Environmental, Social, and Governance (ESG), a key concept in sustainable development, plays a critical role in shaping corporate green economic activities. This study investigated the effect of ESG information disclosure on corporate green innovation using data from Chinese A-share listed companies from 2013 to 2022. The findings revealed that ESG information disclosure significantly fosters corporate green innovation and the results remain robust across various robustness checks and endogeneity tests. The heterogeneity analysis indicated that the positive effect of ESG information disclosure on corporate green innovation is more pronounced among state-owned enterprises, firms located in the eastern region, and companies operating in non-heavily polluting industries. Furthermore, mechanism analysis suggested that ESG information disclosure influences corporate green innovation through two primary channels: easing financing constraints and attracting the attention of analysts. However, this study acknowledged the limitations of the mechanism analysis. Future research should aim to integrate insights from related disciplines to further explore the mechanisms by which ESG information disclosure affects corporate green innovation from a more comprehensive perspective.

Global issues such as environmental pollution and climate change are becoming increasingly severe. Research has shown that the frequency and intensity of extreme weather events continue to rise, primarily because of massive greenhouse gas emissions. In 2019, to combat climate change and environmental crises while safeguarding industrial competitiveness within the region, the European Union issued the European Green Deal, which announced the goal of achieving net-zero greenhouse gas emissions by 2050. Currently, countries around the world are enacting environmental policies aligned with their national conditions to support the achievement of carbon neutrality goals. Sustainable development has become a focal point of global attention (Arisanti et al., 2024; Jasmi & Hassan, 2024; Khasawneh, 2024; Hoşgör et al., 2023; Hu et al., 2024; Lin & Zhai, 2023; Lošonczi et al., 2022; Oceng et al., 2023; Shashyna et al., 2023).

While experiencing rapid economic growth, China faces the serious challenge of high carbon dioxide emissions (He et al., 2022; Wang et al., 2024; Zhao et al., 2023). Consequently, the Chinese government and relevant departments have taken proactive measures to promote energy conservation and emission reduction, improve the environmental well-being of their citizens, and shoulder global responsibilities. China's 13th and 14th Five-Year Plans emphasize the strategic importance of green development in the modernization process. Furthermore, China's 20th National Congress Report reiterated the sustainable development concept of “lucid waters and lush mountains are invaluable assets” and called for advancing the green transformation of economic and social development, firmly pursuing a path of ecological development to help achieve the “dual carbon” goals (Hu et al., 2024).

However, addressing environmental issues is not the sole responsibility of the government; enterprises also play a critical role in this process. Enterprises are key players in the market environment and must effectively fulfill dual roles. Companies should continuously innovate to enhance their market share and value, thereby strengthening their competitive advantages, which require financial, human, and material resources. Meanwhile, companies must assume a certain level of social responsibility and focus on environmental protection while pursuing economic growth. They should strive for high-quality and sustainable development, contributing to global carbon emission reduction efforts. Therefore, entrepreneurs today face the challenge of striking a balance between operating in a competitive market environment and promoting sustainable development. This balance must provide both economic and environmental benefits to enterprises.

Green innovation can achieve this balance by reducing harmful impacts on the environment, while improving the economic efficiency of enterprises and promoting corporate environmental and financial performance (Ahmed et al., 2023; Passaro et al., 2023; Segarra-Oña et al., 2016; Sun et al., 2023; Xu et al., 2023; Zhai et al., 2024). Green innovation as a development strategy enables corporations to develop products and markets in environmentally sustainable ways, which helps them adopt green innovation technologies to gain competitive advantages in the market. Moreover, green innovation can promote the formation of new sustainable consumption patterns in the market, promote the formation of corporations focused on sustainable production methods, facilitate industrial upgrading, and provide momentum to achieve carbon neutrality. Green innovation reduces the damage to the ecological environment while fostering economic development, conserving natural resources, improving resource allocation efficiency, and achieving truly green development. However, because green innovation is generally characterized by high risk, long research and development (R&D) cycles, and high uncertainty (Del Río et al., 2010), corporations often lack the motivation and resources to pursue green innovation. Engaging in green innovation activities not only imposes greater demands on the production factors of enterprises based on their development strategies and using internal and external knowledge (Arfi et al., 2018; Muscio et al., 2017) while effectively expanding market resources, but also requires the joint efforts of multiple organizations to create value together to meet the needs of enterprises engaged in green innovation activities.

Environmental, Social, and Governance (ESG) connects various stakeholders such as governments, corporations, and investors by integrating the concept of sustainable development into corporate strategy formulation and the framework for investors’ decision-making. The goal is to drive corporate social responsibility through stakeholder investment behavior. This trend represents not only a shift in capital markets but also a crucial pathway for companies to achieve sustainable development. Emphasis on corporate sustainability closely aligns with the principles of green innovation. As of the first half of 2023, the number of institutions participating in the Principles for Responsible Investment (PRI) supported by the United Nations reached 5,372. Since 2011, more than 1,200 ESG-related regulations have been implemented. In June 2023, the International Sustainability Standards Board (ISSB) officially released the IFRS Sustainability Disclosure Standard 1—General Requirements for Disclosure of Sustainability-related Financial Information and IFRS Sustainability Disclosure Standard 2—Climate-related Disclosures, marking the launch of the first set of global ESG reporting standards. ESG is becoming an increasingly important standard of participation in global capital markets. This development encourages companies to disclose more comprehensive and in-depth ESG information, thereby enhancing corporate transparency and credibility. An increasing number of companies include ESG information in their sustainability reports, demonstrating their social responsibility towards stakeholders. This trend is expected to affect the relationship between companies and stakeholders, which in turn may affect corporate green innovation. Previous research has primarily focused on the impact of ESG information disclosure on corporate value, financing constraints, and corporate risk (Atif & Ali, 2021; Pedersen et al., 2021; Yu & Van Luu, 2021). However, few studies have addressed the relationship between ESG information disclosure and corporate green innovation in emerging economies, and detailed analyses of the internal mechanisms remain insufficient. The mechanism through which ESG information disclosure promotes corporate green innovation requires urgent investigation. As an emerging market, China faces certain gaps in environmental protection practices, social responsibility fulfillment, and labor income distribution compared to developed countries (Zhang et al., 2023c). In addition, the regulatory mechanisms for corporate green innovation in China are still under development. Therefore, this study focused on the actual situation in Chinese companies and explored whether ESG information disclosure can promote corporate green innovation. It further incorporated financing constraints and analyst attention into the research framework to supplement the existing literature and assist companies in achieving high-quality green transformation.

Green innovation has gradually become an important part of corporate sustainable strategic decision-making, and scholars have focused their research on ESG information disclosure and corporate green innovation. ESG information disclosure can increase the proportion of substantive green innovation within enterprises, optimize the structure of green innovation (Zhang et al., 2024b), improve both the quality and quantity of green innovation (Tan & Zhu, 2022) and promote corporate sustainable development (Chen et al., 2023). Using data from 37 countries between 1990 and 2019 and applying the panel fixed-effects quantile regression method, Long et al. (2023) found that ESG information disclosure significantly promotes green innovation. Using data from the UK and Germany, Chouaibi et al. (2022) confirmed that ESG information disclosure promotes green innovation, thereby influencing corporate financial performance. However, Cohen, using data from U.S. energy companies, explored the inverse relationship between ESG information disclosure and corporate green innovation. It can be seen that the current research presents both a positive promoting relationship and a negative impact relationship between ESG information disclosure and corporate green innovation, and the research conclusions are inconsistent.

