance requires further clarification. Whether this effect will be affected and exhibit heterogeneity under different levels of marketization and urban–rural income inequality requires further exploration. Therefore, it is of theoretical and practical significance to explore the nonlinear effects and impact mechanisms of digital finance on carbon performance based on the actual circumstances in China.

Theoretical analysis and research hypothesesFirst, digital finance provides enterprises with convenient financial services and financing constraints (Xie et al., 2022). With improvements in corporate financing constraints, enterprises have the ability to conduct technological research and expand their industrial scale, which can be referred to as scale and technological effects (Wang et al., 2022). On the one hand, scale effects are accompanied by more carbon emissions, which have a negative impact on regional carbon performance (Zhou et al., 2021). On the other hand, technological effects can improve production efficiency, thereby improving regional carbon performance (Chu et al., 2022). However, the development of these new technologies requires considerable time. In the early stages, the technological effect had not yet formed. The scale effect plays a leading role. In the long term, technological effects gradually form and are beneficial for improving carbon performance. Therefore, based on the above theoretical analysis, Hypothesis 1 was proposed.

Hypothesis 1 The development of digital finance has a nonlinear effect of inhibiting and promoting the improvement of carbon performance.

Second, digital finance has a demonstration effect to promote the development of digital economy entrepreneurship, boosting the development of digital technology and emerging industries (Tu & He, 2021). Most emerging digital economy industries are concentrated in tertiary industries, which are naturally characterized by low-carbon emissions. However, digital finance promotes the transformation of traditional industries into intelligent and green development through resource allocation and improves the efficiency of industrial resources and energy utilization (Feng et al., 2023). Therefore, the development of digital finance is conducive to accelerating the industrial transformation. The optimization of the industrial structure is conducive to the improvement of resource utilization efficiency (Muhammad et al., 2022), promotion of green productivity, and development of the economy, thus improving social carbon performance. Therefore, based on the above theoretical analysis, Hypothesis 2 was proposed.

Hypothesis 2 Digital finance improves carbon performance through the upgrading of industrial structure.

Finally, digital finance provides financial support for enterprises and alleviates their financing constraints. In addition, it provides enterprises with more capital for technological research and upgrades (Razzaq & Yang, 2023). Simultaneously, digital finance can use big data to intelligently analyze financing targets, supporting high-quality and sustainable enterprises (Tang et al., 2023). Second, digital finance has a development-oriented function, and enterprises will take the initiative to carry out green technological innovation to achieve further development and obtain financial support (Hewage et al., 2022). Therefore, the development of digital finance has a positive incentive effect on green technology innovation (Xu et al., 2023). The improvement in green innovation technology can improve unit production efficiency, save resources and energy, reduce pollutant generation, and promote sustainable development. (Guo et al., 2022). Therefore, based on the above theoretical analysis, we propose Hypothesis 3.

Hypothesis 3 Digital finance enhances carbon performance through green technological innovation.

Digital finance promotes energy structure optimization through resource optimization and allocation. On the one hand, compared to traditional high-energy-consuming industries, high-value-added enterprises are more likely to obtain funding. This increase in financing costs forces enterprises to accelerate innovation in production methods and technologies, improve energy efficiency, and reduce high-carbon energy consumption (Lee et al., 2023). On the other hand, in the energy industry, digital finance increases funding support for clean energy production enterprises, such as solar and wind energy, provides financial support for the technological transformation of energy enterprises, and promotes the transformation and upgrading of the energy industry (Ji & Zhang, 2019). With improvements in energy production efficiency and the expansion of clean energy production, the cost of using clean energy has decreased, its application scope has expanded, and clean energy has gradually formed a substitute for traditional high-carbon energy. With continuous improvements in the energy consumption structure, carbon consumption per unit output has decreased, enhancing regional carbon performance (Hussain et al., 2023).

Hypothesis 4 Digital finance enhances carbon performance through energy structure improvement.

- (1)

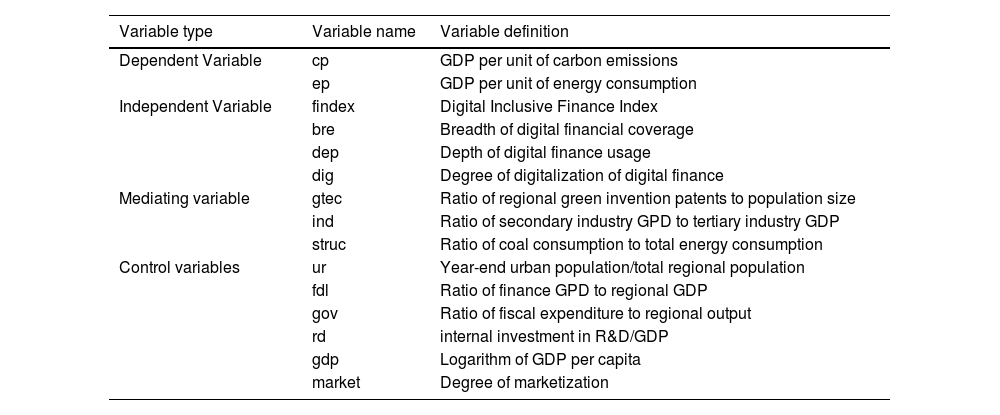

Dependent variables

Carbon performance (cp): Scholars have different ways to measure carbon performance. Zhang et al. (2023) use the output and input model to measure the overall performance by treating carbon emissions as undesired outputs and other scholars use the ratio of carbon emissions to the total regional output to measure unit carbon intensity (Song et al., 2023; Xu et al., 2023). Drawing on the above-mentioned ideas, the ratio of regional output to regional carbon emissions was used to measure carbon performance, which reflects the relative relationship between inputs and outputs and could be a better measure of regional carbon performance.

According to the carbon emission coefficients of each energy source provided in the Guidelines for the Preparation of Provincial Greenhouse Gas Inventories and IPCC2006, nine energy sources (i.e., coal, coke, crude oil, gasoline, kerosene, diesel fuel, fuel oil, liquefied petroleum gas, and natural gas) were selected to calculate carbon emissions. The specific method for accounting for CO2 emissions is given by the following equation:

where Ci is the carbon emissions of province i, λj is the discounted standard coal coefficient of energy j, ηj is the carbon emission coefficient of energy j, Eij is the actual consumption of energy j in province i, and the data are obtained from the National Energy Statistics Yearbook.

Energy performance (ep): The ratio of the regional GDP to energy consumption in the region is used to replace the explained variables in the subsequent robustness test, which represents the economic efficiency of the regional unit of energy consumption and has a consistent logical relationship with carbon performance.

