To identify and analyze the resources and costs associated with the administration of intramuscular antiretroviral therapy (ART) cabotegravir+rilpivirine (CAB+RPV) compared to oral ART in the management of Human Immunodeficiency Virus Type 1 (HIV-1) infection in Spain.

MethodsAn economic model was developed to identify resources and analyze costs from the perspective of the National Health System (NHS) and societal, associated with the administration of intramuscular ART (CAB+RPV) compared to oral ART over a two-year time horizon. Costs included treatment change monitoring, pharmaceutical dispensation, administration, management of adverse events to injection-site reactions (AEs-ISR), travel to the hospital, telepharmacy service, and lost work productivity. Unit costs (€, 2023) were obtained from the literature. Sensitivity analyses were conducted to evaluate the robustness of the model.

ResultsIntramuscular ART compared to oral ART was associated with an increase in costs of €673.16/patient over two years from the perspective of the NHS, and €719.59/patient from the social perspective. Intramuscular ART would generate increased costs for dispensation (+€97.75), administration (+€394.55), monitoring (+€288.74), management of AEs-ISR (+€6.46), travel (+€8.36), and lost work productivity (+€38.07), compared to oral ART administration.

ConclusionTreating HIV-1 with intramuscular CAB+RPV leads to increased resource consumption and costs, compared to oral ART.

Identificar y analizar los recursos y costes asociados a la administración del tratamiento antirretroviral (TAR) cabotegravir+rilpivirina (CAB+RPV) intramuscular frente al TAR oral en el manejo de la infección por el Virus de la Inmunodeficiencia Humana Tipo I (VIH-1), en España.

MétodosSe desarrolló un modelo para la identificación de recursos y análisis de costes desde la perspectiva del Sistema Nacional de Salud (SNS) y de la sociedad asociado a la administración del TAR intramuscular (CAB+RPV) frente al TAR oral en un horizonte temporal de dos años. Los costes englobaron la monitorización por cambio de tratamiento, dispensación farmacéutica, administración, manejo de los eventos adversos por reacciones en el lugar de inyección (EAs-RLI), desplazamiento al centro hospitalario, servicio de telefarmacia y pérdida de productividad laboral. Los costes unitarios (€, 2023) se obtuvieron de la literatura. Se realizaron análisis de sensibilidad para evaluar la robustez del modelo.

ResultadosEl TAR intramuscular frente al TAR oral se asoció con un incremento de los costes de 673,16€/paciente en dos años desde la perspectiva del SNS y de 719,59€/paciente desde la perspectiva social. El TAR intramuscular generaría incremento de costes de dispensación (+97,75€), administración (+394,55€), monitorización (+288,74€), manejo de los EAs-RLI (+6,46€), desplazamiento (+8,36€) y pérdida de productividad laboral (+38,07€), respecto a la administración de TAR oral.

ConclusionesEl tratamiento del VIH-1 con CAB+RPV intramuscular implica un aumento del consumo de recursos y costes, frente al TAR oral.

It is estimated that there are currently in the region of 136,436 to 162,307 people living with human immunodeficiency virus (HIV) in Spain; this represents a prevalence of 0.31%, and 92.5% know that they are infected.1

The therapeutic approach for the chronic management of HIV type 1 (HIV-1) is centred around antiretroviral therapy (ART), the objective of which is to achieve the maximum and longest-lasting suppression of the plasma viral load, reduce the morbidity associated with HIV replication and its effect on other comorbidities, and to prevent transmission of the virus.2–4 Widespread access to such therapy has dramatically reduced HIV-related morbidity and mortality rates.3,5

In patients who have not received prior ART, the treatment strategy is based on combinations of two or three oral antiretroviral drugs administered daily.3,6 However, the proportion of people living with HIV who are aware of their diagnosis and are undergoing treatment is 96.6% and, of these, 9.6% do not achieve viral suppression.1

The continuous advances in therapy and changes in the therapeutic needs of patients with HIV have led to the development of new alternatives, such as long-acting ART agents, which allow greater independence and enable therapeutic levels of ART to be maintained for a longer period of time.2,3,7

The currently available long-acting ART, cabotegravir (CAB) and rilpivirine (RPV), administered by intramuscular injection every two months, was approved in November 2022 for the treatment of adult patients with HIV-1 infection who are virally suppressed on stable ART, with no current or prior evidence of resistance, and with no prior virological failure on non-nucleoside reverse transcriptase inhibitors (NNRTIs) or integrase inhibitors (INIs).2

The development of this type of drug administered by intramuscular injection represents a paradigm shift, as it reduces the patient's perception of stigma or their concern with regard to the lesser degree of confidentiality about their HIV-positive status associated with oral treatments.8,9 However, given the characteristics of this type of "long-acting" therapy, which needs to be administered by a healthcare professional, studies are needed to identify the possible economic impact and possible loss of free time associated with the intramuscular administration of ART.

The aim of this analysis was to determine the use of resources and costs associated with the administration of intramuscular ART with CAB+RPV compared to the administration of oral ART in adult patients with HIV-1, from both the perspective of the Sistema Nacional de Salud (SNS) [Spanish National Health Service] and society.