Existing studies have mainly focused on the impact of ESG information disclosure on green innovation at the national macro level, or relied on micro-level corporate data from developed countries to examine the role of ESG information disclosure on green innovation. Compared to developed countries, emerging countries have less developed sustainable information disclosure systems and insufficient market-driven motivations for green innovation. However, research on how ESG information disclosure affects corporate green innovation in emerging countries is lacking. Zheng et al. (2023) discovered a bidirectional synergistic relationship between ESG information disclosure and corporate green innovation. However, the impact and mechanisms of ESG information disclosure on corporate green innovation in emerging countries remain unclear. Therefore, it is necessary to study how ESG information disclosure affects corporate green innovation in emerging countries and explore issues such as transmission mechanisms and endogeneity between the two. This study contributes to the body of research on ESG information disclosure and corporate green innovation through an in-depth investigation, further enriching and expanding the research in this field. Therefore, it is necessary to study how ESG information disclosure influences corporate green innovation in emerging countries and explore the transmission mechanisms and endogeneity issues between the two. This study contributes to the literature by enriching and expanding research on ESG information disclosure and corporate green innovation through an in-depth analysis.

As one of the world's key emerging economies, China was the focus of this study. We drew on data from A-share listed companies in China from 2013 to 2022 to empirically explore the impact of ESG information disclosure on corporate green innovation. Commonly used panel regression models in existing research include random effects, two-way fixed effects, and generalized method of moments (GMM) models. The random-effects model addresses individual-level random variations but requires the assumption that individual effects are uncorrelated with explanatory variables, an assumption that is difficult to meet in this study. The GMM model is more suitable for dynamic panel data, but involves greater complexity. The two-way fixed effects model accounts for fixed effects across both the individual and time dimensions, thereby improving the model's explanatory power. In this study, firms’ ESG information disclosure and corporate green innovation are likely to be influenced by unobservable factors that vary across individuals and times. Therefore, the two-way fixed effects model is deemed most appropriate for addressing these factors and enhancing the accuracy of the empirical results. The findings indicate that high-quality ESG information disclosure can significantly promote corporate green innovation. This conclusion remains robust after a series of robustness and endogeneity tests. The mechanism analysis reveals that ESG information disclosure affects corporate green innovation through financing constraints and analysts’ attention. The heterogeneity analysis further demonstrates that ESG information disclosure promotes corporate green innovation more significantly among state-owned enterprises, firms in the Eastern region, and firms in non-heavily polluting industries.

The contributions of this study are as follows: (1) It expands research on the impact of ESG information disclosure on corporate green innovation. Most prior studies on ESG information disclosure have focused primarily on its effects on corporate value, financial performance, and other related aspects. Much of the existing literature has examined how external factors influence corporate green innovation. However, few studies have integrated ESG information disclosure with corporate green innovation. This study explored the impact of ESG information disclosure on corporate green innovation from the perspective of internal corporate strategy, drawing on relevant classical theories, such as stakeholder theory and sustainable development. This enriches the literature on the economic consequences of ESG information disclosure and the factors driving corporate green innovation. (2) It enhances research sample diversity. Previous studies on the impact of ESG information disclosure on corporate green innovation have often focused on macro-level national data or relied on samples from developed countries, with limited attention paid to emerging economies. Using data from China, an emerging market, this study demonstrated how ESG information disclosure promotes corporate green innovation, thus broadening the scope of the research samples. (3) It explores transmission mechanisms between ESG information disclosure and corporate green innovation. This study investigated transmission mechanisms through two key channels—financing constraints and analysts’ concerns—shedding light on the dynamic relationships between these factors and corporate green innovation. (4) It provides practical insights into the heterogeneous effects of ESG information disclosure. This study examined the varying impacts of ESG information disclosure on corporate green innovation across various dimensions including property rights, regional disparities, and industry attributes. These findings enrich research perspectives and offer targeted policy recommendations for corporations to enhance their green innovation capabilities and achieve sustainable transformation.

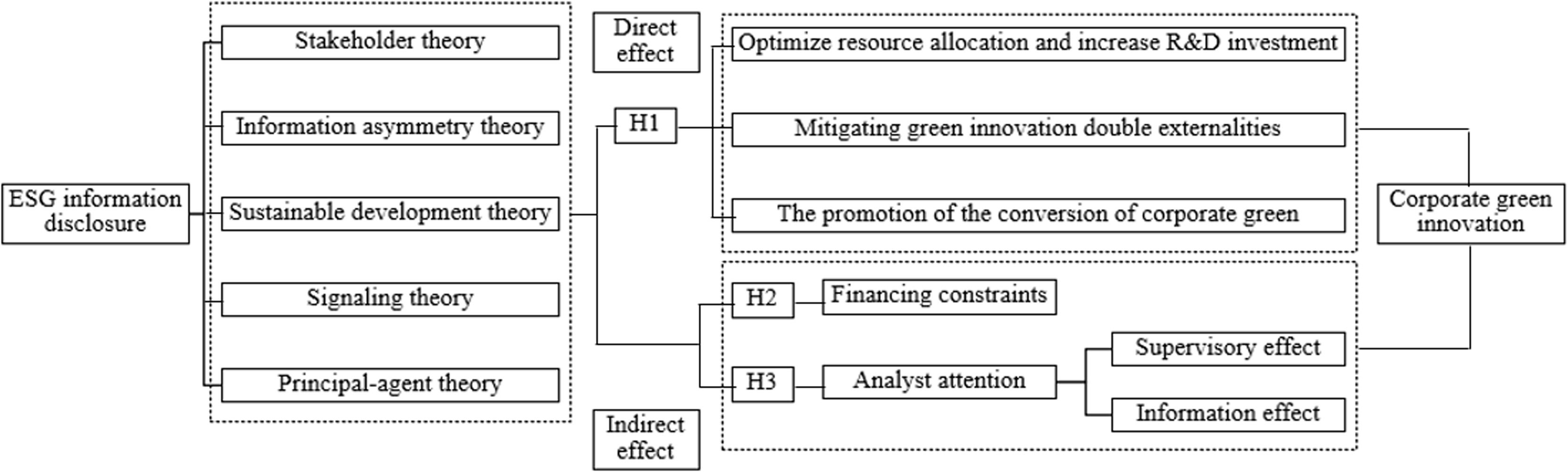

Hypothesis developmentESG information disclosure and corporate green innovationNeoclassical economics states that environmental regulation reduces firms’ resource waste and environmentally harmful behaviors, but crowds out firms’ R&D investment, thereby reducing their competitiveness (Palmer et al., 1995; Petroni et al., 2019). In contrast, the Porter hypothesis argues that environmental regulation positively impacts firms’ innovative activities, not only avoiding crowding out R&D investment but also improving firms’ performance and mitigating the environmental costs incurred in production (Porter & Linde, 1995; Zhao et al., 2023). Both theories suggest that environmental pressures influence firms’ production and innovation activities, which, in turn, affect their economic efficiency and cost-effectiveness. Green innovation differs from traditional production innovation. It focuses on financial benefits while simultaneously emphasizing the creation of environmental benefits, aiming to achieve sustainable development through corporate green innovation. Scholars have primarily explored the impact of external regulations on corporate green innovation from the perspective of environmental policy (Zhang et al., 2023a; 2024a). In contrast, this study investigated the impact of ESG information disclosure on corporate green innovation from the perspective of internal strategy as well as the mechanism through which the two interact.

