The aim of this study was to evaluate the attitude of Iranian auditors toward balance between auditing and marketing with respect to two important components of audit process such as business environment of auditing and corporate governance. The analysis is based on survey data from 257 respondents. To achieve the research aims, we specified four hypotheses based on social theories. The results of this study show that the auditors having positive attitude toward marketing and those who consider it as significant are able, to a large extent, balance spent time for inherent auditing tasks and marketing activities. In addition, the results show that an increase by a unit for the attitude toward business environment results in 0.489 unit increase in attitude toward balance of time spent on marketing and auditing activities, of which 0.396 is direct impact and 0.093 is indirect impact.

El objetivo de este estudio consiste en evaluar la actitud de los auditores iraníes hacia el equilibrio temporal entre la auditoría y el marketing con respecto a dos importantes factores del proceso de auditoría, es decir, el entorno empresarial de auditoría y el gobierno corporativo. El siguiente análisis está basado en datos obtenidos por medio de encuestas a 257 personas. A fin de alcanzar los objetivos de la investigación, se especificaron cuatro hipótesis basadas en teorías sociales. Los resultados de este estudio muestran que los auditores que tienen una actitud positiva hacia el marketing y los que la consideran significativa son capaces, en gran medida, de mantener un equilibrio entre el tiempo dedicado a las tareas inherentes de auditoría y las actividades de marketing. Además, los resultados demuestran que, si se cambia una unidad, la actitud hacia el entorno empresarial da como resultado un aumento de 0.489 unidades en la actitud hacia el equilibrio del tiempo dedicado a actividades de marketing y auditoría, de los cuales 0.396 es impacto directo y 0.093 impacto indirecto.

Owing to the nature of activities of audit firms, they have always been in the judgment position and have always being mixed with concepts such as justice, fairness and independence. So, professional behavior regulations in several countries have prohibited auditors from advertising their abilities and reputation while maintaining independence so as to obtain a larger share in the market. Nevertheless, by comparing auditors’ tendencies for marketing in 1993 with year 2004, Clow, Stevens, Mconkey, and Loudon (2009) revealed that negative perceptions of auditors toward marketing has turned into positive tendencies. This change in auditors’ tendency toward marketing was intensified via more usage of marketing activities and auditors enhanced their relationships with clients.

According to agency theory, auditors in explaining their relationship with other stakeholders should consider the interests of all, and even their own interests. Thus if marketing process, that is the subject matter of this study is able to continue the same concept, audit marketing is not prohibited only from the standpoint of agency theory, but it leads to the business development of auditors and as a result, reduction of their dependence on a specific client, which will lay the ground for increasing auditing quality. Emphasis on good corporate governance can have an impact on the enhancement of the relationship as well. Given that the quality of financial reporting is effective on strengthening corporate governance mechanisms (Kent & Stewart, 2008), it seems that this issue potentially affects the auditor's decisions and judgments in various stages of audit work and vice versa. Moreover, based on the transaction cost theory, if we consider the audit firms as commercial-profit entities, via business development, then involvement of more actors in the business and ultimately increasing audit firms, the necessity to determine the fees by institutions is felt more than ever. This is because in a healthy world of competition, the institutions should determine the fees, although there might be a risk of breaking the risk, which can also be partly compensated via full and adequate supervision on the quality of audit work.

According to the theory of stakeholders, issues like corporate governance, corporate social responsibility and audit marketing are closely related to each other. Positive attitude toward social responsibility implies positive attitude to proper exposure and implementation of corporate governance mechanisms. In such circumstances, it is evident that with a positive faith to corporate governance mechanisms, the auditors can effectively meet the interests of all stakeholders, and of course the double-edged sword of audit marketing can be in accordance with the interests of all stakeholders. In other words, if based on a stakeholder's theory, we respect social responsibility on behalf of the client or the auditor, and then we can control and manage different behaviors of different stakeholder groups.

Auditing is a social phenomenon and has emerged in response to the perceived need of the groups that are looking to learn about the behavior of others (Flint, 1988, p. 14). Theory of Reasoned Action, presents a model for predicting the behavioral concepts that involve predicting the individual's attitudes and behavior. Investigating the consequences of behavioral concepts leads to understanding the type of attitude to specific issues (Ajzen & Fishbein, 1980, p. 52). Other social theories like Parsons’ Social Action Theory have discussed the quality of relationship of different actors of society. With regards to the changing nature of accounting and auditing in line with what Fogarty has proposed and on the basis of Parsons Theory of social action, the structure and function of auditing in the law and legal field must be revised. Changes in the nature of a profession need to be considered because of relationship with other social structures in the subject of legislation and judgments. Since the actors of each function are intimately linked. That was followed until in 1997, when the US Supreme Court in Arizona approved a law based on which professional organizations could no longer prohibit their members from carrying out their advertisement. Today, advertising and marketing are also taken into consideration as factors that could provide structure and functions for interaction between the auditor and client.

Carrying out research in the field of marketing based on social approach in Iran, a country with a high degree of bureaucracy and lack of high transparency, is deemed necessary more than ever, because the improper distribution of benefits results from the lack of transparency. This issue affects all pillars of the society, including auditing profession. Nevertheless, research in the field of auditing as a professional service and its relationship with marketing has started some decades ago, and it is thought that it is a reaction to changes occurring in the business environment. Investigating this relationship is usually done in one of the two ways: Some studies dealt with the evaluation of the changes in the attitude and tendency of auditors in line with marketing activities (Arel, 2012; Cameran, Moizer, & Pettinicchio, 2010) and some others focused on the auditors’ marketing activities (Francis, 2011; Hsu & Sakai, 2009). Prior to 1977, marketing in accounting was considered as an immoral action and auditing advertisement was in violation of the professional code of ethics, but increasing competitive pressures in the US helped auditors to realize the importance of marketing (Broberg, Umans, & Gerlofstig, 2013). Therefore, it seems that explaining attitudes and perhaps modifying auditors’ perspective toward marketing and its relationship to the duration of auditing activities and a creation of balance between professional responsibilities and auditing activities, could enhance the declining quality of audit. Given that the end product of audit is the auditor's report in which he states his opinion in relation to the financial statements, this issue brings this in mind that the audit report represents a combination of auditor's effort and judgment in relation to the whole work of audit (Pratt & Peursem, 1993).

Background and hypotheses developmentBusiness environment of auditingThere are factors within the scope of the audit firms discussed in the study as factors that affect the business environment of auditors. Evaluation of external factors influencing the auditing profession market indicates that the audit firms have less competitive power in the governmental economy. With the expansion of government body and increase in its tenure, job referral to the audit firms reduces. Audit firms in Iran, which have a government with large economic size, lack a good economic position, because in such circumstances, the auditor is imposed and agreed and the audit firms are competitive in a small part where an open economy is ruled and where they are under the pressure of crises and also do not have adequate protection. So, a difficult working condition prevails on them. Poor implementation of laws in the country is one of the most important problems of the audit firms that have affected services market. Nevertheless, issues related to the internal control structure of audit firms also contributed to their problems in optimum implementation of audit.