- (2)

Independent variables

Digital finance (Findex): The digital finance inclusion index was released by the Digital Finance Research Center of Peking University. Findex is based on real-life data provided by Ant Financial Services and the multilevel index system established from the three levels of breadth of digital finance coverage (bre), depth of digital finance use (dep), and degree of digitization of inclusive finance (dig), which can effectively evaluate the development level of digital finance in different regions of China.

- (3)

Control variables

In addition, drawing on the research of previous scholars (Kameyama et al., 2016; Acheampong et al., 2020; Waleed et al., 2024), this article selects variables that may have an impact on carbon performance as control variables, as follows: (1) economic development level (gdp), expressed as the logarithmic value of per capita GDP; (2) urbanization level (ur), measured as the proportion of the urban population to the total population; (3) research and development (rd), expressed as the proportion of intraregional R&D expenditure to the regional GDP; (4)finance development level (fdl), expressed as the proportion of the financial industry GDP to the regional GDP; (5) financial input (gov) is expressed as the ratio of regional financial expenditure to regional GDP; and (6) degree of marketization (market), which is expressed by the Fan Gang marketization index.

- (4)

Mediating variables

Green Technology Innovation (gtec): Referring to Muganyi et al.'s (2021), this research defines the ratio of the number of green patent of each province to the regional population as green technology innovation. Compared to the total number of innovative patents, the per capita green innovation quantity can more appropriately and intuitively reflect the regional green innovation capacity.

Advanced industrial structure (ind): It is measured as the ratio of the output value of the tertiary sector in industry compared with that of the secondary industry. Tertiary industries are characterized by low energy consumption and high efficiency and are more environmentally friendly than secondary industries. Therefore, the ratio reflects the upgrading of the industry and is multiplied by 100.

Energy structure improvement (struc): According to Sun et al. (2018), this study defined the proportion of coal consumption to total energy consumption as the energy structure. Coal combustion produces more pollutants than fossil fuels. A decrease in the proportion of coal consumption represents an improvement in the energy structure, which is more beneficial to the environment.

The definitions and descriptions of all variables are shown in Table 1.

Definition of variables.

- (1)

Baseline regression model

Based on the theoretical foundation and hypotheses of the literature study, referring to the research of previous scholars (Kiefer, 1980), we constructed a fixed effects model to test the impact of digital finance on carbon performance. Considering the nonlinear relationship between digital finance development and carbon performance proposed in this study's hypothesis, a quadratic term is introduced into the benchmark model:

where the explained variable cpit is the carbon performance of province i in year t, the core explanatory variable findex is the level of digital finance development of province i in year t, and the vector cit represents a set of control variables that may affect energy efficiency; λi denotes individual fixed effects, ηt denotes time fixed effects, and εit denotes random disturbance terms.

- (2)

Sub-dimensional regression model

To investigate the impact of each segmentation dimension of digital finance on carbon performance, digital finance coverage breadth, usage depth, and degree of digitization were used as explanatory variables and regression equations were constructed in the following form:

- (3)

Intermediate effect model

Referring to the causal steps approach of (Baron & Kenny, 1986), the mediating effect model equation can be constructed in the following form:

Other variables are interpreted as above, where Mit is the mediating variable, and the green technology innovation (gtec), industrial structure upgrading (ind), and energy structure advanced (struc) are selected as mediating variables in this study.

- (4)

Threshold model

In further analysis, a threshold model was used to test the impact of digital finance on carbon performance at different carbon emission intensities using the panel threshold model proposed by Hansen (1999) as follows:

where I(·) represents the schematic function and takes the value of 1 if the expression in parentheses is true; otherwise, it takes the value of 0. γ is the threshold value to be estimated, and Cit denotes the corresponding control variable; λi denotes the individual fixed effect, ηt denotes the time fixed effect, and εit denotes the random disturbance term.Data sources

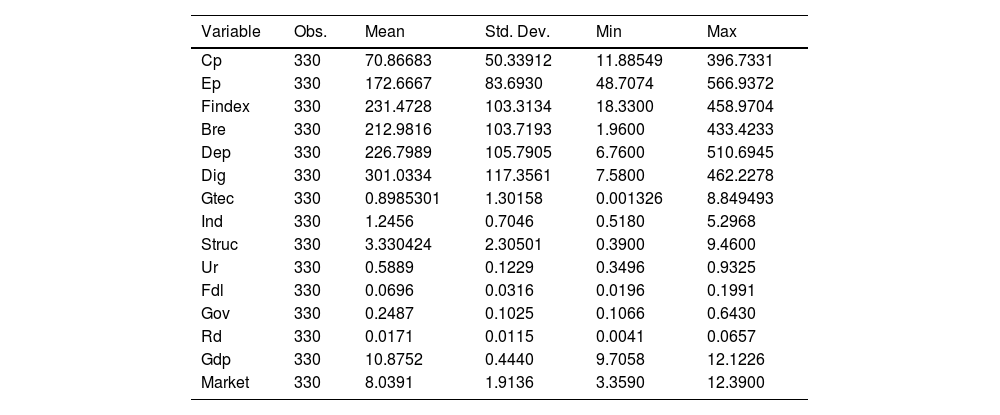

Considering the availability and consistency of the original index data, this study took the panel data of 30 provinces and municipalities in China, except for the Tibetan region, from 2011 to 2021 as the sample for empirical research. Energy consumption data are from the China Energy Statistical Yearbook. Macroeconomic data are from CSMAR, green patent data are collected from the EPS database, and the digital finance index was issued by the Digital Finance Research Center of Peking University. The descriptive statistics of the variables are shown in Table 2.

Descriptive statistics of variables.