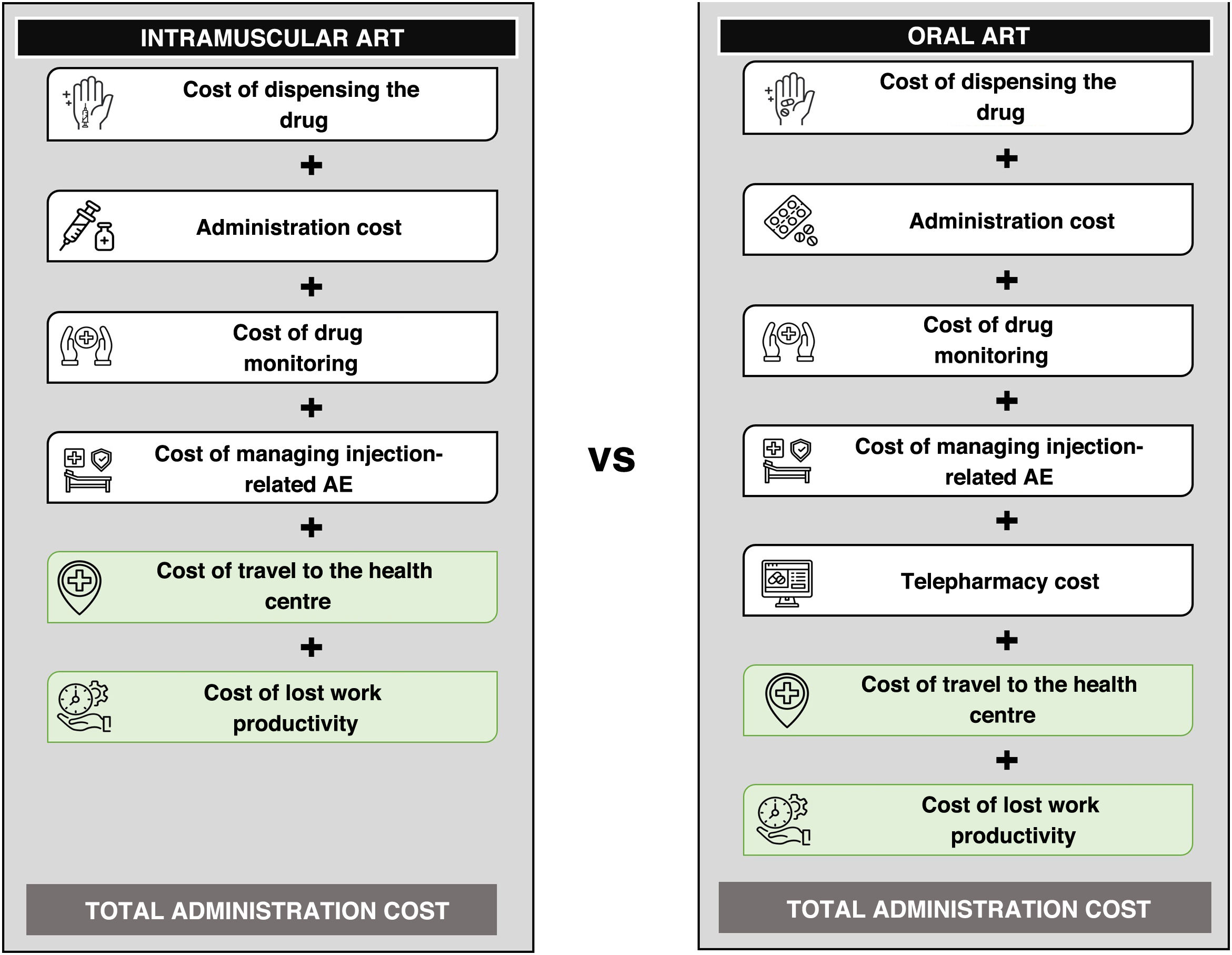

MethodsA cost analysis model was developed in Microsoft Excel® to estimate the resource consumption and costs associated with the administration of intramuscular ART with CAB+RPV versus oral ART in adult patients with HIV-1 who are virally suppressed on stable treatment (Fig. 1). Because CAB+RPV requires an induction phase followed by continuation injections every two months, a time horizon of two years was considered in order to reflect all the administrations necessary at the start of intramuscular treatment.

Different resources and costs were taken into account based on each perspective taken. From the perspective of the SNS, we only considered the direct healthcare costs associated with dispensing and administration of the drugs, monitoring and management of adverse events due to injection site reactions (AE-ISR). From a societal perspective, in addition to direct healthcare costs, we considered non-healthcare-related direct costs, such as travel to the health centre for administration and/or dispensing of medication, and indirect costs calculated through loss of work productivity.