Stakeholder theory advocates that enterprises should consider not only the rights and interests of shareholders, but also those of other stakeholders, balancing the demands of various interest groups to achieve business goals. Signaling theory suggests that due to information asymmetry, investors have limited information at their disposal, which makes them demand higher returns, potentially raising the firm's cost of capital. Therefore, by disclosing relevant information such as operating conditions, financial performance, and development plans, firms send positive signals to attract investor attention, thereby reducing their capital costs and achieving desired outcomes. From the perspectives of stakeholder and signaling theories, enterprises that actively disclose ESG information can promote corporate green innovation. First, as a strategic investment, ESG optimizes resource allocation and boosts R&D investment. Firms are better positioned to leverage new technologies such as networked digital systems to enhance their competitive advantage (Duan & Li, 2023). Through ESG information disclosure, enterprises communicate their performance in ESG areas to stakeholders, increasing transparency across multiple dimensions and mitigating information asymmetry between enterprises and stakeholders. Moreover, to meet the demands of different stakeholders, corporate decision-making considers the comprehensive interests of multiple parties (Moffitt et al., 2024), leading to greater investments in green innovation and the development of systematic, actionable green innovation strategies. Public awareness of environmental protection is increasing, with consumers placing greater emphasis on whether enterprises operate in an environmentally friendly manner (Li et al., 2016) and demanding the incorporation of environmental factors into production processes (Jabeen et al., 2024). ESG information disclosure is not only recognized by third-party authoritative institutions but also reflects government endorsement of CSR investment results, while simultaneously addressing consumer expectations. Consequently, robust ESG information disclosure enables enterprises to establish a favorable image in the minds of consumers, thereby enhancing brand value. Companies prioritize product quality and increase green innovation in both products and processes to meet consumer demands and maintain a positive social reputation (Zhang & Zhu, 2019). On the other hand, comprehensive ESG information disclosure improves corporate transparency, satisfying investors’ need for risk mitigation (Drempetic et al., 2020) and easing financing pressures. Increased transparency provides firms with more resources to support green innovation activities (Castillo, 2015; Houston & Shan, 2022; Ross, 1977). In summary, ESG information disclosure not only addresses the diverse interests of stakeholders but also motivates companies to proactively engage in green innovation. Enterprises with comprehensive ESG disclosure are better equipped to enhance their public image, gain consumer trust, and foster customer loyalty. This loyalty strengthens cash flow stability and provides a solid foundation for sustained green corporate innovation.

Second, ESG information disclosure helps mitigate the dual externalities of the corporate green innovation process. Double externalities comprise technological and environmental components (Rennings & Rammer, 2011; Sun et al., 2020; Wang et al., 2017). Green innovation outcomes create positive externalities through technological spillovers that may reduce corporations’ incentives for green innovation (Zheng et al., 2021) and hinder the development of corporate green innovation. Effective ESG information disclosure facilitates deeper interactions with external parties and establishes a more comprehensive and robust information exchange network. This enhances corporations’ access to green innovation knowledge, improves green innovation efficiency, and enables them to gain a sustainable competitive advantage. Additionally, ESG disclosure enhances corporate transparency, attracts greater analyst attention, and strengthens external oversight, thereby boosting firms’ green innovation capacity and alleviating the challenges posed by technological spillovers. However, environmental spillovers inevitably generate negative societal impacts, with pollution control costs burdening enterprises, diminishing investor confidence and discouraging green innovation. By contrast, high-quality ESG disclosure allows stakeholders to recognize firms’ positive contributions to social responsibility, thus addressing public pressure arising from stakeholders’ social contract expectations (Atif & Ali, 2021; Reber et al., 2022). By fostering strong partnerships, corporations can secure a stable supply of the resources necessary for green innovation (Anwar & Malik, 2020). Therefore, ESG information disclosure is crucial for addressing the double externality of green innovation and serves as a continuous driver of corporate green innovation efforts.

Finally, ESG information disclosure facilitates the transformation of corporate green innovation results and enables companies to gain differentiated competitive advantages in the market. For corporate green innovation, R&D investment is often limited by the efficiency of innovation outcomes, whereas the motivation and stability of R&D personnel remain key factors in promoting the transformation of green innovation into real productivity. A company's high ESG information disclosure level reflects a stronger commitment to sustainable development. This signals employees’ awareness of green development, enhances their environmental awareness (Liao, 2024), and encourages them to engage in eco-friendly behaviors (Jabeen et al., 2024), thereby fostering greater enthusiasm for corporate green innovation. Moreover, high-quality ESG information disclosure demonstrates that a company values employees’ rights and interests, which can boost their loyalty (Du et al., 2011) and attract talented R&D professionals. This influx of expertise increases a company's intellectual capital (Kuzior, 2022; Trzeciak et al., 2022), further driving green innovation. Additionally, companies can provide employees with a high-quality working environment and fair promotion standards, which strengthen employee retention, reduce the loss of high-precision talent, stimulate the innovative enthusiasm of R&D personnel (Chang et al., 2015), foster a positive cultural environment, and comprehensively enhance their ability to promote green corporate innovation. The selection of R&D projects is also a key factor in determining whether green innovation can be successfully implemented. Previous studies have shown that the success rate of R&D project selection depends on how much information is incorporated into decision-making (Meade & Presley, 2002). ESG information disclosure can help management identify corporate weaknesses and facilitate continuous improvement. It also highlights projects with potential for future development, guiding companies to allocate their limited resources more efficiently to enhance the transformation of corporate green innovation results. Based on the above analysis, Hypothesis 1 was proposed:

H1: Good ESG information disclosure can promote corporate green innovation.

(1) ESG information disclosure, financing constraints, and corporate green innovation

Information asymmetry theory posits that information asymmetry often exists between internal and external firms . This is mainly because green innovation projects are usually characterized by long R&D cycles, high risk, and uncertainty. These attributes exacerbate the information asymmetry between internal and external investors. The complexity and riskiness of corporate green innovation intensify this asymmetry, resulting in enterprises encountering higher financing costs and financing constraints when seeking external financing. Corporate green innovation requires a large capital investment (Jiao et al., 2020), and capital is a key factor affecting green innovation (Huang et al., 2019). ESG information disclosure, such as non-financial information (Drempetic et al., 2020; He et al., 2019), complements financial disclosure by filling the gaps that financial information does not cover. Therefore, ESG information disclosure can serve as an effective information pathway, helping financial institutions understand firms with strong sustainability capabilities (King & Levine, 1993; Ahmed et al., 2018), thus reducing the degree of information asymmetry between firms and creditors. Firms that adopt such practices differentiate themselves from their competitors, secure favorable green credit facilities, and alleviate financing constraints. ESG information disclosure also generates a reputational effect, which positively affects a firm's financial performance. Firms with better ESG practices experience lower capital costs, which ultimately enhance dividend payouts (Ellili, 2022). Institutional investors also prefer firms with high levels of ESG disclosure to mitigate adverse selection (Cornell, 2021). These advantages help to reduce financing costs (Goss & Roberts, 2011; Kim et al., 2019; Wong et al., 2021). According to the signaling theory, companies with high ESG information disclosure levels pay more attention to sustainable development capabilities such as environmental protection, social responsibility, and internal governance than companies with low ESG disclosure levels. This sends a positive signal to the capital market and establishes a good corporate image (Limkriangkrai et al., 2017), which helps gain the trust and support of stakeholders (Dacko-Pikiewicz, 2019; Khan et al., 2022). Such trust improves a firm's reputation and lowers the perceived risk faced by creditors and investors, thereby attracting the attention of potential investors (Kim & Li, 2021). This improved trust also lowers investors’ expected rates of return (Albarrak et al., 2019; Azmi et al., 2021), facilitating access to external financing at reduced costs (Cheng et al., 2014; Dhaliwal et al., 2012; Eliwa et al., 2021) and further easing financing constraints (Tang, 2022).