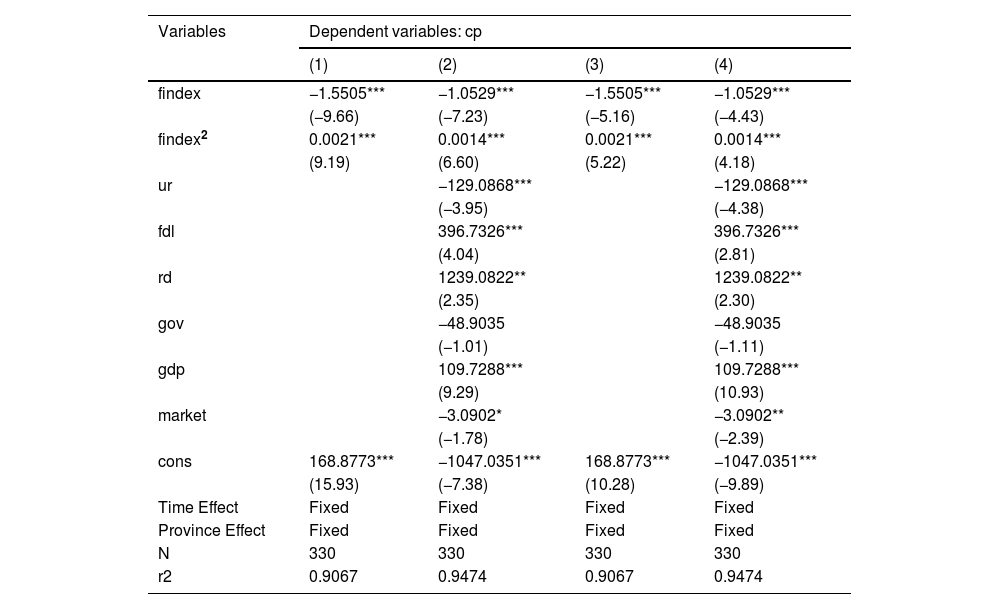

A two-way fixed effects model is used to estimate the effect of digital finance on carbon performance, and the regression results are shown in Table 3. Columns (1) and (2) report the impact of the digital finance index on carbon performance, and all regressions control for individual fixed effects and time fixed effects. Column (1) does not include control variables, and Column (2) shows the regression results after adding control variables. The regression results show that the coefficients of linear and quadratic entries of the digital finance index are negative and positive at the 1 % significance level, respectively; the slope is negative when the independent variable takes the minimum value (k1=2 × 0.0014×18.33- 1.0529= 1.0016) and positive when the independent variable takes the maximum value (k2=2 × 0.0014×458.9704- 1.0529=0.2322); the inflection point (1.0529/(2 × 0.0014)=376.0357) falls within the range of values of the independent variable, and the three conditions for the U-shaped curve were satisfied. In other words, the development of digital finance has a nonlinear impact on carbon performance, which is "inhibited first and then promoted.”

Regression results of the effect of digital finance on carbon performance.

| Variables | Dependent variables: cp | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| findex | −1.5505*** | −1.0529*** | −1.5505*** | −1.0529*** |

| (−9.66) | (−7.23) | (−5.16) | (−4.43) | |

| findex2 | 0.0021*** | 0.0014*** | 0.0021*** | 0.0014*** |

| (9.19) | (6.60) | (5.22) | (4.18) | |

| ur | −129.0868*** | −129.0868*** | ||

| (−3.95) | (−4.38) | |||

| fdl | 396.7326*** | 396.7326*** | ||

| (4.04) | (2.81) | |||

| rd | 1239.0822** | 1239.0822** | ||

| (2.35) | (2.30) | |||

| gov | −48.9035 | −48.9035 | ||

| (−1.01) | (−1.11) | |||

| gdp | 109.7288*** | 109.7288*** | ||

| (9.29) | (10.93) | |||

| market | −3.0902* | −3.0902** | ||

| (−1.78) | (−2.39) | |||

| cons | 168.8773*** | −1047.0351*** | 168.8773*** | −1047.0351*** |

| (15.93) | (−7.38) | (10.28) | (−9.89) | |

| Time Effect | Fixed | Fixed | Fixed | Fixed |

| Province Effect | Fixed | Fixed | Fixed | Fixed |

| N | 330 | 330 | 330 | 330 |

| r2 | 0.9067 | 0.9474 | 0.9067 | 0.9474 |

(Note: * p < 0.1, ** p < 0.05, *** p < 0.01; T-values for robust standard errors are in parentheses.).

Analyzing the possible reasons, the development of digital finance in the initial stage can alleviate financing constraints for enterprises based on its inclusive characteristics, further promoting the expansion of enterprise production scale. At this point, scale effects play a major role, whereas technological effects are not yet established. Upgrading industrial structures requires certain development and accumulation, and digital finance plays a restraining role in improving carbon performance. However, with the further integration of digital finance and enterprises, the development of digital finance can provide sufficient financial support for green innovation of enterprises, making the emission reduction effect formed by the "technology effect" exceed the expansion of the "scale effect.” Simultaneously, with the development of emerging industries and the optimization of the industrial structure, green efficiency improves, unit carbon emission output increases, and the development of digital finance plays a role in improving carbon performance. The results using robust standard errors are presented in Columns (3) and (4), and Table 3 shows that the results are still significant at the 1 % level.

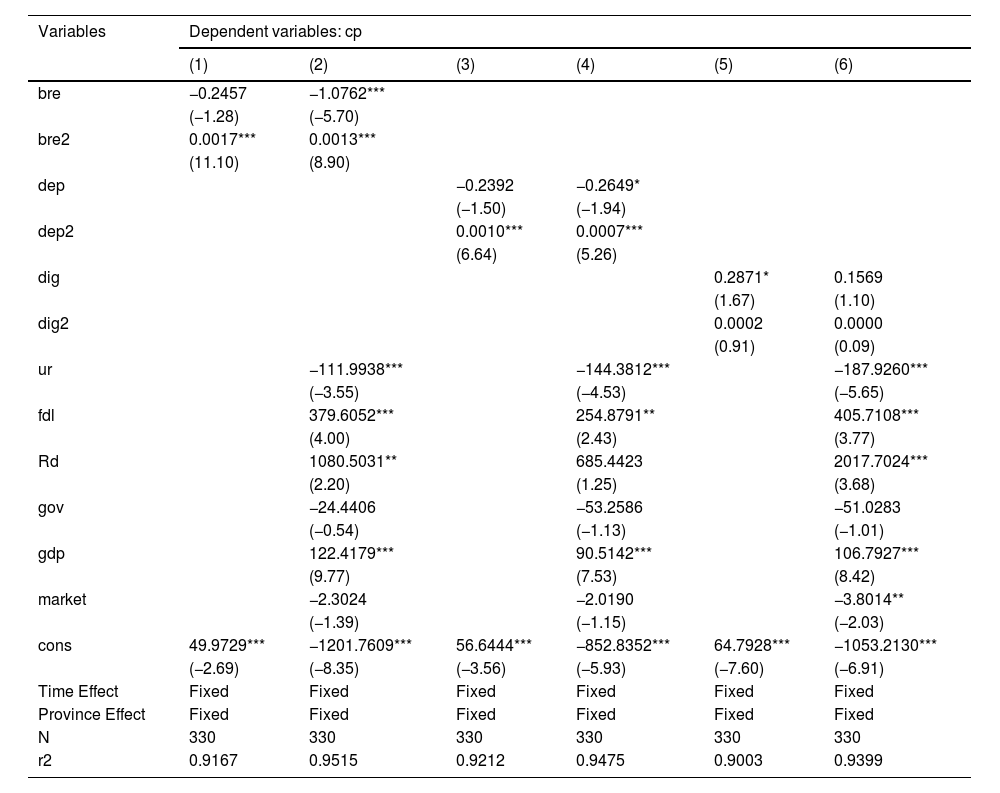

Sub-dimensional analysisDigital finance is a comprehensive indicator with multilevel and diverse characteristics. Table 4 presents the regression results to examine the role of its sub-dimensions on energy intensity and their impact on carbon performance.