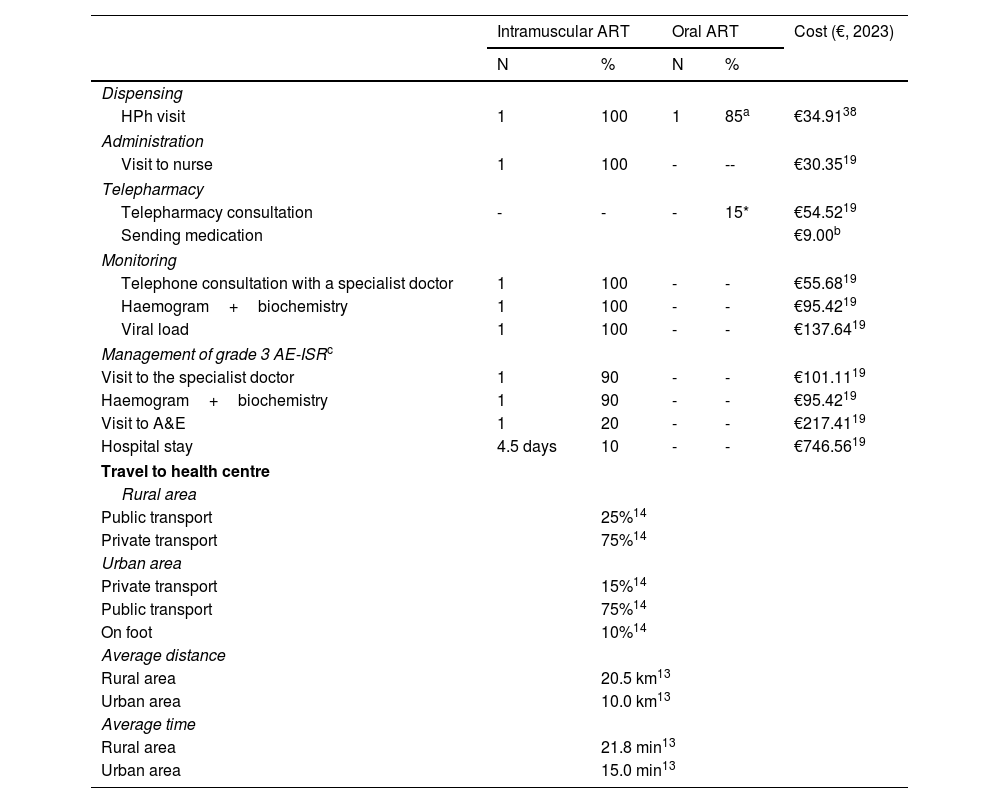

For CAB+RPV, we considered administration every two months,10,11 which meant a total of 13 administrations (seven in the first year and six the second year) over the time horizon; this had the associated costs of dispensing by hospital pharmacy and administration by nursing staff (Table 1).

Use and costs of resources due to administration, by ART type.

| Intramuscular ART | Oral ART | Cost (€, 2023) | |||

|---|---|---|---|---|---|

| N | % | N | % | ||

| Dispensing | |||||

| HPh visit | 1 | 100 | 1 | 85a | €34.9138 |

| Administration | |||||

| Visit to nurse | 1 | 100 | - | -- | €30.3519 |

| Telepharmacy | |||||

| Telepharmacy consultation | - | - | - | 15* | €54.5219 |

| Sending medication | €9.00b | ||||

| Monitoring | |||||

| Telephone consultation with a specialist doctor | 1 | 100 | - | - | €55.6819 |

| Haemogram+biochemistry | 1 | 100 | - | - | €95.4219 |

| Viral load | 1 | 100 | - | - | €137.6419 |

| Management of grade 3 AE-ISRc | |||||

| Visit to the specialist doctor | 1 | 90 | - | - | €101.1119 |

| Haemogram+biochemistry | 1 | 90 | - | - | €95.4219 |

| Visit to A&E | 1 | 20 | - | - | €217.4119 |

| Hospital stay | 4.5 days | 10 | - | - | €746.5619 |

| Travel to health centre | |||||

| Rural area | |||||

| Public transport | 25%14 | ||||

| Private transport | 75%14 | ||||

| Urban area | |||||

| Private transport | 15%14 | ||||

| Public transport | 75%14 | ||||

| On foot | 10%14 | ||||

| Average distance | |||||

| Rural area | 20.5 km13 | ||||

| Urban area | 10.0 km13 | ||||

| Average time | |||||

| Rural area | 21.8 min13 | ||||

| Urban area | 15.0 min13 | ||||

| Loss of work productivity, time | Intramuscular ART | Oral ART | |||

|---|---|---|---|---|---|

| Dispensing in hospital pharmacyb | 15 min | - | |||

| Drug administrationd | 10 min | - | |||

| Travel to treatmente | 16 min | - | |||

| Travel from treatmente | 16 min | - | |||

| Salary cost/hour | €23.5539 | ||||

The unit costs obtained from the eSalud database19 represent an average of the rates published in the Official Bulletins of Spain's Autonomous Regions.

AE-ISR: adverse events - injection site reactions; A&E: Accident and Emergency; ART: antiretroviral therapy; HPh: hospital pharmacy.

Of the total number of patients on oral ART, it was assumed that 85% go to the hospital pharmacy service to collect oral ART every two months, while 15% benefit from a telepharmacy service so the medication is sent to their home every two months.

Management cost applied to the proportion of patients with grade 3 AE-ISR (1.16% of the total patients treated with CAB+RPV).