Schumpeter's innovation theory posits that the difficulty in securing funds is a key factor affecting innovation activities in enterprises. Existing research shows that compared with traditional innovation, corporate green innovation is characterized by large investments, long cycles, high risks, and difficulties in assessment (Jiao et al., 2020). Investors often face information disadvantages and a lengthy investment process makes it challenging for them to evaluate a project's investment value, resulting in enterprises struggling with financing constraints. This constraint limits R&D investment and innovation. According to the theory of financing constraints, when enterprises rely on external financing to secure funds, they may encounter higher financing constraints and abandon high-risk projects even if such projects enhance firm value. Directing enterprise funds toward environmental protection and sustainable development is essential for overcoming the challenges of path dependence, double externalities, and other obstacles to green innovation. This approach helps minimize the negative impact of financing constraints on corporate green innovation. Based on the above analysis, enterprises reduce the degree of information asymmetry through effective ESG information disclosure, which helps alleviate financing constraints by improving transparency and attracting more resources (Gao et al., 2016; Sun et al., 2022). When enterprises secure long-term stable funds, their willingness to engage in innovation increases (Xu & Xu, 2012), thereby promoting corporate green innovation and fostering a virtuous development cycle. Accordingly, Hypothesis 2 was proposed:

H2: Good ESG information disclosure can alleviate financing constraints, thereby promoting corporate green innovation.

(2) ESG information disclosure, analyst attention, and corporate green innovation

Analysts, as crucial information intermediaries in the capital market (Healy & Palepu, 2001; Tsang et al., 2024) and important external watchdogs (Yu, 2008), are drawn to publicly disclosed information on target firms. In recent years, the concept of sustainable development has gained increasing prominence, prompting a growing number of investors to focus not only on corporate financial information but also on ESG information disclosure within their investment decision frameworks (Amel-Zadeh & Serafeim, 2018; Murata & Hamori, 2021). Some professional investors place less emphasis on financial performance and choose to invest at a premium in firms that excel in social responsibility (Riedl & Smeets, 2017). To meet these investor demands, analysts tend to focus on companies with higher levels of ESG information disclosure (Ioannou & Serafeim, 2015). Moreover, high-quality ESG information disclosure reflects enhanced internal governance, increased information transparency, and reduced costs for analysts to access relevant data, further attracting analysts’ attention (Baldini et al., 2018; Li et al., 2022). Companies that demonstrate strong ESG performance are often perceived as having greater enterprise value and lower investment risk, thereby sending positive signals to capital markets. For analysts, profitability and growth potential are of paramount concern, and firms that exhibit strengths in ESG information disclosure are more likely to attract their attention. Analyst attention exerts both informational and supervisory effects on enterprises by fostering corporate green innovation.

Drawing on the information revelation hypothesis from the perspectives of information asymmetry theory and principal-agent theory, two challenges emerge. On the one hand, the complexity and specialized nature of green innovation projects exacerbates information asymmetry, making it difficult for investors, who often lack the necessary expertise, to recognize the potential investment value of these activities. This, in turn, leads to resource shortages for corporate green innovation efforts. On the other hand, green innovation typically requires an extended time horizon to yield benefits (Jiao et al., 2020), and the presence of internal information asymmetry makes it difficult for management to provide owners with clear and accurate valuations of these efforts. However, analysts possess the expertise to publish reports that effectively communicate the value of corporate green innovation to stakeholders, helping to mitigate information asymmetry between corporations and the market. Furthermore, analysts’ extensive experience enables them to detect fraudulent information disclosure practices, influence corporate reputation, and guide investors’ decisions. Analysts’ ability to access comprehensive information also allows them to assess the intrinsic value of corporate green innovation more accurately, helping owners better understand these activities and reducing the principal-agent problem. Finally, analyst attention serves as external oversight, curbing shortsighted behavior by corporate management (Su et al., 2016) and incentivizing management to pursue innovation, ultimately enhancing the corporate green innovation level. Based on the above analysis, Hypothesis 3 was proposed:

H3: Good ESG information disclosure can attract more analyst attention, thereby promoting corporate green innovation.

Based on the above discussion, this study presented a hypothetical framework, as shown in Fig. 1, to support the core arguments of this study.

Research designData and sample

We selected A-share listed companies in China from 2013 to 2022 as our sample. ESG information disclosure was measured using the ESG index published by Sino-Securities Index Information Service (Shanghai) Co. Ltd. (SSIIS). The SSIIS began conducting ESG ratings in 2013, and its coverage is now extended to all A-share-listed companies in China. The index is constructed by referencing international best practices while considering the characteristics of China's capital market and earning broad recognition from both industry and academia (Lin et al., 2021). ESG data were sourced from the WIND financial database, whereas financial information was obtained from the China Stock Market and Accounting Research (CSMAR) database. In China, the WIND and CSMAR are the two most widely used financial databases. Data on corporate green innovation were primarily collected from the China Research Data Services (CNRDS) platform, which draws inspiration from leading platforms such as Wharton Research Data Services, providing a high-quality, open, and platform-based dataset for research in economics, finance, and business in China.

Additionally, to ensure the reliability of the research data and avoid the impact of outliers on the research results, this study conducted the following treatments on the initial research sample collected: (1) Exclusion of special treatment (ST) and ST enterprises: Enterprises classified as ST or *ST are in financial distress, with financial performance significantly differing from other firms, which could introduce uncertainty into the research findings. Therefore, this study excluded listed enterprises with ST and *ST status. (2) Exclusion of financial sector firms: The financial industry has distinctive characteristics, with accounting standards and business operations differing significantly from those of non-financial institutions. Consequently, this study excluded companies listed in the financial sector. (3) Removal of samples with missing data: Samples with missing values for key and control variables were excluded to ensure data completeness. (4) Winsorization to address outliers: To account for outlier interference in the sample, all continuous variables were winsorized at the top and bottom 1%. After these treatments, the final dataset consisted of 9,400 sample observations. Excel and Stata 17 were used for data processing and empirical analyses.