Regression results of digital finance segmentation dimensions.

(Note: * p < 0.1, ** p < 0.05, *** p < 0.01; T-values for robust standard errors are in parentheses.).

Columns (1) and (2) in Table 4 present the regression results of the breadth of digital finance coverage on carbon performance, where the coefficients of the linear and quadratic terms are negative and positive, respectively. The regression results presented in Columns (3) and (4) for the depth of digital finance use on carbon performance show that the coefficient of the quadratic term is significantly positive, which also has a nonlinear effect of "suppressing first, then increasing" on carbon performance, further verifying Hypothesis 1. Columns (5) and (6) show the regression results for the degree of digitization of digital finance on carbon performance, indicating that the degree of digitization does not have a significant effect on carbon performance.

The lack of significant impact of digitization on carbon performance may stem from the fact that China's financial digitization development is still undergoing continuous transformation and progress, and the digitization effect is achieved better by empowering the financial industry to develop strongly. The improvement of digitization symbolizes the improvement of the integration level between finance and digital technology, which helps improve the efficiency of financial institutions and expands the depth and coverage of digital finance. The improvement effect of financial institutions on carbon performance mainly results from resource empowerment. The increase in coverage and usage depth symbolizes the enhanced resource support role of digital finance and promotes the improvement of carbon performance. However, improvements in digitization are more reflected in empowering the development of the financial industry, but the role of digitization in improving carbon performance has not been directly reflected.

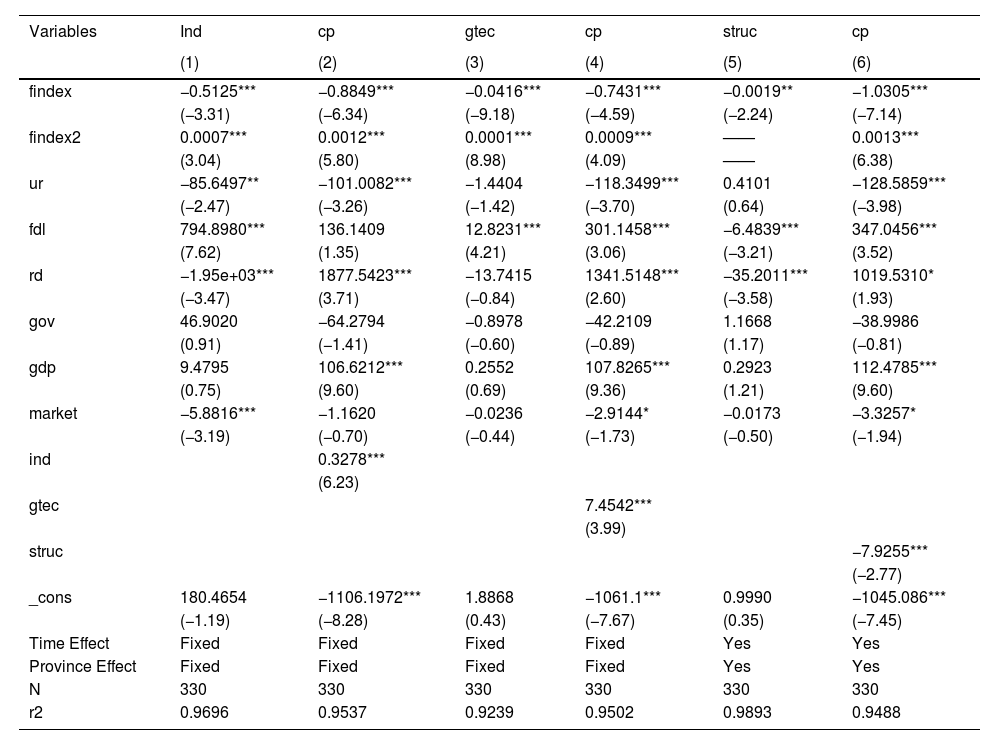

Mediating mechanisms testsReferring to traditional three-step test of Baron and Kenny (1986), we tested whether upgrades in the industrial structure, green innovation, and energy structure improvement play a mediating role in carbon performance improvement. According to Hypotheses 2 and 3, digital finance has a nonlinear effect on technological innovation and industrial structure upgrades. Therefore, a nonlinear model was used for verification, and the results are listed in the first four columns of Table 5. The improvement in the energy structure was rapid and direct, and a linear model was used to test the mediating effect. The results are shown in Columns (5) and (6) of Table 5.

Mediation mechanism regression results.

| Variables | Ind | cp | gtec | cp | struc | cp |

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| findex | −0.5125*** | −0.8849*** | −0.0416*** | −0.7431*** | −0.0019** | −1.0305*** |

| (−3.31) | (−6.34) | (−9.18) | (−4.59) | (−2.24) | (−7.14) | |

| findex2 | 0.0007*** | 0.0012*** | 0.0001*** | 0.0009*** | —— | 0.0013*** |

| (3.04) | (5.80) | (8.98) | (4.09) | —— | (6.38) | |

| ur | −85.6497** | −101.0082*** | −1.4404 | −118.3499*** | 0.4101 | −128.5859*** |

| (−2.47) | (−3.26) | (−1.42) | (−3.70) | (0.64) | (−3.98) | |

| fdl | 794.8980*** | 136.1409 | 12.8231*** | 301.1458*** | −6.4839*** | 347.0456*** |

| (7.62) | (1.35) | (4.21) | (3.06) | (−3.21) | (3.52) | |

| rd | −1.95e+03*** | 1877.5423*** | −13.7415 | 1341.5148*** | −35.2011*** | 1019.5310* |