Estimated time, taken from cabotegravir and rilpivirine summaries of product characteristics, for patient observation after administration.10,11

In oral ART, according to the expert panel, pharmacy dispensing was established every two months. In order to reflect the care programmes in place across Spain and the increasingly widespread use of telepharmacy (remote dispensing and informed delivery) as a supply strategy, the cost of travel to the hospital and dispensing of treatment by hospital pharmacy was assumed in 85% of patients, while the cost of telepharmacy was charged for the remaining 15% (Table 1). For intramuscular ART, it was assumed that 50% of patients go to the hospital pharmacy to collect the treatment for administration at the centre and in the remaining 50%, the drug is sent by this service to the place of administration through healthcare personnel from the centre itself.

For monitoring costs, only laboratory tests and telephone consultation with the specialist carried out after the first administration of CAB+RPV due to starting the new treatment were considered apart (Table 1). It was assumed that HIV patient monitoring is not altered by different routes of administration of ART, so this cost in general was not considered.

Due to their clinical and economic relevance, we only considered the cost of managing grade 3 AE-ISR associated with CAB+RPV (Table 1). According to clinical practice observed by experts in HIV management, 90% of patients treated with CAB+RPV report AE-ISR, 1.29% of which are grade 3.7

In order to estimate travel costs, we considered the proportion of the population residing in urban areas (84%) and rural areas (16%),12 and their distances to the health centre,13 as well as the type of transport used (private, public or on foot)14 (Table 1). Costs associated with private transport were estimated based on the average fuel consumption and the average cost of fuel in Spain published in the literature (€1.29/l).15 For public transport, the average cost of a ticket in Spain (€1.51) was applied.16

The loss of work productivity was estimated assuming that 100% of intramuscular administrations are carried out in the morning and considering the patients with HIV who are actively working (52.2%),17 the proportion of patients on treatment with CAB+RPV who come to the hospital during the working day (12.5%) and the average time spent travelling to the health centre (estimated from data found in the literature13 and from clinical practice observed by experts) (Table 1). For patients receiving oral ART, no loss of work productivity was considered as they are able to go to the hospital pharmacy in the evening and outside of working hours.

Resource consumption was validated and agreed upon by a multidisciplinary panel of experts consisting of three clinicians and two hospital pharmacists. Unit costs were obtained from different sources in the literature15,16,18 and from a national database of healthcare costs.19 All costs were updated according to the Spanish consumer price index (índice de precios de consumo [IPC]),20 and are expressed in euros for the year 2023 (€, 2023) (Table 1).