Key variables(1) Dependent variable

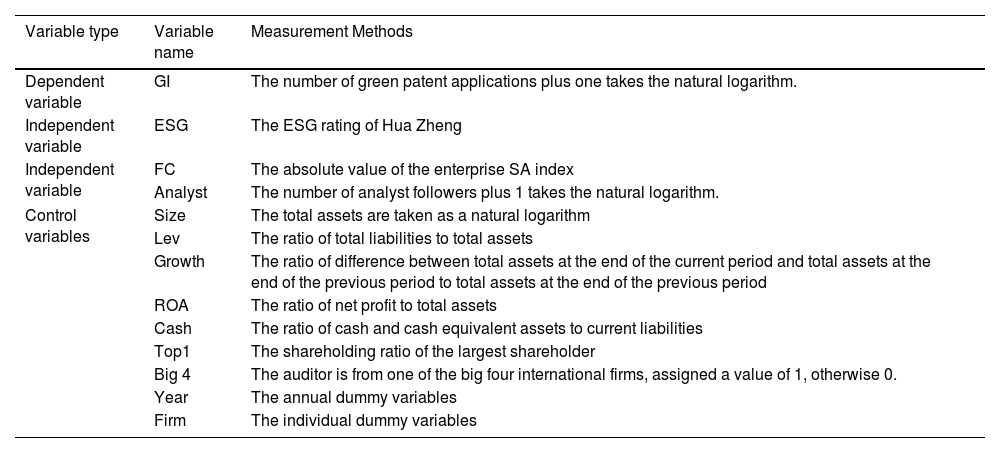

Green Innovation (GI). Current academic research on innovative technologies predominantly measures innovation from both input and output perspectives (Lanoie et al., 2011; Adhikari & Agrawal, 2016; He & Tian, 2013; Zhang et al., 2023b). Given the high uncertainty and lengthy R&D cycles associated with green innovation, relying on input indicators alone may lead to an overestimation of the level of corporate green innovation, with the risk of superficial reporting. Moreover, R&D inputs reflect only the financial resources allocated to innovation activities, and do not necessarily capture the actual outcomes of green innovation. To accurately evaluate the effectiveness of corporate green innovation, this study adopted an output-based approach, focusing on actual results to measure firms’ green innovation levels. Drawing on Zhang et al. (2019) and Wang et al. (2022), this study used the sum of green invention and green utility patent applications to measure the level of green innovation. There were three main reasons for this. First, patents serve as one of the most effective ways to reflect the innovation achievements of enterprises, conveying their innovation efforts to the market. Second, compared with patent applications, patent grants involve time lags and uncertainties and are susceptible to external factors such as the preferences of patent agencies. Third, patented technology can be implemented during the application process, potentially influencing the enterprise performance. Given these considerations, selecting the number of green patent applications as a key indicator of corporate green innovation is critical. As the annual distribution of green patent applications is right-skewed, the natural logarithm of the original value (after adding 1) was used to ensure the accuracy and reliability of the data.

(2) Independent variable

ESG Information Disclosure: In this study, we referred to related research by Lin et al. (2021) and used the ESG ratings published by SSIIS to measure enterprises’ ESG information disclosure. These ratings were based on data from corporate social responsibility reports, sustainability reports, periodic and interim reports, and information provided by government agencies, news media, and other sources. The ESG rating system draws on established ESG rating frameworks and adapts them to the specific characteristics of China's capital markets. SSIIS's ESG ratings are meticulously categorized into three primary areas: environmental, social, and governance. They encompass 14 themes, 26 key indicators, and over 130 sub-indicators, providing a comprehensive coverage of China's A-share listed companies. This assessment framework ensured data continuity and accessibility. Accordingly, this study adopted SSIIS ESG ratings as the primary measure of ESG information disclosure to enhance the scientific validity and reliability of the empirical results. Additionally, the findings of this study contribute to improving the ESG evaluation system and offer empirical support for future research.

(3) Control variables

Drawing on relevant studies (Zhang et al., 2020; Wu et al., 2024), this study focused on factors in corporate operations and governance that are closely related to corporate green innovation when selecting control variables. (1) Firm size (Size). As corporate green innovation is characterized by high investment and risk, it requires sufficient capital investment and human resource support throughout the innovation process. Larger firms generally possess more abundant resources and stronger risk-bearing capacity, both of which play crucial roles in facilitating corporate green innovation. (2) Leverage ratio (Lev). The leverage ratio reflects a firm's solvency. While moderate financial leverage can compensate for a shortage of funds, a high leverage ratio signals poor financial health, exposing the firm to heavy debt repayment pressure, weakening its investment capacity and making it difficult to maintain stable and adequate funding for green innovation activities. (3) Firm growth (Growth). Firm growth significantly influences corporate green innovation. Firms with higher growth tend to adopt more advanced development concepts, possess greater technological capabilities, and maintain richer talent reserves, all of which encourage them to explore projects with high potential. (4) Return on assets (ROA). Profitability is a key indicator of a company's financial strength. Firms with high profitability typically have sufficient capital, making them more capable of engaging in high-risk, high-return green innovation activities. (5) Cash ratio (Cash). This ratio reflects the adequacy of a firm's disposable cash flow. Firms with higher cash ratios are better positioned to meet the substantial capital demand for green innovation, thereby providing solid financial support for these activities. (6) Ownership concentration (Top1). Concentration of ownership reflects the stability of a firm's governance structure, which helps mitigate the principal-agent problem and enables firms to focus more on green innovation, thereby enhancing sustainable development. However, excessive ownership concentration may result in shareholder dominance, whereby large shareholders prioritize self-interest at the expense of a firm's long-term development, potentially undermining green innovation investment. (7) Auditor affiliation with a Big 4 Firm (Big 4). Auditors with extensive professional experience can significantly influence corporate green innovation. Therefore, this study controlled for whether a firm's auditor is a Big 4. (8) Year and firm fixed effects. Given that corporate green innovation strategies may vary significantly across years and firms, this study controlled for both year and firm fixed effects.

(4) Intermediary variable

Financing constraints. Currently, the measurement of financing constraints has not yet formed a unified standard, and the measurement indices widely accepted by scholars include Kaplan and Zingales (1997) KZ index, White and Wu (2006) WW index. However, these constructed indices share a common shortcoming in that they incorporate financial variables with endogenous characteristics, such as cash flow and total assets, which are susceptible to endogeneity and affect the robustness of the research results. Therefore, we adopted Hadlock and Pierce's (2010) SA index to measure financing constraints. The SA index consists of two strongly exogenous indicators, namely the number of years since listing and the size of the firm, which help mitigate the endogeneity problem and reduce the influence of subjective factors to a certain extent. Moreover, this index aligns well with the characteristics of China's capital market and has been widely used in academic research. The specific calculation method was as follows: This study employed the absolute value of the SA index as a metric, with a higher absolute value indicating that enterprises face greater financing constraints.

Analyst Attention. This study drew on studies such as Lin et al. (2014), who suggested that analyst attention can be measured by the number of tracking analyses conducted in a year. When analysts publish rating reports through a team, their attention is counted as one. For example, if 20 analysts from 20 brokerage firms issued 50 rating reports on the China BG Group in 2022, they were treated as 20 analysts following the China BG Group regardless of the total number of reports issued or analysts involved. To reduce the magnitude of the data and ensure data smoothness, the number of analysts plus one was used to calculate the natural logarithm to measure analysts’ attention in the subsequent empirical analysis. The main variables and measurements selected for this study are presented in the Appendix.