In previous studies, branding was considered as a factor that can be reasonably attributed as a logical step for the business development based on the theory of action. Regarding branding in the audit firms, Caragber (2013) suggests that branding is possible with investment on money and time. He believes that branding leads to positive differentiation when compared to other auditor institutions. He also believes that marketing plan, workforce development, and survival efforts are consequences of branding. Therefore, explaining tenured accountants’ attitudes on the audit issue from the perspective of brand can be an instrument for a more positive look to other important related issues like marketing. This will not be achieved unless one obtains some information about their attitude to topics like audit business environment and corporate governance structure. Finally, awareness of the above items can lay the ground to take the necessary steps to define the logical relationship based on maintaining independence – important factor of the quality of audits – between auditor and clients. Identification of the recipients’ model of audit services can have a positive impact on the relationship between the auditor firms and the client.

Corporate governance and auditing marketingThe purpose of many corporate governance mechanisms is to achieve responsible and responsiveness companies, value creating managers and ultimately controlling the companies. In other words, rules of corporate governance have developed owing to possible conflict resolution between the interests of shareholders, employees and managers in the international market (Malekian & Daryaei, 2012, p. 123). By explaining their relationship with the company by raising audit quality, while maintaining their independence with specific marketing activities, auditors as a part of external mechanisms of corporate governance can be effective in enhancing corporate governance mechanisms by decreasing their cost of actions and by indirectly decreasing agency costs and increasing stock price of the client company. This implies that the attitude of auditors to audit activities and marketing can be influenced by their perspective to corporate governance regulations. To decrease client costs, the auditors agree on not implementing a part of the corporate governance mechanisms, so that in this way, they convince their client on the audit costs. This threatens the interests of other stakeholders. Therefore, there can be a significant relationship between the attitude of auditors to audit activities in general and marketing activities in particular and their attitude toward the implementation of corporate governance.

According to “actor-network theory”, Marketization of Accountancy is concerned with the necessity emanating from a system of tools and experience sharing and partnerships. Marketization of accountancy may be considered as a natural process in marketing science in the first place. Nevertheless, the audit market as a two-sided fraud can be defined in two ways: the first is “union of heterogeneous actors” around an awareness which results in a doubt. The second is the legitimacy of a natural process where marketing researchers initially have concluded and described it via documentation (introduction and integration of specialized marketing) (Picard, 2016, p. 3). So, marketing and marketization are a necessity, and before answering the question that “whether marketing is necessary or not?” One must seek answer to the question “how to carry out marketing for audit process?”

Given the importance of the marketization and marketing, the academics should ask themselves about their participation in the process of marketization. This cultural change does not only affect the auditors employed in audit firms. Audit students also will tend more toward neo-liberal discourse, a discourse that promotes individualism and individual economic interests. Since universities have become a form of entrepreneurial business company, students idealism for activities in line with the public interest have fallen sharply (Picard, 2016, p. 17). When universities are evidently and increasingly moving toward commercializing, the trend toward personal economic interests finds a high legitimacy and is reinforced. Therefore, instead of training professionals committed to public interest, universities train specialists that have commercial concerns (Hanlon, 2004, p. 190). Based on what was discussed earlier, Picard (2016) quite extremely believes that for academics to foster the values of public interest among the students, they should try to avoid market discourse in classrooms and commercialization auditing (and marketing) (Picard, 2016, p. 17). This is while the audit market and consequently marketing is a complex and multifaceted phenomenon, where different factors and stimuli within the audit profession and the entire community affect it. Nevertheless, explaining social theories help to further understand the social role of auditors and determination of the narrow lanes between the auditors and the marketing and even marketization.

Social theoriesTheory of reasoned actionTheory of reasoned action provides a model for predicting behavioral concepts which includes predicting the individual attitudes and behaviors. Investigating the consequences of behavioral concepts leads to understanding the type of attitude toward specific issues (Ajzen & Fishbein, 1980, p. 52). Theory of reasoned action was developed by Ajzen and Fishbein (1980). Their research follows previous research on the theory of attitude. The roots of this theory should be probed in the field of social psychology. A model developed by Fishbein and Ajzen (1975), explains the relationship between beliefs, attitudes, norms, intents and treatment of individuals. They have explained the intellectual norms like the perception of the individuals, based on which many people refuse to carry out behaviors related to them (Fishbein & Ajzen, 1975, p. 302). Theory of reasoned action is summarized as: Behavioral Intention=Attitude+Subjective Norms. This model suggests that external stimuli lead to a tendency to modify the person's belief structure. Beliefs in the personal domain can affect their performance in the society.

Theory of reasoned action believes that individual behavior is derived from the acquired concepts. In other words, intention to carry out a behavior in an individual is attributed to his attitude to the norms. Consequently, increased competition is the result of the increasing number of audit firms, and specialization of audit activities is the result of the increased attitude toward competitiveness of the audit market for business development. This kind of competition will increase the desire to enter into various methods of audit marketing (Heischmidt, Elfrink, & Mays, 2002, p. 63). In addition, based on the theory of reasoned action, this could be attributed to the attitude of auditors toward the issue of corporate governance. This is because using or ignoring subjective norms of corporate governance affects the behavior of auditors. Therefore, attitude to corporate governance is effective on the attitude to audit marketing, because marketing is a commercial behavior (Mitra & Lynch, 1995, p. 649). Audit activities, rather than being based on personal interests should be based on the consent of all stakeholders. This requires that auditors in some cases take measures that appear to be incompatible with their basic duties, but correct understanding of their auditor's position can be justifiable based on the theory of reasoned action. Auditors are those whose professional activities, although apparently associated with personal affairs between themselves and the client, the social effects of their activities are evident to all. For instance, several factors such as entrepreneurship, economic environment, audit activities, gender and other personal characteristics affect the attitude of auditors to perform the audit process (Popescu, Popescu, & Popescu, 2015; Tremblay & Malsch, 2016), however, what is important is the way by which the intellectual basis of auditors toward society is made and that as a part of the society, they should make their logical behavior in accordance with the interests of others.

In an environment where the auditors activate internal and external factors affecting them and their clients, one of the most important factors is corporate governance mechanisms. Theory of reasoned action provides a model for explaining the relationship between attitudes toward audit marketing and corporate governance. This theory distinguishes between human behavior as part of the international community and a rational person with local perspectives. This issue justifies the difference between the behavior of local and international auditors. This theory also predicts the mutual attitudes between the type of attitude toward audit marketing and corporate governance. Based on the theory of reasoned action, when the development of the industry, international business operations, continuous changes in accounting and auditing standards and most importantly the entry of new audit firms are an essential part of the auditing profession, auditors must take reasonable measures to preserve their legitimate interests.