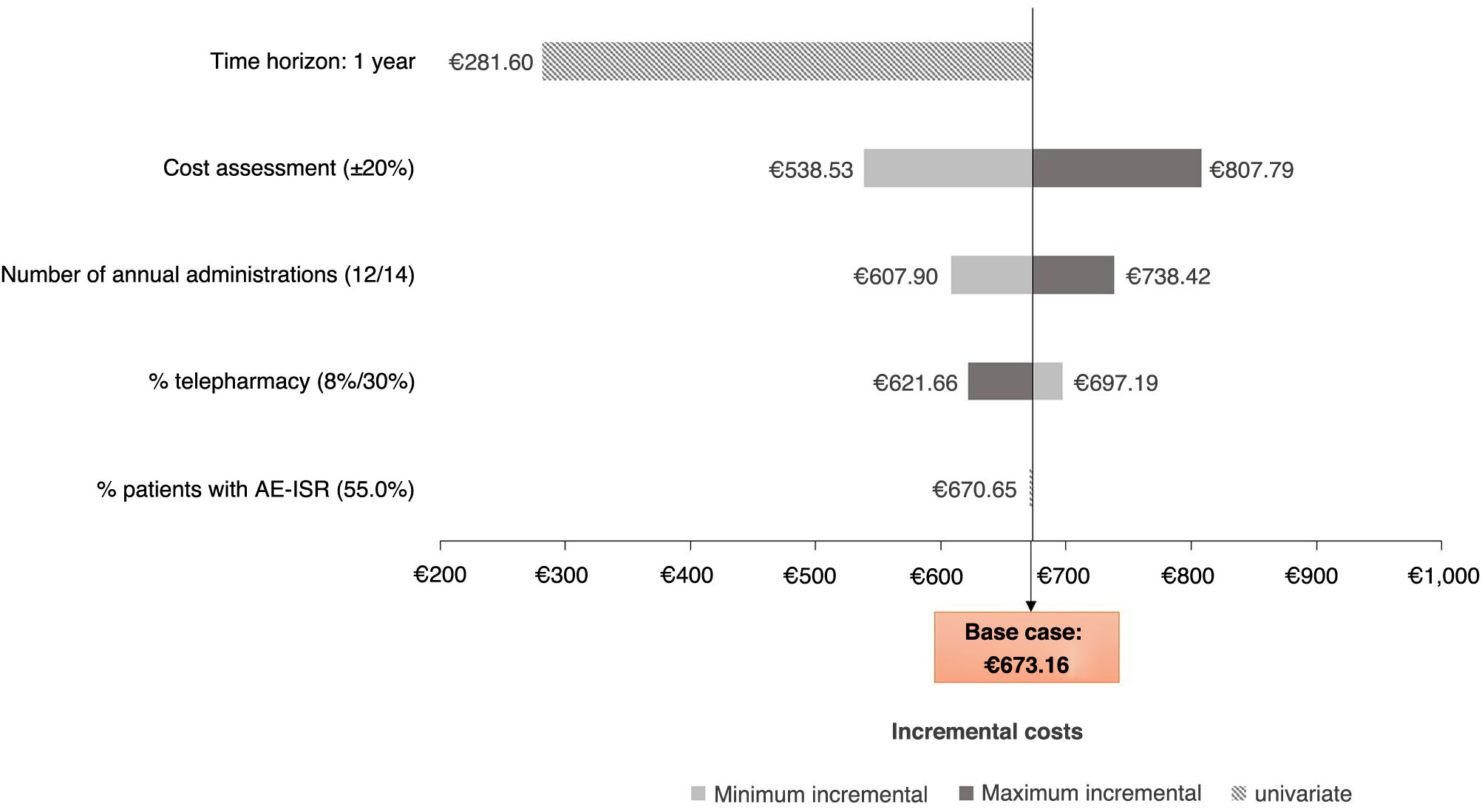

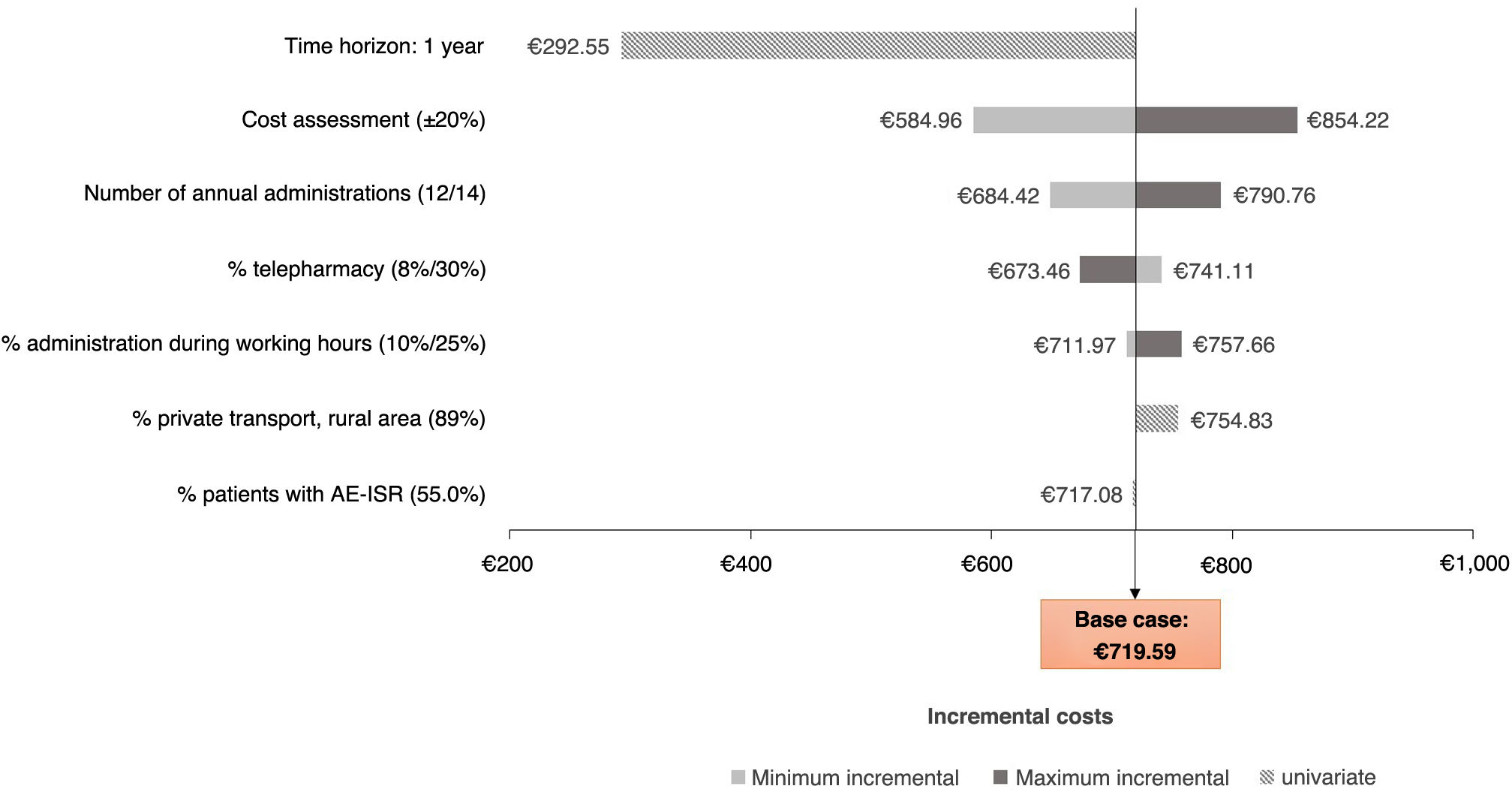

Sensitivity analysisIn order to evaluate the robustness of the analysis, a univariate deterministic sensitivity analysis (DSA) was performed with different scenarios, modifying the number of annual administrations of CAB+RPV (±1 administrations), the one-year time horizon, the unit costs (±20%), the proportion of patients on oral ART with the option of telepharmacy (8% and 30%), the proportion of patients with AE-ISR of any grade (55%),7 the proportion of patients who use private transport in rural areas (89%)13 and the proportion of patients on intramuscular ART who come to the hospital for administration during the working day (10% and 25%).