| (−3.47) | (3.71) | (−0.84) | (2.60) | (−3.58) | (1.93) | |

| gov | 46.9020 | −64.2794 | −0.8978 | −42.2109 | 1.1668 | −38.9986 |

| (0.91) | (−1.41) | (−0.60) | (−0.89) | (1.17) | (−0.81) | |

| gdp | 9.4795 | 106.6212*** | 0.2552 | 107.8265*** | 0.2923 | 112.4785*** |

| (0.75) | (9.60) | (0.69) | (9.36) | (1.21) | (9.60) | |

| market | −5.8816*** | −1.1620 | −0.0236 | −2.9144* | −0.0173 | −3.3257* |

| (−3.19) | (−0.70) | (−0.44) | (−1.73) | (−0.50) | (−1.94) | |

| ind | 0.3278*** | |||||

| (6.23) | ||||||

| gtec | 7.4542*** | |||||

| (3.99) | ||||||

| struc | −7.9255*** | |||||

| (−2.77) | ||||||

| _cons | 180.4654 | −1106.1972*** | 1.8868 | −1061.1*** | 0.9990 | −1045.086*** |

| (−1.19) | (−8.28) | (0.43) | (−7.67) | (0.35) | (−7.45) | |

| Time Effect | Fixed | Fixed | Fixed | Fixed | Yes | Yes |

| Province Effect | Fixed | Fixed | Fixed | Fixed | Yes | Yes |

| N | 330 | 330 | 330 | 330 | 330 | 330 |

| r2 | 0.9696 | 0.9537 | 0.9239 | 0.9502 | 0.9893 | 0.9488 |

(Note: * p < 0.1, ** p < 0.05, *** p < 0.01; T-values for robust standard errors are in parentheses.).

Columns (1) and (3) show the effects of digital finance on industrial structure improvement and green innovation, respectively. Their coefficients of linear and quadratic entries are significantly negative and positive at the 1 % level, and they satisfy the three conditions of the U-shaped curve, indicating that digital finance has the same "first inhibit, then promote" nonlinear effects on industrial structure improvement and green innovation. The regression results presented in Columns (2) and (4) are the results after adding advanced industrial structure and green innovation as explanatory variables, respectively. The main effect of digital finance on carbon performance remains significant at the 1 % level, whereas the regression coefficients of advanced industrial structure and green innovation are significantly positive at the 1 % level, indicating that it played a role in the mediating effect. Columns (5) and (6) indicate that digital finance has improved the energy structure by reducing the proportion of coal consumption and positively impacts carbon performance improvement. Therefore, digital financing can improve carbon performance in the long term by promoting green technological innovation and upgrading industrial and energy structures.

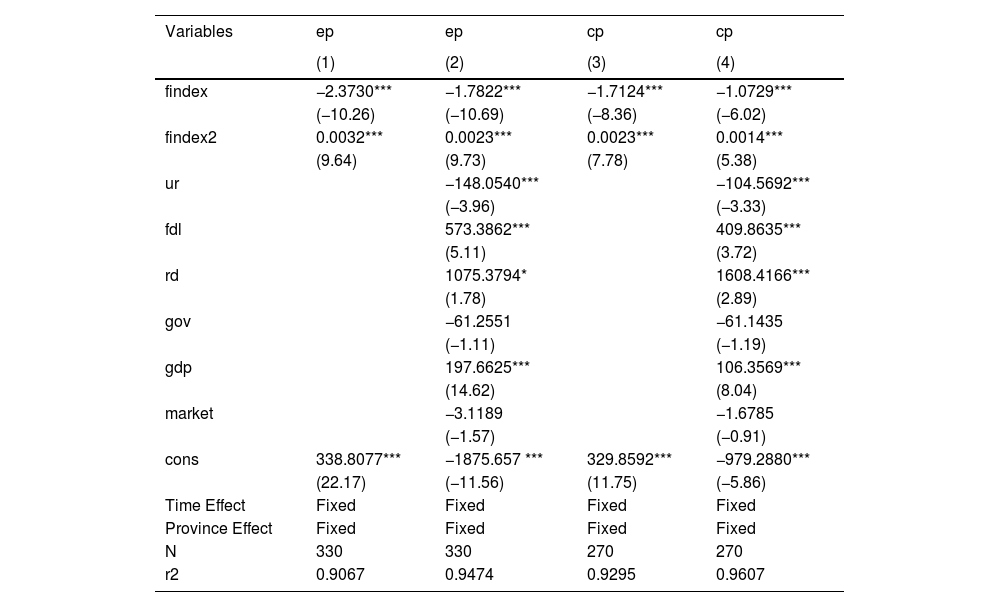

Robustness testIn this study, we replace the core explained variable and shorten the sample period to test the robustness of the baseline regression results. Energy performance is selected as an explained variable to test the model, and the regression results are shown in Columns (1) and (2) of Table 6. The regression results indicate that when energy performance is used as the explained variable, the coefficients of the linear and quadratic terms are significantly negative and positive, the three conditions of the U-shaped curve are satisfied, and the development of digital finance also has a nonlinear effect of "inhibiting first and then promoting" on energy performance.

Robustness test results.

| Variables | ep | ep | cp | cp |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| findex | −2.3730*** | −1.7822*** | −1.7124*** | −1.0729*** |

| (−10.26) | (−10.69) | (−8.36) | (−6.02) | |

| findex2 | 0.0032*** | 0.0023*** | 0.0023*** | 0.0014*** |

| (9.64) | (9.73) | (7.78) | (5.38) | |

| ur | −148.0540*** | −104.5692*** | ||

| (−3.96) | (−3.33) | |||

| fdl | 573.3862*** | 409.8635*** | ||

| (5.11) | (3.72) | |||

| rd | 1075.3794* | 1608.4166*** | ||

| (1.78) | (2.89) | |||

| gov | −61.2551 | −61.1435 | ||

| (−1.11) | (−1.19) | |||

| gdp | 197.6625*** | 106.3569*** | ||

| (14.62) | (8.04) | |||

| market | −3.1189 | −1.6785 | ||

| (−1.57) | (−0.91) | |||

| cons | 338.8077*** | −1875.657 *** | 329.8592*** | −979.2880*** |

| (22.17) | (−11.56) | (11.75) | (−5.86) | |

| Time Effect | Fixed | Fixed | Fixed | Fixed |

| Province Effect | Fixed | Fixed | Fixed | Fixed |

| N | 330 | 330 | 270 | 270 |

| r2 | 0.9067 | 0.9474 | 0.9295 | 0.9607 |

(Note: * p < 0.1, ** p < 0.05, *** p < 0.01; T-values for robust standard errors are in parentheses.).