Independence is one of the intrinsic properties of the auditors’ (Chan & Wu, 2011, p. 201; Cohen, Gaynor, Krishnamoorthy, & Wright, 2011, p. 672–656). Independence is a belief and may affect the auditor's judgment. The incentive to compete with other auditors, avoiding loss of market and regulatory requirements may affect the behavior of business auditors (Solomon & Solomon, 2004). We cannot just avoid the logical and appropriate measures owing to the fact that the auditors’ independence features might be threatened. One of these logical measures is the development of marketing activities by auditors. Based on the theory of reasoned action, belief in the audit marketing alongside auditor independence may lead to some actions and avoidance of some others. The combination of these two approaches will result to rational behavior in the interests of all stakeholders. Creation of time balance between marketing and audit activities in business environment of auditors-where corporate governance rules prevail-can be considered as a test to observe the theory of reasoned action. So, in this study, the theory of reasoned action is tested for Iranian Certified Accountants for which the following relevant hypotheses were developed.

Parsons’ social action theoryPrevious studies on the balance between the interests of all stakeholders have revealed that a lack of clear conceptual framework is one of the main issues regarding the attitude and consequently the behavior of auditors (Broberg et al., 2013). Nevertheless, in other areas of the social sciences like sociology, many people are seeking to provide a conceptual framework for relationship between the people. One of these men was Parsons. According to Parsons, social action is the subject of all human science studies and since in the view of Parsons, the concept of system is very important for the scientific knowledge, he believes in the ability of systems analysis for human action (Roche, 1998, p. 53).

Marketing near consumer needs and characteristics of the product or service provided by the seller plays a significant role that is entwined with issues like advertising and pricing. These two factors, i.e., the seller and the buyer are related together in economic structure with functions like marketing. The basic question is whether the auditor and the client are closed together with the marketing process, or due to disruption of some inherent properties of auditor such as independence, the parties are damaged. According to Parsons's theory of social action, the auditors should be able to create a balance between their needs and that of others. The role of personality traits of auditors or even their gender can affect their performance (Alavi Tabari, Mojtahed Zadeh, & Bakhtyari, 2012; Tremblay & Malsch, 2016).

Parsons separates family roles based on gender and believes that the acquisition of skills and expertise in family roles should inevitably vary according to the natural and potential talents of members, and its difference is driven from specific physical and mental structures of both sexes (Roche, 1998). First the family, society in general and the economic community in particular is affected by attitudes of women. Women, owing to substantial differences with men may have different attitudes and behaviors when compared to men in the same situation. Conducting audit as economic performance as part of the society is no exception to this general rule. Therefore, asking about the gender respondents to assess their attitudes in this study was also based on these concepts.

What happens when the company loses its whole property? Who do shareholders believe to be responsible for the cause of this incident? What is the role of auditors in preventing the occurrence of such an incident? These are the questions all stakeholders of a company are seeking answer for. Based on the writings of Parsons, there is only one convincing answer and that is the formation of an improper structure and consequently a poor performance. In response to this poor performance and structure, and strengthening the relationship between the company and other stakeholders, corporate governance has received a lot of attention in recent years (Black, Love, & Rachinsky, 2006; Cornett, Marcus, & Tehranian, 2008). Positive attitude toward corporate governance will lead to facilitation of relationships between stakeholders of a company and thus proper performance. Nevertheless, investigating research on attitudes to corporate governance, responsibility and social accountability audit market can help in explaining the unexplored dimensions of the above problem. According to Parsons's theory of social action, it is important to determine the optimal relationship between the auditor and the client. This is carried out by investigating the attitude of auditors toward professional activities.

Auditor industry specialization, experience and entrepreneurshipSarwoko and Agoes (2014) have demonstrated that auditor specialization in industry is effective on the audit procedures to detect fraud in financial audit and high quality audit. This is because the deep understanding and long experience in a particular industry of client on business process, business risk and the risk of material misstatement play a crucial role in the financial statements. The ability of the auditor in such specific areas of the client enables him to choose and implement effective audit procedures to detect important fraud cases that lead to an increase in audit quality (Sarwoko & Agoes, 2014, p. 280). Dao and Pham (2014) sought to answer the question whether the auditor tenure has any effect on the delay of audit report and whether the auditors specialized in this respect, have a modulatory role or not. In addition, there has been a special emphasis on timely financial information. They based their theoretical basis discussions on rotation of auditors and increasing demand for high quality auditors. The results demonstrated that there is a significant negative relationship between auditor tenure and audit report delays. The specialized auditors also confirmed the moderating role of the relationship between auditor tenure and audit report delays (Dao & Pham, 2014, p. 490). In addition, Yuan, Cheng, and Ye (2016) examined the relationship between business strategy of the clients and audit quality resulting from the work of specialized auditors in the industry. Their sample was Chinese companies for the years 2000 to 2010. The results demonstrated that there is a significant negative relationship between industry professionals and discretionary accruals of the client. In other words, the expertise of auditors in a specific industry will enhance financial performance of the clients and greater transparency of financial statements. Nevertheless, the present study has emphasized the interference of the client's overall strategy with audit procedures of the expert that may affect audit quality.

Because younger auditors are replaced by experienced auditors, tendency toward marketing will change and this is obvious in the performance of auditors. Conflict between auditors as professional services and marketing is not so evident. Research findings indicate that auditors create a balance between audit responsibilities and imposed marketing activities. Other studies deal with ways of improving the auditing profession, which requires accepting marketing as an important part of professional services. Furthermore, previous research has pointed to the fact that the notion of different activities among the auditing profession depends on the age of auditors (Clow et al., 2009). Alissa, Capkun, Jeanjean, & Suca (2014) concluded that there is a significant positive relationship between auditor characteristics and their performance. They studied 15,392 tax auditors in their study. Their research demonstrated that the auditor's experience as one of the auditors’ acquired characteristics can decrease the complexities of the audit work. This implies that in dealing with audit activity problems, the auditors’ choose the lowest-cost solution based on their experience. In addition, the efforts of auditors has a direct and significant relationship with the performance of auditors, and this relationship is under the influence of intervening variables related to the characteristics of the auditor.

Another important feature of auditors which may be related to their performance is entrepreneurship. Entrepreneurship and audit activities will result to the development of humanity over a long period. Audit plays a significant role in improving and increasing the transparency of the business environment, especially since ancient times when ways to better manage assets has been known. Today, accounting and auditing are basically proposed as a science that is undergoing evolution even after thousands of years. The term “audit” originates from the word listening in Latin, nevertheless, audit was widespread in the Assyrian and Egypt times. Homocianu and Airinei (2014) in a study titled “Facilities of the intelligence business and its application at audit and financial reporting” demonstrated that the dynamics and responsibility of financial auditors in the role of experienced and professionals entrepreneurs can meet the essential need of each company to provide fair financial reporting and commenting in line with regulatory frameworks that investors, creditors, government and people can take advantage. The results of their study demonstrated that the need to provide services that should have a high level of objectivity, will force audit firms to benefit from entrepreneur auditors. In line with the professional and ethical requirements, entrepreneurial auditors will design and implement the audit work in order to further increase trust to the content of reports (Homocianu & Airinei, 2014, p. 4).