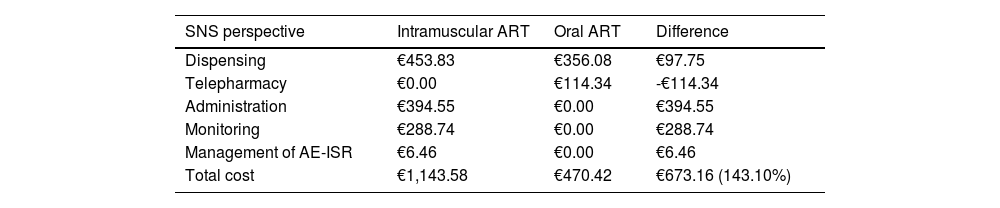

ResultsSpanish national health service perspectiveFrom the perspective of the Sistema Nacional de Salud (SNS) [Spanish national health service] and considering a two-year time horizon, the total cost associated with the intramuscular administration of ART was €1,143.58 per patient, compared to €470.42 with oral administration, which represented a 143.10% increase in healthcare costs per patient (Table 2). Considering a price parity in the acquisition costs of the two drugs, the total cost of intramuscular ART would entail an additional cost of €673.16 per patient compared to oral ART.

Base case results from the perspective of the SNS.

| SNS perspective | Intramuscular ART | Oral ART | Difference |

|---|---|---|---|

| Dispensing | €453.83 | €356.08 | €97.75 |

| Telepharmacy | €0.00 | €114.34 | -€114.34 |

| Administration | €394.55 | €0.00 | €394.55 |

| Monitoring | €288.74 | €0.00 | €288.74 |

| Management of AE-ISR | €6.46 | €0.00 | €6.46 |

| Total cost | €1,143.58 | €470.42 | €673.16 (143.10%) |

AE-ISR: adverse events - injection site reactions; ART: antiretroviral therapy; SNS: Sistema Nacional de la Salud [Spanish national health service].

Compared to oral ART, HIV management with intramuscular ART resulted in higher costs per patient for administration (+€394.55), monitoring (+€288.74) and management of grade 3 AE-ISR (+€6.46) (Table 2). In addition, treatment with CAB+RPV was associated with an increase in hospital pharmacy dispensing costs of €97.75 per patient compared to those associated with oral ART.

Meanwhile, oral ART was associated with a telepharmacy cost per patient of €114.34 (Table 2).

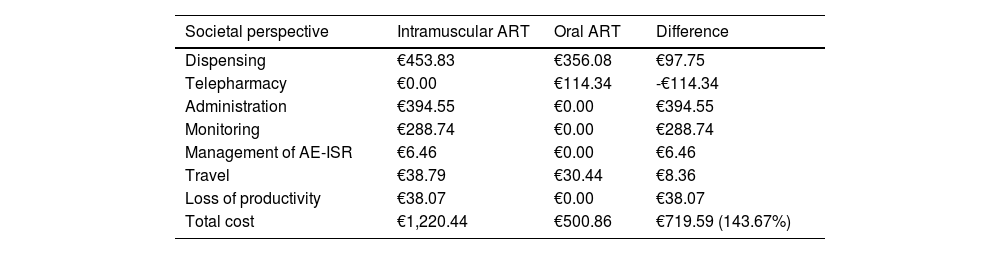

Societal perspectiveFrom a societal perspective, the total cost associated with the administration of intramuscular ART over a two-year time horizon was €1,220.44 per patient, compared to €500.86 with oral ART, which represented an increase per patient of 143.67% (Table 3). Considering a price parity in the acquisition costs of the two drugs, the total cost of intramuscular ART would entail an additional cost of €719.59 per patient compared to oral ART.

Base case results from the societal perspective.

| Societal perspective | Intramuscular ART | Oral ART | Difference |

|---|---|---|---|

| Dispensing | €453.83 | €356.08 | €97.75 |

| Telepharmacy | €0.00 | €114.34 | -€114.34 |

| Administration | €394.55 | €0.00 | €394.55 |

| Monitoring | €288.74 | €0.00 | €288.74 |

| Management of AE-ISR | €6.46 | €0.00 | €6.46 |

| Travel | €38.79 | €30.44 | €8.36 |

| Loss of productivity | €38.07 | €0.00 | €38.07 |

| Total cost | €1,220.44 | €500.86 | €719.59 (143.67%) |

AE-ISR: adverse events - injection site reactions; ART: antiretroviral therapy; SNS: Sistema Nacional de la Salud [Spanish national health service].

In addition to the healthcare costs mentioned above, intramuscular ART generated costs of lost work productivity (+€38.07/patient) and was associated with an increase in travel costs of €8.36 per patient compared to oral ART (Table 3).