Model designThis study used panel data on A-share listed companies from 2013 to 2022. To test Hypothesis 1 (i.e., the effect of ESG information disclosure on corporate green innovation), a two-way fixed effects model was constructed, as shown in Model (1):

In Model (1), i denotes different enterprises, and t denotes the year. The independent variable ESGi,t is ESG information disclosure, dependent variable GIi,t is corporate green innovation, Controlsi,t is the control variable, Year denotes the control year, and Firm denotes the control individual. In Model (1), if it is significantly positive, it means that good ESG information disclosure can effectively promote corporate green innovation; that is, it verifies Hypothesis 1.

To test Hypothesis 2 (i.e., to verify whether financing constraints play a mediating role in the relationship between ESG information disclosure and corporate green innovation), this study adopted the stepwise regression method proposed by Baron and Kenny (1986) and constructed a model of the mediating effect based on Model (1). The specific model forms are expressed in Eqs. (2) and (3). Among them, FCi,t is the financing constraint, and the other variables are consistent with previous studies.

To test Hypothesis 3, that is, to verify whether analysts’ concerns play a mediating role in ESG information disclosure and corporate green innovation, and then combine this with Model (1) to construct the mediation effect model, the specific models are shown in (4) and (5), where Analysti,t is analyst concern, and other variables are consistent with the previous paper.

Empirical resultsDescriptive statistics

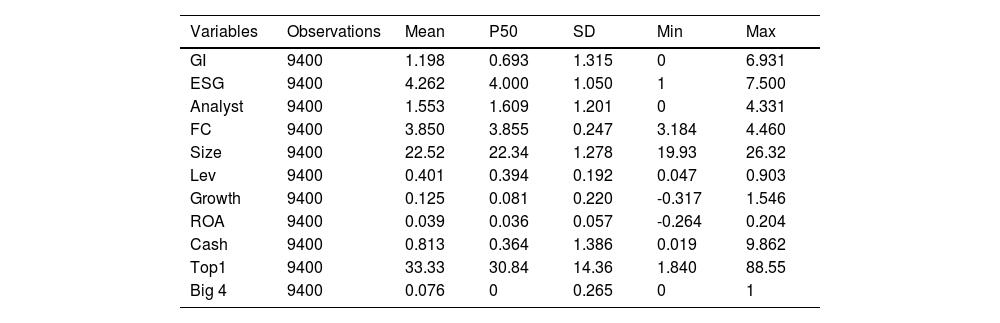

Table 1 presents the descriptive statistics for the main variables used in the model established in this paper. The mean value of the sample of corporate green innovation (GI) was 1.198, with a minimum of 0 and a maximum of 6.931, indicating a relatively low overall level. Furthermore, green innovation levels varied significantly among the different sample firms. The median was 0.693, which was smaller than the mean, indicating that a significant proportion of sample firms still have ample room for development when adopting green strategies. The mean value of ESG information disclosure was 4.262, with a median of 4, suggesting that the sample firms generally achieved a moderate level of ESG information disclosure. However, the minimum value of ESG information disclosure was 1 and the maximum was 7.500, indicating that ESG disclosure scores vary widely and that firms assign different levels of importance to ESG disclosure. The mean value of financing constraints (FC) was 3.850, with a minimum of 3.184 and maximum of 4.460, highlighting the significant differences in financing constraints across sample firms. The mean value of analyst attention (Analyst) was 1.553, with a minimum of 0 and maximum of 4.331, suggesting significant variation in analyst attention across firms. In addition, the analyst attention data exhibited a right-skewed distribution. To address uneven data distribution and prevent missing sample data, this study transformed the analyst attention measure by taking the natural logarithm after adding one to the original value.

Descriptive statistics.

Among the control variables, the mean enterprise size was 22.52, with a minimum value of 19.93 and a maximum value of 26.32. This indicates that the total assets of the sample enterprises varied considerably. To mitigate the estimation errors caused by this asset disparity, total assets were logarithmized. The mean Lev was 0.401 and the median was 0.394, suggesting that the overall leverage level of the sample enterprises is moderate. Growth reflected the growth capability of the sample enterprises, with a mean value of 0.125, a minimum value of -0.317, and a maximum value of 1.546, indicating that the sample enterprises possess good development potential, although their growth capacity varies significantly. Return on Assets (ROA) represents the profitability of the sample enterprises. The mean ROA was 0.039, with a minimum of -0.264 and a maximum of 0.204, suggesting that the dataset included enterprises experiencing losses or revenue declines and that there was significant variability in profitability among them. The mean Cash was 0.813, with a minimum of 0.019 and a maximum of 9.862, highlighting a substantial gap in the cash flow held by the sample enterprises. The mean Top1 was 33.33%, with a minimum of 1.84% and maximum of 88.55%, indicating considerable variation in equity concentration across firms. Lastly, Big 4 had a mean value of 0.076, with a minimum of 0 and a maximum of 1, showing that 7.6% of the sample firms are audited by one of the Big 4 international accounting firms.

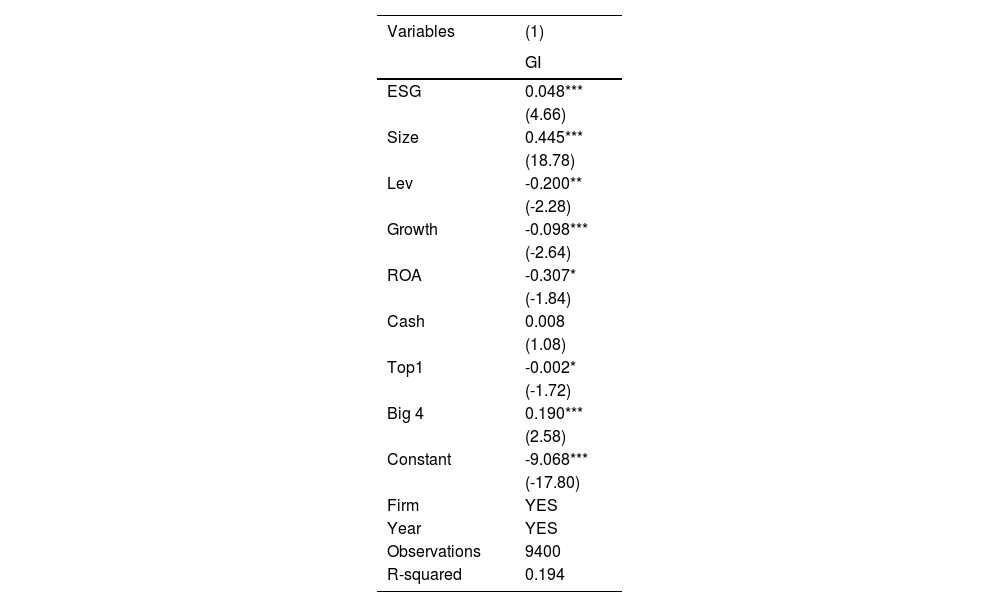

Baseline testTable 2 presents the regression results of the impact of ESG information disclosure on firms’ green innovation. As Column (1) of Table 2 shows, the coefficient of ESG information disclosure on corporate green innovation was 0.048, which was statistically significant at the 1% level. This suggests that good ESG information disclosure promotes corporate green innovation. Specifically, higher ESG ratings issued by the SSIIS can increase the number of corporate green patent applications, thereby confirming the validity of Hypothesis 1. The underlying reason for these results is that effective ESG information disclosure enables enterprises to showcase their positive efforts toward environmental protection, social responsibility, and corporate governance. Such disclosures communicate the firm's values and strategic goals to stakeholders, thereby enhancing its reputation and business credit. When an enterprise actively discloses ESG information, stakeholders, such as investors, creditors, customers, employees, and communities, are more inclined to trust and support the firm, which in turn promotes sustainable development. Through effective ESG disclosures, enterprises can highlight the long-term value and potential benefits of green innovation activities, making it easier to obtain financial support. ESG information disclosure also sends positive external signals, encouraging creditors to lend funds to enterprises, ultimately reducing their debt capital costs and alleviating financing constraints. On the other hand, the alignment between ESG development goals and corporate green development strategies further demonstrates that enterprises with proactive ESG disclosure exhibit greater willingness and ability for green innovation. Such enterprises are better positioned to gain competitive advantages, attract high-caliber technological talent, retain employees, and foster positive and innovative working environments. Therefore, effective ESG information disclosure helps enterprises to leverage their achievements and drive green innovation.