In 2013, the central bank launched a third-party payment license to promote the development of China's digital finance into a new stage, so the sample interval is shortened to 2013–2021, and then the model is estimated. The regression results are shown in Columns (3) and (4) of Table 6. The development of digital finance on carbon performance has a nonlinear effect of first inhibiting and then increasing and is significant at the 1 % level, which indicates that the research results are robust and reliable. This again verifies the first hypothesis that digital finance has a nonlinear effect of first inhibiting and then promoting improvements in carbon performance.

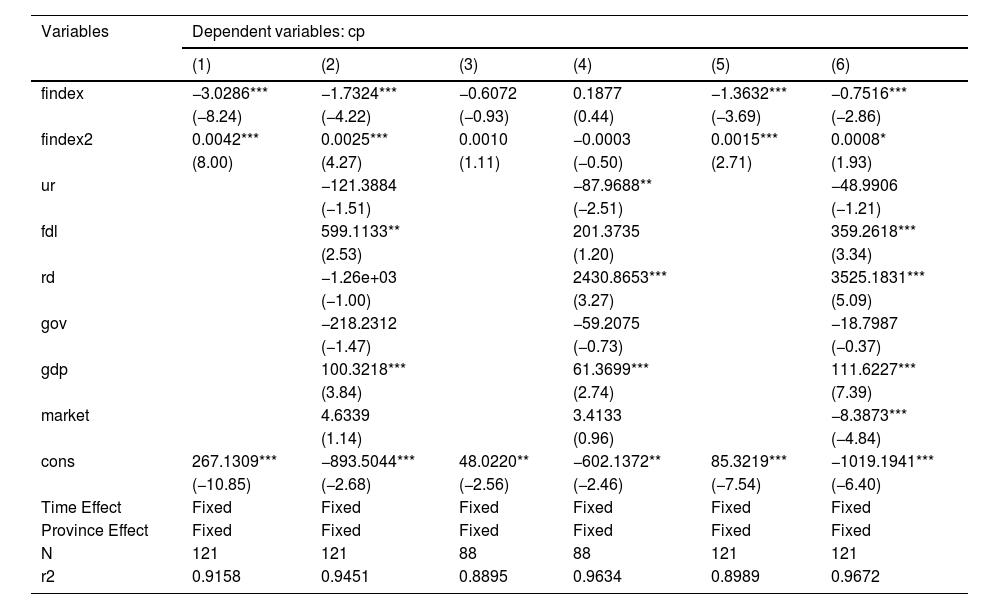

Further discussionSpatial heterogeneity analysisChina covers a vast territory, and the development of digital finance varies greatly in different regions, with obvious regional heterogeneity among the eastern, central, and western regions. Therefore, to more accurately study the impact of digital finance on carbon performance in different regions, the entire sample was divided into three sub-samples of eastern, central, and western regions for analysis. The regression results are presented in Table 7. Columns (1) and (2) show the regression results of digital finance on carbon performance in the eastern region with and without control variables, Columns (3) and (4) correspond to the central region, and Columns (5) and (6) correspond to the western region. The results show that the coefficients of the linear and quadratic entries in the eastern region are significantly negative and positive at the 1 % level and satisfy the three conditions of the U-curve, indicating that digital finance has a nonlinear effect of inhibiting and promoting the improvement of carbon performance in the eastern region. However, the regression results of digital finance on carbon performance in the central region did not pass the significance test. The slope of the right endpoint in the western region was negative and on the left side of the curve and digital finance showed an inhibitory effect on carbon performance.

Results of the spatial heterogeneity analysis.

| Variables | Dependent variables: cp | |||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| findex | −3.0286*** | −1.7324*** | −0.6072 | 0.1877 | −1.3632*** | −0.7516*** |

| (−8.24) | (−4.22) | (−0.93) | (0.44) | (−3.69) | (−2.86) | |

| findex2 | 0.0042*** | 0.0025*** | 0.0010 | −0.0003 | 0.0015*** | 0.0008* |

| (8.00) | (4.27) | (1.11) | (−0.50) | (2.71) | (1.93) | |

| ur | −121.3884 | −87.9688** | −48.9906 | |||

| (−1.51) | (−2.51) | (−1.21) | ||||

| fdl | 599.1133** | 201.3735 | 359.2618*** | |||

| (2.53) | (1.20) | (3.34) | ||||

| rd | −1.26e+03 | 2430.8653*** | 3525.1831*** | |||

| (−1.00) | (3.27) | (5.09) | ||||

| gov | −218.2312 | −59.2075 | −18.7987 | |||

| (−1.47) | (−0.73) | (−0.37) | ||||

| gdp | 100.3218*** | 61.3699*** | 111.6227*** | |||

| (3.84) | (2.74) | (7.39) | ||||

| market | 4.6339 | 3.4133 | −8.3873*** | |||

| (1.14) | (0.96) | (−4.84) | ||||

| cons | 267.1309*** | −893.5044*** | 48.0220** | −602.1372** | 85.3219*** | −1019.1941*** |

| (−10.85) | (−2.68) | (−2.56) | (−2.46) | (−7.54) | (−6.40) | |

| Time Effect | Fixed | Fixed | Fixed | Fixed | Fixed | Fixed |

| Province Effect | Fixed | Fixed | Fixed | Fixed | Fixed | Fixed |

| N | 121 | 121 | 88 | 88 | 121 | 121 |

| r2 | 0.9158 | 0.9451 | 0.8895 | 0.9634 | 0.8989 | 0.9672 |

(Note: * p < 0.1, ** p < 0.05, *** p < 0.01; T-values for robust standard errors are in parentheses.).

This regression result is related to the level of economic development and foundation of digital finance development in each region of China. The economic development foundation of the eastern region is better than that of the central and western regions, and there is a large gap between the regional digital economy development level, industrial structure, green technology, development resources, and other elements. With the accumulated first-mover advantage, the eastern region can realize the optimization of industrial structure and green technological innovation more quickly under the promotional effect of digital finance and, therefore, can play a more significant role in improving carbon performance. The development level of digital finance in the central and western regions is relatively backward. The degree of integration with industry is still relatively low, and the effect of green technological innovation needs to be further developed and highlighted in the future.