Sensitivity analysisFrom the perspective of the SNS (Fig. 2), the scenario that caused the greatest variation in costs was considering the one-year time horizon, due to the greater number of intramuscular administrations carried out in year 1 compared to year 2, and the more exhaustive patient monitoring as a consequence of the change in treatment. The scenario that least affected the results obtained was the variation in the proportion of patients with any grade of AE-ISR, as those of a mild nature were not associated with any management costs.

![Deterministic sensitivity analysis diagram from the perspective of the Spanish national health service. AE-ISR: adverse events - injection site reactions; SNS: Sistema Nacional de la Salud [Spanish national health service].](https://static.elsevier.es/multimedia/2529993X/unassign/S2529993X24002582/v2_202501230445/en/main.assets/gr2.jpeg?xkr=ue/ImdikoIMrsJoerZ+w997EogCnBdOOD93cPFbanNc+34VOwP+2HTB5hao7CSfc3vHAcopEDD4TvJ2qcebX0gs12FWnes6tRAug9qRjSzglixh6NeA+dW6v4+6nNWM0krRR6hD4ZFzMsY4iPcrNRO87jzYDSJb9JAfHz/7VbPYaJa9eDt4Q7GoakuWrJb6e4klWtCF70ospGJmBzoCqZDBqR3BRzJwfaS2brDToU36ydGhgBV1fhe8PTBvxpT+lSNDU06+SUvV46W3NeuHA4jwIIj7sdh7pXNUHa4XMUGRsUrBK5jfHAJhoP0xHlHconziPlylMZaSr1ph1/1ytgA== "Deterministic sensitivity analysis diagram from the perspective of the Spanish national health service. AE-ISR: adverse events - injection site reactions; SNS: Sistema Nacional de la Salud [Spanish national health service].")

From a societal perspective (Fig. 3), the alternative scenarios analysed followed a similar trend to those observed from the perspective of the SNS, in terms of the time horizon, number of intramuscular administrations and variation in costs. The increase in the proportion of patients using private transport in rural areas, and the variation in the proportion of patients who go to the hospital during their working day for the administration of intramuscular ART, also led to an increase in the incremental costs between intramuscular and oral ART, albeit to a lesser extent.

Discussion![Deterministic sensitivity analysis diagram from the societal perspective. AE-ISR: adverse events - injection site reactions; SNS: Sistema Nacional de la Salud [Spanish national health service].](https://static.elsevier.es/multimedia/2529993X/unassign/S2529993X24002582/v2_202501230445/en/main.assets/gr3.jpeg?xkr=ue/ImdikoIMrsJoerZ+w997EogCnBdOOD93cPFbanNc+34VOwP+2HTB5hao7CSfc3vHAcopEDD4TvJ2qcebX0gs12FWnes6tRAug9qRjSzglixh6NeA+dW6v4+6nNWM0krRR6hD4ZFzMsY4iPcrNRO87jzYDSJb9JAfHz/7VbPYaJa9eDt4Q7GoakuWrJb6e4klWtCF70ospGJmBzoCqZDBqR3BRzJwfaS2brDToU36ydGhgBV1fhe8PTBvxpT+lSNDU06+SUvV46W3NeuHA4jwIIj7sdh7pXNUHa4XMUGRsUrBK5jfHAJhoP0xHlHconziPlylMZaSr1ph1/1ytgA== "Deterministic sensitivity analysis diagram from the societal perspective. AE-ISR: adverse events - injection site reactions; SNS: Sistema Nacional de la Salud [Spanish national health service].")

This analysis has estimated the economic impact of intramuscular ART administration (CAB+RPV) compared to the administration of oral ART in patients with HIV-1 in Spain, focusing exclusively on the quantification of the resources used and associated with the route of ART administration from SNS and societal perspectives.

Through cost analysis, it is possible to quantify, in monetary units, and estimate the financial impact associated with the administration of intramuscular ART and compare it with oral administration, providing descriptive information on the cost of treatment. Studies of this type focused on cost estimation are a key resource when evaluating the allocation of healthcare, human and material resources in the health service and society as a whole.21,22

As this analysis demonstrates, the costs associated with the administration of intramuscular ART could increase by up to 143.67% (societal perspective) compared to the administration of oral ART. In view of our results, if the acquisition costs of intramuscular and oral ART were not equal, the pharmacological cost of oral ART could increase by around 14% until reaching parity with the total cost that would be involved in the acquisition and administration of intramuscular ART. If we were to consider a hypothetical cohort of 12,000 HIV-1 patients treated with intramuscular ART, estimated from the data published in Spain on the number of patients with suppressed HIV1,23 and the possible proportion of use of intramuscular ART (10%), from a societal perspective, this would generate a total two-year cost increase of €8,635,060 compared to oral ART. These results should be taken into account in order to optimise therapeutic choice.