Financial audit is the real meaning of an entrepreneur. His own fate and that of his client is in his hands. Owing to the independence needed for his work, the professional and ethics codes requires that he differ from company employees for whom one audits. Their results demonstrated that with an increase in competing auditors, the marketing process to introduce the capabilities and advantages of auditors in Romania is based on this topic that by attracting auditor entrepreneurs, one can obtain a good share of audit market. Entrepreneur auditors were determined based on questionnaires and interviews (Popescu et al., 2015, p. 230).

Given the theoretical and empirical evidence, our hypotheses regarding balance time and nature of the relationship between the auditors and clients are specified as follows:

H1: There is a significant difference between the attitude of younger auditors and others toward marketing activities in the balance time between auditing and marketing.

H2: There is a significant relationship between business environment and balance time between auditing and marketing.

H3: There is a significant relationship between perceived balance time between marketing activities and the inherent tasks of auditing and attitude toward corporate governance mechanism.

H4: Attitude toward business environment has effects on attitude toward balance between auditing and marketing via attitude toward corporate governance mechanism.

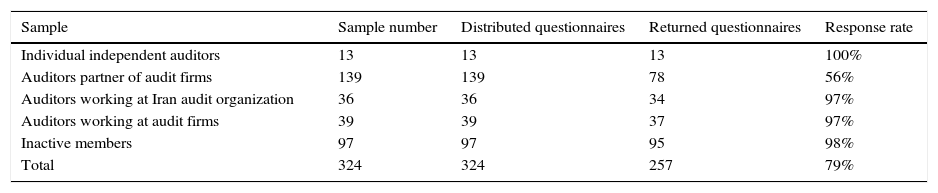

The sample comprised Iranian Association of Certified Public Accountants (IACPA) that was calculated by Cochran's sample size formula. Thus, the analysis is based on survey data from 257 respondents. Although there's no standard rate of questionnaire return for research but return rate less than 70% increases the risk of acceptance and generalization of results and if the rate of return was on the risk range, then more questionnaires can be distributed to move out of this range (Dillman, Smyth, & Christian, 2009). The number of questionnaires distributed, received and returned is presented in Table 1.

Sample number, distributed questionnaires, returned questionnaires, and response rate.

| Sample | Sample number | Distributed questionnaires | Returned questionnaires | Response rate |

|---|---|---|---|---|

| Individual independent auditors | 13 | 13 | 13 | 100% |

| Auditors partner of audit firms | 139 | 139 | 78 | 56% |

| Auditors working at Iran audit organization | 36 | 36 | 34 | 97% |

| Auditors working at audit firms | 39 | 39 | 37 | 97% |

| Inactive members | 97 | 97 | 95 | 98% |

| Total | 324 | 324 | 257 | 79% |

The present study is one of the types of survey research. Surveys represent one of the most common types of quantitative, social science research. In survey research, the researcher selects a sample of respondents from a population and administers a standardized questionnaire to them. In building the questionnaire, we relied as far as possible on instruments validated in previous studies. In addition, we pre-tested the survey instrument by asking many experts to complete the questionnaire and to discuss their experiences with us. This led to some minor adjustments in the original survey design. The relevant parts of the questionnaire are reproduced in Appendix A. To collect data for hypotheses testing, this study used a questionnaire adapted from the studies of Broberg et al. (2013), Biech (2007), in addition to literature review and document analysis.

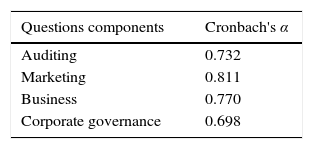

Our observations include data from individual independent auditors (4%), auditor's partner of audit firms (43%), auditors working at Iran audit organization (11%), auditors working at audit firms (12%), and inactive members (30%). The respondents marked their opinion on a 7-point Likert scale ranging from “strongly disagree/not at all important/no time at all” (1) to “strongly agree/very important/a lot of time” (7) for each of the activity. Cronbach's Alpha is a tool for the assessment of the reliability of scales. Cronbach's Alpha is an index of reliability associated with the variation accounted for by the true score of the “underlying construct.” Construct is the hypothetical variable that is being measured (Hatcher, 1994). Alpha coefficient ranges in value from 0 to 1 and may be employed to describe the reliability of factors extracted from dichotomous (that is, questions with two possible answers) and/or multi-point formatted questionnaires or scales (i.e., rating scale: 1=poor, 7=excellent). Nunnaly (1978) has indicated 0.7 to be an acceptable reliability coefficient but lower thresholds are sometimes employed in the literature.

We performed our analysis by applying a binary Probit regression. Furthermore, given that in the comparison of two samples’ coefficients such as Fisher (1921), it was necessary to determine Z-statistic. In the present study to compare the relationship between dependent and independent variables in a community with other independent community, Z-statistic was used as follows:

Finally, we hypothesize that the manner in which attitude toward business environment are being used affects perceived balance between marketing activities and the inherent tasks of auditing, and that attitude toward business environment depends on attitude toward corporate governance mechanism.

VariablesBt: was created by subtracting the average scores for all auditing activities from the average scores for all marketing activities. We employed a dummy variable coded one if the balance time was higher than average scores and zero if otherwise.

CG: was created by questionnaire. We utilized a dummy variable coded one if the CG was higher than average scores and zero if otherwise.

Attitutem: Auditor's attitude toward marketing, utilized as an independent variable, was operationalized as an index of the average scores for all the marketing activities in the attitude section of the questionnaire. The scores were added for each of the respondents, and the sum was divided by the total number of activities.

Attitutea: Auditor's attitude toward auditing, employed as an independent variable, was operationalized as an index of the average scores for all the auditing activities in the attitude section of the questionnaire. The scores were added for each of the respondents, and the sum was divided by the total number of activities.

Importanta: Auditor's view on the importance of auditing, utilized as an independent variable, was operationalized as an index of the average scores for all the auditing activities in the important section of the questionnaire. The scores were added for each of the respondents, and the sum was divided by the total number of activities.

Importantm: Auditor's view on the importance of marketing, applied as an independent variable, was operationalized as an index of the average scores for all the marketing activities in the important section of the questionnaire. The scores were added for each of the respondents, and the sum was divided by the total number of activities.

Speciality: Speciality was measured as a dummy variable and was coded 1 if auditors were specialist and 0 if otherwise.

Entrepreneurship: The entrepreneurship was constructed based on 22 questions relating to different entrepreneurship practices.