Baseline test.

t-statistics in parentheses, *** p<0.01, ** p<0.05, * p<0.1

Among the control variables, size was positively correlated with enterprise green innovation and was statistically significant at the 1% level. This indicates that larger enterprises have greater capital resources, enabling more investment in R&D, and fostering green innovation. Lev was significantly negatively correlated with enterprises’ green innovation, exerting an inhibitory effect at the 5% significance level. This finding suggests that enterprises with high financial leverage face heavier debt costs and risks, leaving insufficient funds for green innovation activities, hindering their development. Top1 had a significant negative correlation with green innovation. This implies that when equity is less concentrated, principal-agent problems among major and minor shareholders, management, and investors are mitigated, which discourages short-sighted behavior and enhances corporate sustainability, thereby promoting green innovation. Big4 was significantly positively correlated with green innovation and statistically significant at the 1% level. This finding indicates that higher audit quality improves corporate transparency and reputation, which, in turn, facilitates corporate green innovation.

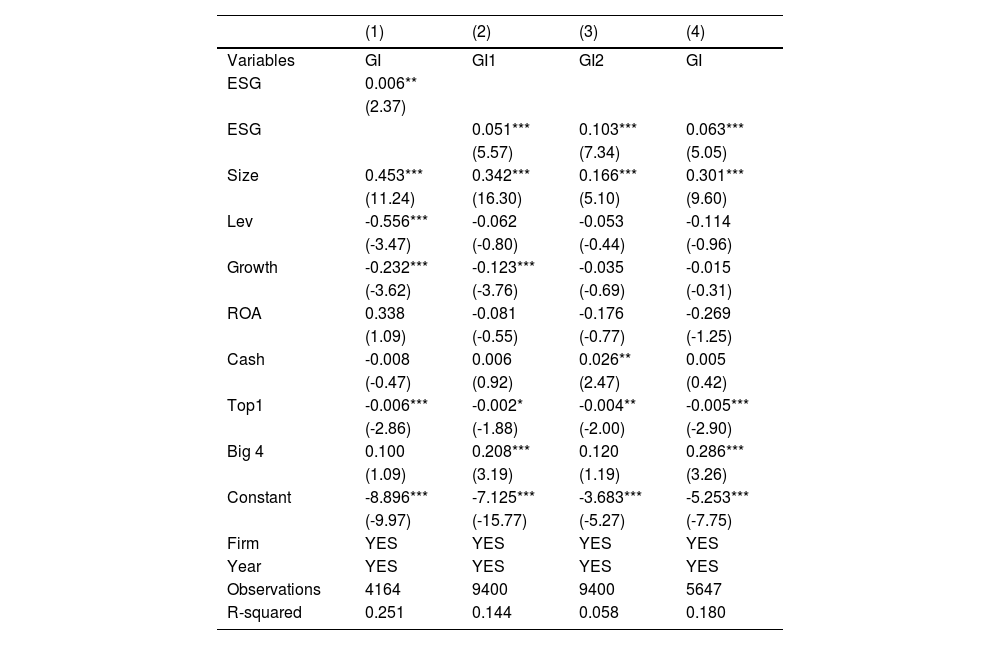

Robustness tests(1) Changing the measurement of the independent variable

Drawing on Yu et al. (2018), this study used Bloomberg ESG scores to remeasure corporate ESG information disclosure. The Bloomberg ESG score ranges from 0 to 100 and this evaluation system covers a wide range of qualitative and quantitative indicators that comprehensively reflect the overall situation of enterprises. This scoring system has been widely used in the existing literature, and its validity has been verified. Therefore, it can be used as a proxy for the dependent variable ESG information disclosure. The sample was re-analyzed by regression, replacing the original independent variable. Column (1) of Table 3 presents the regression results using the Bloomberg ESG score as the dependent variable. After replacing the independent variables, the coefficient of ESG information disclosure and corporate green innovation was 0.006, and both passed the 5% significance level. This indicates that, even after replacing the independent variables, ESG information disclosure alleviates information asymmetry between firms and stakeholders, enhances positive signals to the outside world, and significantly promotes corporate green innovation. The regression results are consistent with the benchmark regression results above, further confirming the positive impact of ESG information disclosure on corporate green innovation and the robustness and reliability of the main effect results.

(2) Changing the measurement of the dependent variable

Robustness tests.

According to previous studies, the difficulty and requirements for invention patent applications are relatively high, and they are more capable of demonstrating enterprises’ levels of innovation than utility patents, which are substantial innovations. Similarly, the number of green invention patent applications represents corporate green innovation development through green transformation, thereby promoting corporate green innovation. In this study, we used the natural logarithm of the number of invention-based green patent applications plus one to re-measure the level of corporate green innovation and re-regress the sample. Column (2) of Table 3 reports the regression results with invention-based green patent applications as the dependent variable. After replacing the dependent variable, the coefficient of ESG information disclosure and corporate green innovation was 0.051, significant at the 1% level. Additionally, as the number of green innovation applications is an absolute indicator, it measures the level of corporate green innovation output. To make the test results more robust, this study adopted the ratio of the number of green patent applications to R&D investment, and then took the natural logarithm as a measure of corporate green innovation indicators from the perspective of green innovation efficiency. The larger the ratio, the stronger the corporate green innovation ability. The sample was regressed after replacing the original dependent variables. Column (3) of Table 3 reports the regression results for the dependent variable, measured from the perspective of green innovation efficiency. The coefficient of ESG information disclosure and corporate green innovation was 0.103, significant at the 1% level. The above results showed that after replacing the dependent variable indicators, good ESG information disclosure can still enhance the trust of stakeholders, such as creditors, investors, and consumers; alleviate the financing constraints of enterprises; attract more analysts to pay attention to the enterprise; exert the supervisory and informational effects of analysts; and play a significant role in the promotion of corporate green innovation. The regression results were consistent with the above regression results, further proving the reliability and robustness of the main effects regression results.

(3) Elimination of zero values

As some corporate green innovations have not been carried out, there are no green innovation patent applications. To eliminate the interference of this part of the value, we excluded enterprises with zero green patent applications during the sample period and conducted a regression analysis to further enhance the robustness of the regression results. The regression results are shown in Column (4) of Table 3, where the coefficient of ESG information disclosure and corporate green innovation was 0.063, which was significant at the 1% level. These results showed that after excluding enterprises with zero green innovation applications in the sample, ESG information disclosure can still help enterprises obtain innovation information, improve innovation efficiency, mitigate the double externality in the process of green innovation, and significantly promote enterprises’ green innovation.