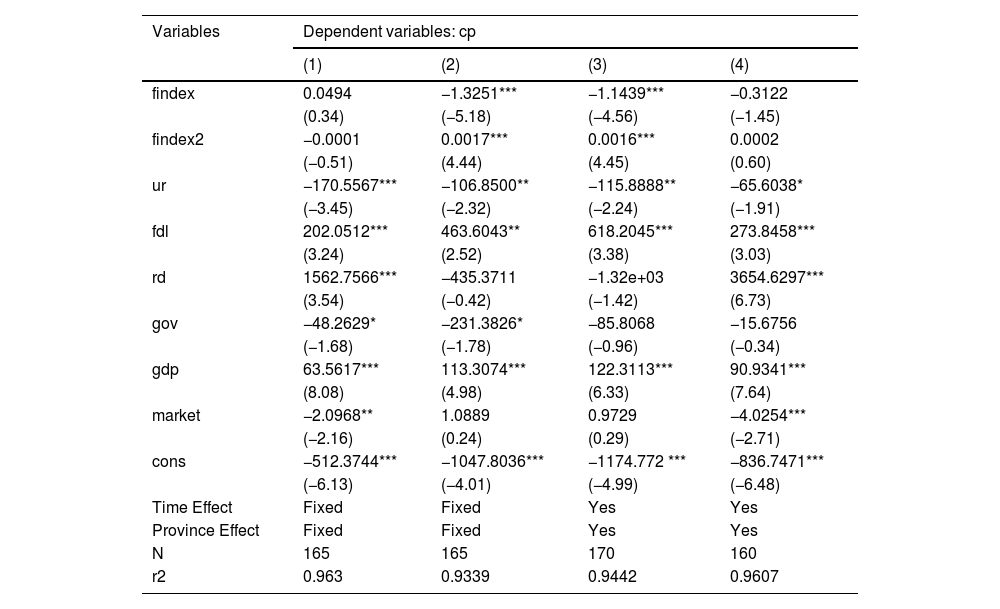

Heterogeneity analysis of the degree of marketThe development of digital finance is influenced by the macroeconomic environment, and the degree of marketization reflects the role of the market in resource allocation, which inevitably affects the functioning of the financial industry. Therefore, the effect of digital finance on carbon performance under different degrees of marketization was analyzed. Columns (1) and (2) of Table 8 are the results obtained from the group test using the Fan Gang marketization index (market), where regions with lower than the median level of regional marketization each year are low-marketization regions, and higher than the median level of regional marketization each year are high-marketization regions. Columns (1) and (2) of Table 8 show digital finance development has a significant inhibitory and incremental effect on carbon performance at a high marketization level, whereas there is no significant effect at a low marketization level.

Heterogeneity analysis based on the degree of market and urban-rural income gap.

| Variables | Dependent variables: cp | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| findex | 0.0494 | −1.3251*** | −1.1439*** | −0.3122 |

| (0.34) | (−5.18) | (−4.56) | (−1.45) | |

| findex2 | −0.0001 | 0.0017*** | 0.0016*** | 0.0002 |

| (−0.51) | (4.44) | (4.45) | (0.60) | |

| ur | −170.5567*** | −106.8500** | −115.8888** | −65.6038* |

| (−3.45) | (−2.32) | (−2.24) | (−1.91) | |

| fdl | 202.0512*** | 463.6043** | 618.2045*** | 273.8458*** |

| (3.24) | (2.52) | (3.38) | (3.03) | |

| rd | 1562.7566*** | −435.3711 | −1.32e+03 | 3654.6297*** |

| (3.54) | (−0.42) | (−1.42) | (6.73) | |

| gov | −48.2629* | −231.3826* | −85.8068 | −15.6756 |

| (−1.68) | (−1.78) | (−0.96) | (−0.34) | |

| gdp | 63.5617*** | 113.3074*** | 122.3113*** | 90.9341*** |

| (8.08) | (4.98) | (6.33) | (7.64) | |

| market | −2.0968** | 1.0889 | 0.9729 | −4.0254*** |

| (−2.16) | (0.24) | (0.29) | (−2.71) | |

| cons | −512.3744*** | −1047.8036*** | −1174.772 *** | −836.7471*** |

| (−6.13) | (−4.01) | (−4.99) | (−6.48) | |

| Time Effect | Fixed | Fixed | Yes | Yes |

| Province Effect | Fixed | Fixed | Yes | Yes |

| N | 165 | 165 | 170 | 160 |

| r2 | 0.963 | 0.9339 | 0.9442 | 0.9607 |

(Note: * p < 0.1, ** p < 0.05, *** p < 0.01; T-values for robust standard errors are in parentheses.).

Improvement in the marketization level means that the market plays a more decisive role and promotes the flow of resource factors. The free flow of resources in the market helps to leverage the role of financial resource allocation and improve resource allocation efficiency. With the continuous improvement in the marketization level, the demand on the supply and consumption sides of the market can be more accurately matched. Digital finance, through the advantages of digital technology, matches suitable investors and alleviates the financing constraints of enterprises, gradually realizing the transformation from scale effect to technology effect. When the degree of marketization is low, the flow of resource elements is insufficient, the degree of information asymmetry is high, and the resource allocation role of digital finance cannot be fully utilized. Enterprises find it difficult to obtain financing in a timely and accurate manner, and the scale and technological effects are difficult to highlight.

Heterogeneity analysis of urban-rural income gapThe imbalance in income distribution between urban and rural areas not only affects the efficiency of economic development and hinders the full flow of resource elements but also has a certain impact on environmental quality. Therefore, drawing on existing research (Sun & Sun, 2016), the Theil index was used to measure the income gap between urban and rural residents, and the effects of digital finance on carbon performance under different urban–rural income gaps were analyzed. The results of the grouping tests using the urban–rural income gap (gap) are shown in Columns (3) and (4) of Table 8. Columns (3) and (4) show that digital finance has a significant inhibitory and then promoting effect on carbon performance when the urban–rural income gap is low but has no significant impact when the urban–rural income gap is high.

When there is a large income gap between urban and rural areas in a region, resources flow to higher-income groups, and rural residents have reduced access to high-quality education opportunities, which is not conducive to the improvement of China's human capital level and further inhibits the development of technological innovation. In addition, when there is a large income gap, insufficient resource flow and an intensified mismatch between urban and rural resources are not conducive to the coordinated development of society and the improvement of production efficiency, which has a negative impact on the improvement of carbon performance. Simultaneously, the income gap between urban and rural areas increases the possibility of pollution transfer from cities to rural areas, making it difficult for urban and rural areas to reach a consensus and cooperate to solve environmental pollution problems, which is not conducive to improving environmental quality. In the case of insufficient factor flow, the role of financial resource allocation is weakened, and the role of digital finance in carbon performance is limited.