Ex: It was created by questionnaire. We employed a dummy variable coded one if the balance time was higher than average scores and zero if otherwise.

Gen: We classified respondents into male or female and we coded female as 0 and male as 1.

Edu: We classified respondents into BA or upper and we coded BA as 0 and upper as 1.

Business: The business was constructed based on 9 questions relating to business environment practices.

In this study, Cronbach's α was calculated for auditing, marketing, corporate governance, and business environment components. The results are presented in Table 2.

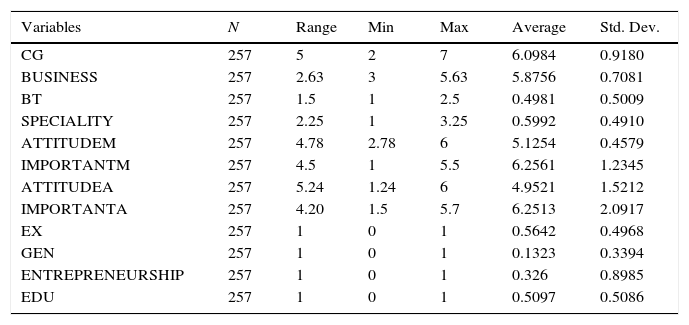

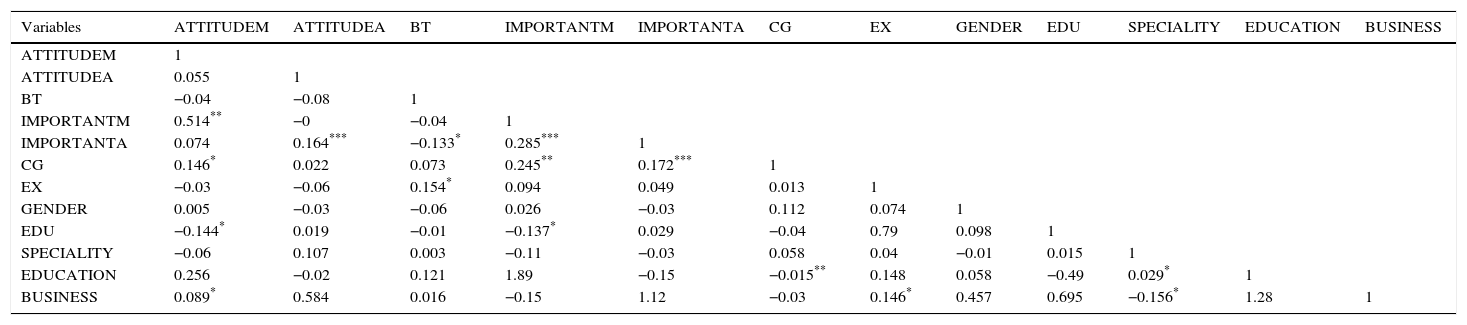

ResultsDescriptive statisticsTable 3 shows summary statistics for each variable, and Table 4 presents the correlation matrix. From these tables, the numbers given in Table 3 indicate that there is no high deviation among subjects’ opinions. The equal attitude toward corporate governance and business environment shows that as one of them improves, so does the other. The mean binary variable of time balance between marketing and auditing activities that is equal to 0.49 shows that there is a balanced attitude toward auditing and marketing activities. The mean gender variable, which equals 0.13, demonstrates that there is no desirable balance between subjects’ gender. Further investigation clarifies that the number of male subjects is higher than that of females.

Descriptive statistics.

| Variables | N | Range | Min | Max | Average | Std. Dev. |

|---|---|---|---|---|---|---|

| CG | 257 | 5 | 2 | 7 | 6.0984 | 0.9180 |

| BUSINESS | 257 | 2.63 | 3 | 5.63 | 5.8756 | 0.7081 |

| BT | 257 | 1.5 | 1 | 2.5 | 0.4981 | 0.5009 |

| SPECIALITY | 257 | 2.25 | 1 | 3.25 | 0.5992 | 0.4910 |

| ATTITUDEM | 257 | 4.78 | 2.78 | 6 | 5.1254 | 0.4579 |

| IMPORTANTM | 257 | 4.5 | 1 | 5.5 | 6.2561 | 1.2345 |

| ATTITUDEA | 257 | 5.24 | 1.24 | 6 | 4.9521 | 1.5212 |

| IMPORTANTA | 257 | 4.20 | 1.5 | 5.7 | 6.2513 | 2.0917 |

| EX | 257 | 1 | 0 | 1 | 0.5642 | 0.4968 |

| GEN | 257 | 1 | 0 | 1 | 0.1323 | 0.3394 |

| ENTREPRENEURSHIP | 257 | 1 | 0 | 1 | 0.326 | 0.8985 |

| EDU | 257 | 1 | 0 | 1 | 0.5097 | 0.5086 |

Correlations.

| Variables | ATTITUDEM | ATTITUDEA | BT | IMPORTANTM | IMPORTANTA | CG | EX | GENDER | EDU | SPECIALITY | EDUCATION | BUSINESS |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ATTITUDEM | 1 | |||||||||||

| ATTITUDEA | 0.055 | 1 | ||||||||||

| BT | −0.04 | −0.08 | 1 | |||||||||

| IMPORTANTM | 0.514** | −0 | −0.04 | 1 | ||||||||

| IMPORTANTA | 0.074 | 0.164*** | −0.133* | 0.285*** | 1 | |||||||

| CG | 0.146* | 0.022 | 0.073 | 0.245** | 0.172*** | 1 | ||||||

| EX | −0.03 | −0.06 | 0.154* | 0.094 | 0.049 | 0.013 | 1 | |||||

| GENDER | 0.005 | −0.03 | −0.06 | 0.026 | −0.03 | 0.112 | 0.074 | 1 | ||||

| EDU | −0.144* | 0.019 | −0.01 | −0.137* | 0.029 | −0.04 | 0.79 | 0.098 | 1 | |||

| SPECIALITY | −0.06 | 0.107 | 0.003 | −0.11 | −0.03 | 0.058 | 0.04 | −0.01 | 0.015 | 1 | ||

| EDUCATION | 0.256 | −0.02 | 0.121 | 1.89 | −0.15 | −0.015** | 0.148 | 0.058 | −0.49 | 0.029* | 1 | |

| BUSINESS | 0.089* | 0.584 | 0.016 | −0.15 | 1.12 | −0.03 | 0.146* | 0.457 | 0.695 | −0.156* | 1.28 | 1 |

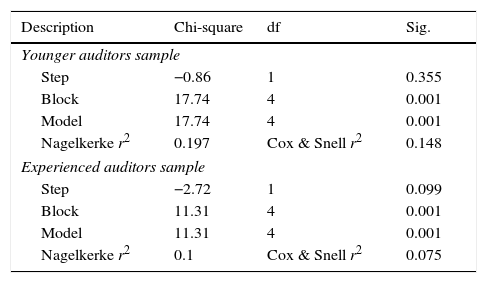

To test the first hypothesis, the sample was first divided into two samples of young and experienced auditors. To do so, just like the criteria of Broberg et al. (2013), the average work experience was calculated, thereafter, auditors with experience of more than the average were considered as experienced while others were considered as young. Thereafter, the logistic regression equation was specified for both samples. The results are provided in Table 5.