This is the first published study to compare the costs associated with the administration of intramuscular ART and the oral ART alternatives. In general, there are few published economic evaluation studies on intramuscular ART,6,24 conducted with the aim of evaluating the efficiency of this type of treatment. One of these studies was carried out from the perspective of the SNS and focused on analysing pharmacological costs and adherence,6 ignoring non-healthcare costs (both direct and indirect), which represent a high burden for patients, as our analysis suggests. The results of this cost-effectiveness analysis showed that after a lifetime time horizon, treatment with intramuscular CAB+RPV compared to oral ART was associated with 0.27 additional quality-adjusted life years and an increase in total costs of €4,003, resulting in an incremental cost-utility ratio of €15,003 per quality-adjusted life year.6 Total costs may have increased when looking at costs from a societal perspective.

In our analysis, which focused on analysing the differences in the use of resources associated with the intramuscular versus oral administration routes, pharmacological costs were not taken into account due to the lack of public prices. Nor did we consider the costs associated with HIV management, assuming that patient follow-up is the same regardless of the route of administration of the treatment, except for the starting period of treatment with CAB+RPV, in which the specific monitoring was considered apart.

One of the key aspects of the costs associated with oral ART is telepharmacy (telematic follow-up by the pharmacist and delivery of the medication to the patient's home), which has been of great benefit to the patient, due to the savings in travel to the health centre to have the medication dispensed, meaning they are not losing free time or working hours.25,26 In health centres where the telepharmacy service has not been implemented, pharmaceutical care (PC) models have been put in place that help minimise the loss of work productivity for HIV patients by offering the option of accessing the hospital pharmacy outside of working hours.27–29

This type of PC model is not possible with intramuscular ART, which requires administration by a healthcare professional in the health centre, leading to losses in work productivity and an increase in costs to be assumed by patients, such as having to travel to the centre, sometimes from more remote areas.

In this study, loss of work productivity was estimated based on the assumption that all intramuscular administrations are carried out during consultation hours from 8 a.m. to 3 p.m. However, it is possible that some hospitals will have longer opening hours, which would allow patients to attend for intramuscular ART administration outside their working hours and would therefore be associated with a lower societal cost for lost productivity.

Another notable fact in treatment with "long-acting agents" and which we did not take into account in this analysis is the development of resistance to the treatment.30–32 The ATLAS-2M clinical trial reported that 2.3% of patients with CAB+RPV administered every two months had confirmed virological failure at 152 weeks.7

Our analysis is not without limitations, one of which is the great variability in patient management between different hospital centres.3,33–36 In order to minimise this heterogeneity, the parameters included in the analysis reflected the clinical practice of a panel of experts made up of hospital pharmacists and infectious disease specialists from different hospitals in Spain.

Another limitation to take into account is not having considered, due to lack of data, the waiting time for the patient at the health centre. Despite developing new care models aimed at better time management,3,33–36 some patients have to wait a considerable amount of time prior to the administration of intramuscular ART or in the hospital pharmacy to collect their oral ART. It is possible that if we had considered this time invested by the patient, the loss of work productivity costs would have increased.

With regard to the management of AE-ISR, according to the data reported in the clinical trial of CAB+RPV,7 55% of patients with intramuscular ART had some type of AE. However, the rates of patients reporting some type of discomfort at the injection site (mainly pain and swelling) in real life have been found to be much higher than those reported in clinical trials. After considering in the base case an any-grade AE-ISR rate of 90%, based on observation in clinical practice, a sensitivity analysis was performed with the rate reported in the ATLAS-2M trial (55.0%),7 finding that the costs generated by the management of AE-ISR affect the results to a lesser extent, as the management of patients with mild AE-ISR does not require the use of healthcare resources, and grade 3 AE-ISR were only found in a tiny proportion of patients.

One of the key aspects in this type of treatment that we did not take into account in our analysis is patient adherence, which may be affected by aspects related to the dosage regimen and dosing frequency, dietary restrictions and the stigma involved.8,9 Clinical trials conducted with CAB+RPV appear to report higher adherence rates than with oral therapy.7 However, studies based on real clinical practice that reflect long-term adherence rates are warranted in order to analyse therapeutic adherence more prospectively.37

Due to the nature of cost analyses, this study focused on quantifying the resources generated by intramuscular and oral administration of ART, without assessing other fundamental aspects such as efficacy and quality of life, as is done in cost-effectiveness studies.32

Despite the limitations described above, this type of study is essential to determine the sustainability of a healthcare system of limited resources. This cost analysis represents a first step in assessing the economic impact associated with the type of ART administration. However, in light of the results obtained, observational studies are necessary, which, in addition to analysing the costs generated by the administration of ART, whether intramuscular or oral, also analyse the healthcare and non-healthcare resources used in greater detail. In addition, further cost-effectiveness analyses are needed to assess the effectiveness of intramuscular versus oral alternatives. This would help the system generate more efficient healthcare management models.

ConclusionsCompared to oral ART, intramuscular ART in virally suppressed adults with HIV-1 infection entails an increase in healthcare costs and indirect costs, mainly due to the need for healthcare personnel to administer it.

CRediT authorship contribution statementVE, JEL, RMV, MPE and JS validated the structure of the model and helped interpret the data and prepare the manuscript.

AC contributed to interpreting the results and reviewing the manuscript.

MP and LSO contributed to the literature search, study design, data collection, data interpretation and manuscript preparation.

All authors approved the final manuscript.

FundingThis study was funded by Gilead Sciences.