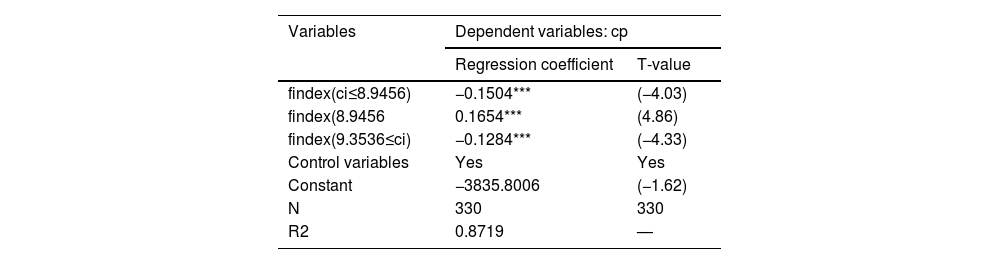

Threshold effect test of carbon emission intensityThe effect of digital finance development on carbon performance may differ at different carbon emissions intensities; therefore, the threshold effect model was applied for further testing. Before conducting the threshold regression, it is necessary to determine whether there is a single threshold effect or multiple thresholds, and the bootstrap method is used to judge whether there is a threshold effect. The results of the threshold effect tests are presented in Table 9. It can be seen that there is a significant double-threshold effect; therefore, the double-threshold effect model was chosen to analyze the empirical model, and the regression results are shown in Table 10.

Estimation results of the panel threshold model.

(Note: * p < 0.1, ** p < 0.05, *** p < 0.01; T-values for robust standard errors are in parentheses.).

As can be seen from Table 10, when ci ≤ 8.9456, digital finance is negatively correlated with carbon performance at the 1 % significance level with an impact coefficient of −0.1504; when 8.9456 < ci < 9.3536, the regression coefficient of digital finance on carbon performance changes from negative to positive with a coefficient of 0.1654 positively correlated at the 1 % significance level, and when 9.3536 ≤ ci, the regression coefficient of digital finance on carbon performance changes to negative again and is significant at the 1 % level. The initial period of low carbon emissions is also characterized by relatively low production efficiency and low overall economic efficiency, and the technical effect of digital finance is difficult to manifest. When carbon emissions exceed a certain threshold, the development of digital finance improves production efficiency and promotes the transformation of advanced industrial structures through the efficiency-enhancing effect. Carbon performance is affected when carbon emissions are too high, distorting the effect of digital finance on carbon performance to some extent.

Research conclusions and recommendationsDigital finance has provided a new direction and has promoted the rapid development of China's financial industry. Achieving carbon peak and carbon neutrality is an inevitable requirement for China's high-quality development; in this context, it is of great practical significance to analyze the relationship between digital inclusive finance and carbon performance. This study examined the effects, mediating mechanisms, and heterogeneity of digital finance development on carbon performance using panel data for 30 provinces from 2011 to 2021.

The following conclusions were drawn: First, the development of digital finance has a nonlinear effect of "inhibiting first and then promoting" the improvement of carbon performance. Among them, the two sub-dimensions of coverage breadth and usage depth of digital performance play a more significant role. Second, digital finance can improve regional carbon performance through the intermediary mechanisms of technological innovation, industrial upgradation, and energy structure improvement. Third, the effect exhibits significant heterogeneity; the higher the level of marketization and the smaller the urban–rural income gap, the more significant the nonlinear effect. The eastern region has the advantage of resources and technology, and the effect in the eastern region is more obvious than compared to the central and western regions. In addition, the role of digital finance in carbon performance varies with carbon levels.

This study has significant theoretical contributions to the environmental benefits of digital finance. Firstly, it explores the role of digital finance on carbon performance based on non-linear thinking, revealing a U-shaped relationship between the two, which is precisely the reason for the inconsistent conclusions of previous research. Secondly, this study enriches the potential mechanisms underlying the impact of digital finance on carbon performance, which re-mains a neglected area in previous literature. By demonstrating that technological innovation, industrial structure upgradation, and energy structure optimization mediate the relationship between digital finance and carbon performance, we reveal the black box. In addition, compared to previous studies, this article analyzes the heterogeneity of the effects of different levels of urban-rural income inequality and marketization, which helps to grasp the key influencing factors and create conditions for digital finance to better promote carbon performance.

Based on the above analyses and conclusions, this study provides the following policy suggestions. First, the development of digital finance has both an inhibitory and promoting effect on carbon performance. Therefore, measures should be implemented at different developmental stages to promote carbon performance. In the early stages of digital finance development, attention should be paid to guiding enterprises to expand their scale reasonably and reduce the expansion of high-energy-consuming industries. Simultaneously, incentivizing green technological innovation in enterprises through resource allocation promotes the transformation from a scale effect to a technological effect. In the later stages of development, we should be guided by high-quality development goals supported by green technology, improve top-level design, fully leverage the role of digital finance, and promote the achievement of the carbon peak and carbon neutrality goals.

Second, digital finance should leverage its resource endowment advantages, consciously promoting low-carbon development in China. It should actively provide services for green and highly efficient enterprises and stimulate regional green technology innovations. Simultaneously, it should encourage the development of emerging industries, cultivate high-value-added industries, and promote industrial transformation and upgrades. In addition, it should encourage enterprises to use clean energy, improve energy efficiency, optimize energy structure, and promote the achievement of carbon peak and carbon neutrality goals.

Third, there was significant heterogeneity in the effect. The improvement of the marketization level and narrowing of the urban–rural income gap is conducive to the improvement of carbon performance, and the creation of conditions for digital finance to promote carbon performance should be encouraged. Simultaneously, strategies need to be formulated according to local conditions in response to differences in economic foundations and resource endowments. The eastern region of China has a first-mover advantage and a high level of digital finance development. Digital finance should be fully utilized to actively promote low-carbon development. The level of digital finance development in the central and western regions is relatively low. We should strengthen policy support for the development of digital finance in the central and western regions, promote the improvement of relevant infrastructure, and enhance the strength of digital finance.

This study has several limitations. First, the generalization of this study is limited by background factors. China is a rapidly developing digital economy and the second-largest developing country in terms of global carbon emissions. The conclusions of this study may not apply to other developed economies with slow development rates. In the future, studying the impact of digital finance on carbon performance can help examine the impact of digital finance development on carbon performance in Western countries to explain the consequences of digital finance more comprehensively. The second limitation is related to the impact mechanism. This study only investigated the mechanisms of industrial structure upgrading, energy structure improvement, and green technology innovation. Future research could focus on other channels through which digital finance affects carbon performance and further expand our understanding of how digital finance affects carbon performance.

CRediT authorship contribution statementBing Zhou: Conceptualization, Formal analysis, Methodology, Software, Writing – review & editing. Yu-Lan Wang: Data curation, Investigation, Resources, Writing – review & editing. Bin-Hu: Data curation, Formal analysis, Investigation, Project administration, Supervision.