Binary probit regression results.

| Description | Chi-square | df | Sig. |

|---|---|---|---|

| Younger auditors sample | |||

| Step | −0.86 | 1 | 0.355 |

| Block | 17.74 | 4 | 0.001 |

| Model | 17.74 | 4 | 0.001 |

| Nagelkerke r2 | 0.197 | Cox & Snell r2 | 0.148 |

| Experienced auditors sample | |||

| Step | −2.72 | 1 | 0.099 |

| Block | 11.31 | 4 | 0.001 |

| Model | 11.31 | 4 | 0.001 |

| Nagelkerke r2 | 0.1 | Cox & Snell r2 | 0.075 |

Given that to compare the coefficients of the two samples we need to determine Z-statistics such as Fisher (1921), in order to compare the relationship between dependent and independent variables in a community with another independent community, in the present study, Z-statistic was used as demonstrated below.

Given that in multivariate regression analysis, the coefficient of determination (r2) demonstrates the changes in the dependent variable due to the independent variable, in this study, binary logistic regression was used. The Cox–Snell coefficient of determination plays the same role as r2 in multivariate regression, i.e., Cox–Snell coefficient of determination indicates the dependency between dependent and independent variables. Information on young auditors (less experienced) is as follows:

Information on experienced auditors is as follows:

So

Then considering that Z-statistic is equal to 1.128, the fourth hypothesis could not be verified. The results of this research are contrary to the findings of Broberg et al. (2013) and these findings are in line with the findings of Basioudis and Fifi (2004).

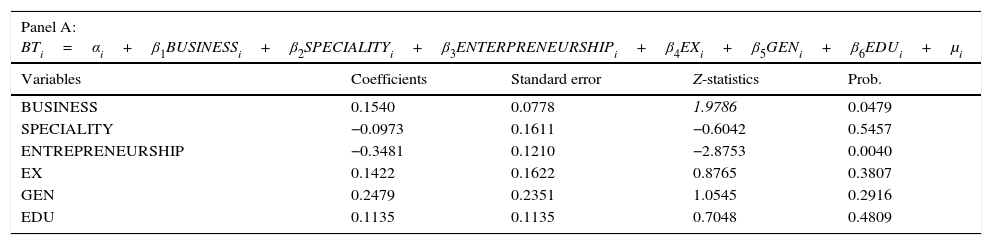

To test the second hypothesis, model (1) is used as follows:

The results of the model test are given in Table 6 panel A. As shown in Table 6 panel A, there is a positive and significant relationship between the business environment, with the time balance between marketing activities and auditing at 95%. Moreover, there is a negative and significant relationship between the entrepreneurial characteristic at 99%, with the time balance of marketing activities and auditing. One of the items that is of great importance in the business environment is corporate governance. The philosophy of corporate governance in a firm is to guarantee the interests of the relevant stakeholders of that firm. Therefore, compliance with laws and regulations, adherence to professional ethics, and the information transparency are the most important cases proposed in discussion of corporate governance. In corporate governance, in particular, the sector for the implementation of regulations monitors the compliance with laws and regulations in the Institute and in the case of any violations of the laws and regulations, besides guiding the executive department of law violation, offers guidelines for the strict observance of rules and regulations to executive departments. In this context, the development of corporate governance can affect the independence of auditors who are part of the corporate governance mechanisms. Marketing activities can threaten auditor independence, but the balance between them may be attributed to improvements in the business environment. Therefore, developing and improving the business environment can help to create balance between marketing and audit activities. As noted earlier in the previous hypotheses on the time balance between marketing and audit activities, in testing this hypothesis, there has been a negative and significant relationship between entrepreneurs with time balance of marketing and audit activities. This is because in the face of the client, before thinking about the time balance between audit and marketing activities, the entrepreneur auditors think about entrepreneurial and creative strategies to promote the objectives of the organization.

Binary probit regression results.

| Panel A: BTi=αi+β1BUSINESSi+β2SPECIALITYi+β3ENTERPRENEURSHIPi+β4EXi+β5GENi+β6EDUi+μi | ||||

|---|---|---|---|---|

| Variables | Coefficients | Standard error | Z-statistics | Prob. |

| BUSINESS | 0.1540 | 0.0778 | 1.9786 | 0.0479 |

| SPECIALITY | −0.0973 | 0.1611 | −0.6042 | 0.5457 |

| ENTREPRENEURSHIP | −0.3481 | 0.1210 | −2.8753 | 0.0040 |

| EX | 0.1422 | 0.1622 | 0.8765 | 0.3807 |

| GEN | 0.2479 | 0.2351 | 1.0545 | 0.2916 |

| EDU | 0.1135 | 0.1135 | 0.7048 | 0.4809 |

| Panel B: CGi=αi+β1BTi+β2SPECIALITYi+β3ENTERPRENEURSHIPi+β4EXi+β5GENi+β6EDUi+μi | ||||

|---|---|---|---|---|

| Variables | Coefficients | Standard error | Z-statistics | Prob. |

| BT | −0.1717 | 0.1628 | −1.0552 | 0.2913 |

| SPECIALITY | 0.0501 | 0.1613 | 0.3105 | 0.7561 |

| ENTREPRENEURSHIP | 0.1828 | 0.0487 | 3.7488 | 0.0002 |

| EX | −0.2091 | −0.2091 | −1.2894 | 0.1973 |

| GEN | −0.1065 | −0.1065 | −0.4527 | 0.6507 |

| EDU | −0.4988 | −0.4988 | −3.1336 | 0.0017 |

To test the third hypothesis, model 2 is used as follows:

After constructing the variables of the model, the least squares method was employed to test the model specified, but because of the proximity of the attitude score to corporate governance, the above model could not be statistically explained. Consequently, the dependent variable of time balance was defined as binary (zero-one). Therefore, the average of this change variable was calculated and responses above the mean were assigned one and the other were assigned zero. Thereafter, using zero and one probit, the model was tested. The results of the model are presented in Table 6 panel B. As shown in Table 6 panel B, entrepreneurship has a significant positive relationship, with attitude to corporate governance at 99%. The education also has a negative and significant relationship with attitude to corporate governance at 99%. Entrepreneur auditors believe that corporate governance is a favorable environment for the prosperity and creativity of auditing firm forces.

Consequently, entrepreneur auditors are very effective in the implementation and development of corporate governance mechanisms. By employing auditors, or training auditors to learn entrepreneurial skills, audit firms lead to improvement of the mechanisms of corporate governance in the company of the client. This is because the belief and attitude to a particular subject is the first step toward practical implementation of that issue. However, what is achieved in this research is remarkable, which is the negative and significant relationship of education and attitude to corporate governance. What is evident is the importance of education, but considering the attitude to corporate governance mechanisms, it must be stated that attitude toward corporate governance can only be in accordance with the formed objectives of the companies that are in the business environment of company and developed as a results of its needs. Auditors, who have higher education levels, are less willing to accept latent corporate governance of the client companies. Because in their mental background they have shaped certain conditions and presumptions of attitudes to corporate governance, which may not necessarily be in line with the benefits of their client.

To test the fourth hypothesis, models 3, 4 and 5 and Fig. 1 are used as follows:

Results are shown in Table 7 panels A, B and C. The fourth hypothesis aims to estimate the direct impact of attitude to business environment on the balance of time spent on marketing and auditing activities, as well as its indirect impact through the attitude toward corporate governance. So, the general impact of attitude toward business environment on the balance of time spent on marketing and auditing activities is computed in this part based on the estimation of other direct relationships related to the impacts of attitude to business environment. The following equivalent shows how the general impact of attitude toward business environment on the balance of time spent on marketing and auditing activities is calculated according to the simplified variable relations:

Fourth hypothesis results.

| Panel A: CGi=αi+β1BUSINESSi+β2SPECIALITYi+β3EXi+β4GENi+β5EDUi+μi | ||||

|---|---|---|---|---|

| Variables | Coefficients | Standard error | Z-statistics | Prob. |

| BUSINESS | 0.269 | 0.068 | 4.42 | 0 |

| SPECIALITY | −0.05 | 0.087 | −0.75 | 0.454 |

| EX | 0.018 | 0.128 | 0.296 | 0.768 |

| GEN | 0.023 | 0.087 | 0.379 | 0.705 |

| Panel B: BTi=αi+β1CGi+β2SPECIALITYi+β3EXi+β4GENi+β5EDUi+μi | |||||

|---|---|---|---|---|---|

| Variables | Coefficients | Standard error | Wald | df | Sig. |

| CG | 0.347 | 1.25 | 7.728 | 1 | 0.002 |

| SPECIALITY | 0.166 | 0.181 | 0.835 | 1 | 0.361 |

| EX | −0.03 | 0.365 | 0.007 | 1 | 0.932 |

| GEN | 1.097 | 0.611 | 3.221 | 1 | 0.073 |

| EDU | 0.324 | 0.38 | 0.771 | 1 | 0.38 |

| Constant | 0.808 | 2.286 | 0.125 | 1 | 0.724 |

| Nagelkerke r2 | 0.129 | Cox & Snell r2 | 0.101 | ||

| Panel C: BTi=αi+β1BUSINESSi+β2SPECIALITYi+β3EXi+β4GENi+β5EDUi+μi | |||||

|---|---|---|---|---|---|

| Variables | Coefficients | Standard error | Wald | df | Sig. |

| BUSINESS | 0.396 | 1.279 | 6.744 | 1 | 0.01 |

| SPECIALITY | 0.189 | 0.51 | 0.137 | 1 | 0.711 |

| EX | 0.16 | 0.448 | 0.127 | 1 | 0.721 |

| GEN | −1.12 | 0.44 | 6.503 | 1 | 0.011 |

| EDU | −0.14 | 0.448 | 0.092 | 1 | 0.762 |

| Constant | 2.681 | 2.887 | 0.862 | 1 | 0.353 |

| Nagelkerke r2 | 0.162 | Cox & Snell r2 | 0.122 | ||

The above equation shows the general impacts of attitude toward business environment on the balance of time spent on marketing and auditing activities.

According to estimated equations, ∂BT/∂CG that shows the impact of attitude toward corporate governance on the balance of time spent on marketing and auditing activities is equal to 0.347, ∂CG/∂BUSINESS that shows the impact of attitude to business environment on the attitude to corporate governance is equal to 0.269 and dBT/dBUSINESS showing the direct impact of attitude to business environment on the balance of time spent on marketing and auditing activities is equal to 0.396. Hence, the general impact of attitude toward business environment on the balance of time spent on marketing and auditing activities according to these estimated coefficients is equal to:

The results show that an increase by a unit for the attitude toward business environment results in 0.489 units increase in attitude toward balance of time spent on marketing and auditing activities, of which 0.396 is direct impact and 0.093 is indirect impact. So, the fourth hypothesis is confirmed.

Discussion and conclusionThe results of this study show that auditors having positive attitude to marketing and those who consider it as significant are able, to a large extent, to balance spent time for inherent auditing tasks and marketing activities. As the younger auditors are replaced with experienced ones, the inclination toward marketing changes as this is evident in their performance. Of course, there was no significant difference between the attitude of young auditors and that of experienced ones regarding the balance of time spent on marketing and auditing activities.

The importance of knowledge and business skills is higher than other skills (Lin, 2008). The need for institutions to determine the fee is more than ever felt with the development of trade, presence of more actors in auditing business field as well as an increased number of auditing institutions. This is because in a healthy competitive environment, institutions should determine fee, although there may be a rate-cut risk which can be compensated for by a careful and adequate supervision of auditors’ performance quality. Healthy business environment is capable of changing the auditors’ attitude toward marketing, as well as respecting their independence. Consideration of entrepreneurship in business field has a high degree of importance. Entrepreneurial auditors while encountering employers first think of entrepreneurial and creative solutions to develop organization's objectives before considering the balance of time spent on marketing and auditing activities.

Auditors as a group of company's stakeholders decrease the price of their activities by expressing their relationship toward the company by improvement of audit quality while maintaining their independence by specified marketing. In addition, they can have a major role in the improvement of corporate governance mechanism while indirectly reducing the costs of representatives and increasing employer's share price. Consequently, the balance of time spent on marketing and auditing activities by auditors may be influenced by their outlook on corporate governance regulations. Change by one unit in the attitude to business leads to an increase of 0.489 units in the attitude to balance the time spent on marketing and auditing activities, of which 0.396 is the direct impact and 0.093 is the indirect impact.

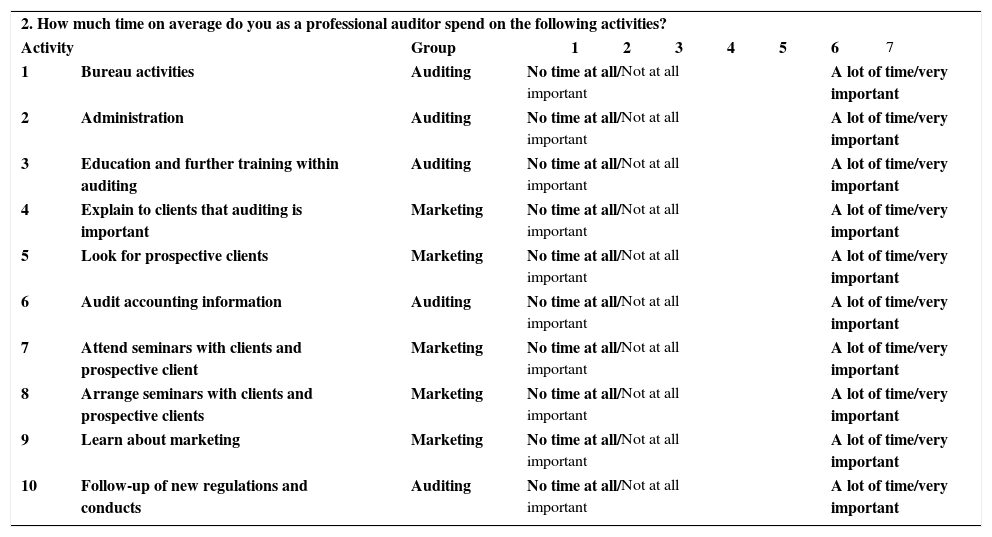

| 2. How much time on average do you as a professional auditor spend on the following activities? | |||||||||||

| Activity | Group | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |||

| 1 | Bureau activities | Auditing | No time at all/Not at all important | A lot of time/very important | |||||||

| 2 | Administration | Auditing | No time at all/Not at all important | A lot of time/very important | |||||||

| 3 | Education and further training within auditing | Auditing | No time at all/Not at all important | A lot of time/very important | |||||||

| 4 | Explain to clients that auditing is important | Marketing | No time at all/Not at all important | A lot of time/very important | |||||||

| 5 | Look for prospective clients | Marketing | No time at all/Not at all important | A lot of time/very important | |||||||

| 6 | Audit accounting information | Auditing | No time at all/Not at all important | A lot of time/very important | |||||||

| 7 | Attend seminars with clients and prospective client | Marketing | No time at all/Not at all important | A lot of time/very important | |||||||

| 8 | Arrange seminars with clients and prospective clients | Marketing | No time at all/Not at all important | A lot of time/very important | |||||||

| 9 | Learn about marketing | Marketing | No time at all/Not at all important | A lot of time/very important | |||||||

| 10 | Follow-up of new regulations and conducts | Auditing | No time at all/Not at all important | A lot of time/very important | |||||||

| 3. How do you rate auditing business environment in Iran? | ||||||||||

| Description | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |||

| 1 | No fair competitive market exists for auditing firms. | Totally disagree | Totally agree | |||||||

| 2 | Business transactions are not based on demand and supply and are based on personal relations. | Totally disagree | Totally agree | |||||||

| 3 | Auditing fee in not based on predefined price. | Totally disagree | Totally agree | |||||||

| 4 | The problem of changing fees influences over the quality of auditing. | Totally disagree | Totally agree | |||||||

| 5 | The main economical problem of auditing institutions is lack of liquidity of clients. | Totally disagree | Totally agree | |||||||

| 6 | Lack of proper mechanisms for professional ads leads to negative effect on liquidity. | Totally disagree | Totally agree | |||||||

| 7 | A main portion of auditing services is under the control of very few auditing institutions (5 to 10). | Totally disagree | Totally agree | |||||||

| 8 | Financial position of auditing firm has improved comparing to previous years. | Totally disagree | Totally agree | |||||||

| 9 | Not training skilled crew capable of using auditing standards and software leads to a complex challenge in business environment. | Totally disagree | Totally agree | |||||||

| 4. How do you evaluate the importance of corporate governance mechanisms? | ||||||||||

| Description | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |||

| 1 | Strengthening the role of non obliged managers in board of directors | Not at all important | Very important | |||||||

| 2 | Strengthening supportive rules of stakeholders’ interests | Not at all important | Very important | |||||||

| 3 | Preference of quality of auditing to its fees in practical procedures | Not at all important | Very important | |||||||

| 4 | Expanding role and responsibilities of auditing committees | Not at all important | Very important | |||||||

| 5 | Expanding role and responsibilities of internal auditors | Not at all important | Very important | |||||||

| 6 | Defining social role of auditing for clients | Not at all important | Very important | |||||||

| 7 | Defining the effect of mechanisms of corporate governance on auditing reports for clients | Not at all important | Very important | |||||||

| 8 | Duality of CEO and chairman of the board | Not at all important | Very important | |||||||

| 9 | Training managers in terms of corporate governance mechanisms | Not at all important | Very important | |||||||

| 5. Evaluating entrepreneurial skills of people | ||||||||||

| Description | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |||

| 1 | Usually, I try to accept the responsibility in team work. | Totally Disagree | Totally Agree | |||||||

| 2 | I am able to materialize my ideas. | Totally Disagree | Totally Agree | |||||||

| 3 | I am so tolerant. | Totally Disagree | Totally Agree | |||||||

| 4 | I believe I can influence over results. | Totally Disagree | Totally Agree | |||||||

| 5 | I am praised because of my ability in fast analysis of complicated situations. | Totally Disagree | Totally Agree | |||||||

| 6 | I’d rather work with an incompatible but proficient person than a friendlier and less efficient person. | Totally Disagree | Totally Agree | |||||||

| 7 | I can fire employees who are not profitable. | Totally Disagree | Totally Agree | |||||||

| 8 | I want to leave safe jobs with high payment to start my own business. | Totally Disagree | Totally Agree | |||||||

| 9 | I incline myself towards laborious tasks. | Totally Disagree | Totally Agree | |||||||

| 10 | I can work for long hours. | Totally Disagree | Totally Agree | |||||||

| 11 | I need to be best in whatever I do. | Totally Disagree | Totally Agree | |||||||

| 12 | I do not disappoint easily. | Totally Disagree | Totally Agree | |||||||

| 13 | I prefer develop in challenges and hardships. | Totally Disagree | Totally Agree | |||||||

| 14 | I am tired of doing repeated tasks. | Totally Disagree | Totally Agree | |||||||

| 15 | I don’t like to be ordered for some duties. | Totally Disagree | Totally Agree | |||||||

| 16 | Comparing to other, I have more proficiency in performing tasks. | Totally Disagree | Totally Agree | |||||||

| 17 | I have the ability of managing some works. | Totally Disagree | Totally Agree | |||||||

| 18 | I enjoy performing complex works and have this ability. | Totally Disagree | Totally Agree | |||||||

| 19 | In the case of inefficiency in one action, I can change the procedure. | Totally Disagree | Totally Agree | |||||||

| 20 | In my colleagues’ opinions, I am a creative person in solving problems. | Totally Disagree | Totally Agree | |||||||

| 21 | I have the ability of relating the whole and details of job. | Totally Disagree | Totally Agree | |||||||

| 22 | I have the ability of predicting the effect of current operations on future actions. | Totally Disagree | Totally Agree | |||||||

Peer Review under the responsibility of Universidad Nacional Autónoma de México.