Endogeneity test(1) Instrumental variable approach

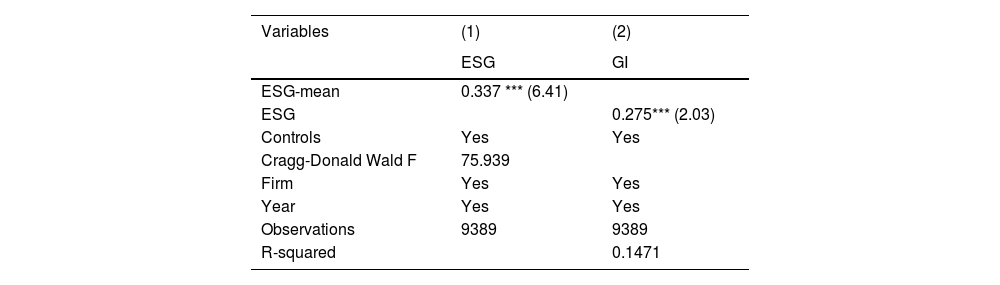

Given the research on the relationship between ESG information disclosure and corporate green innovation, endogeneity issues, such as omitted variables, may exist. This study used a two-stage instrumental variable regression to mitigate this endogenous effect. Specifically, the average ESG value of other firms in the same industry in the same year was chosen as the instrumental variable in this study. The rationale for this variable selection is that the ESG information disclosure of other firms in the same industry in the same year can reflect the level of ESG practices in the entire industry, which in turn may affect the ESG information disclosure decision of this firm and thus has a strong correlation. Simultaneously, this instrumental variable was not directly related to the corporate green innovation activities of this enterprise, thus ensuring its exogenous nature. Therefore, this study selected the average ESG value of other enterprises in the same industry in the same year as an instrumental variable and used it to conduct a regression test to improve the robustness and validity of the research results.

The regression results are shown in Table 4. Column (1) presents the results of the first-stage regression using the average ESG value of other firms in the same industry in the same year as an instrumental variable. This result showed that the coefficient between the average ESG value of other firms in the same industry in the same year and ESG information disclosure was 0.337, which was significantly positive at the 1% level. This finding indicates a significant effect of the average ESG value of other firms in the same industry in the same year on ESG information disclosure in the current period, further validating the relevance of the instrumental variables. In addition, the Cragg-Donald Wald F-statistic was 75.939, which was significantly greater than the F critical value at the 10% confidence level. This indicated that the instrumental variables selected in this study were not weak. The results of the second-stage regression are presented in Column (2) of Table 4. After eliminating potential endogeneity issues that may exist, the coefficient of ESG information disclosure and corporate green innovation was 0.275, significant at the 1% level. Based on the above results, it can be seen that after mitigating the endogeneity problem through instrumental variables, high-quality ESG information disclosure still exerts a signaling effect, shapes a positive image of the firm, and at the same time attracts more R&D personnel, which has a significant positive impact on corporate green innovation.

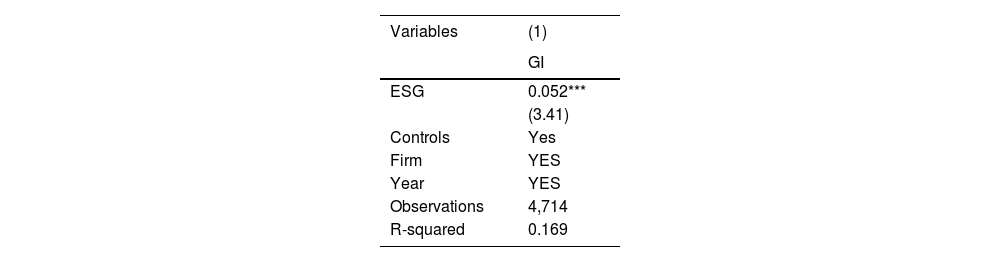

(2) Propensity score matching

To address the possible endogeneity problem caused by sample self-selection, this study mitigated this problem using the propensity score matching (PSM) method. Specifically, the median ESG information disclosure of the sample firms was used as the critical value to construct the experimental and control groups; those larger than the critical value were assigned a value of 1, and those smaller than the critical value were assigned a value of 0. Size, LEV, Growth, ROA, Cash, Top1, and Big 4 were used as covariates for matching. The results are shown in Table 5. The regression coefficient of ESG information disclosure was 0.052, which was significantly positive at the 1% level. These results showed that after mitigating the endogeneity problem arising from sample self-selection through the PSM method, ESG information disclosure can still mitigate information asymmetry between internal and external enterprises, reduce the cost of corporate financing, enhance the external image of enterprises, and promote corporate green innovation.

Future analyses and testsMechanism analysis(1) Financing constraints

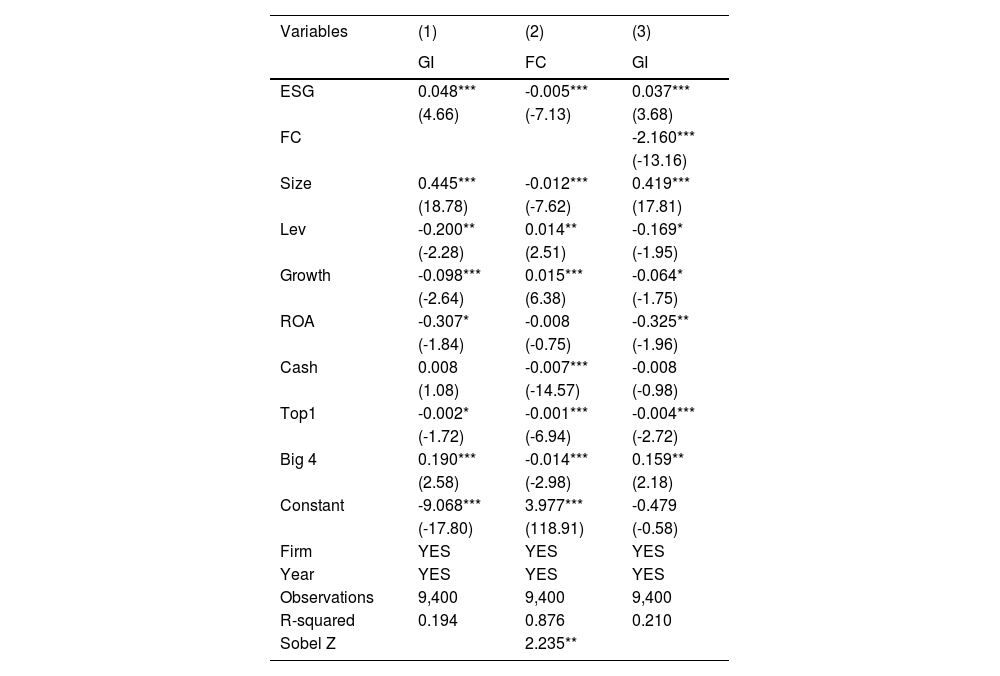

After the main effects regression, the transmission mechanism of financing constraints was tested. The regression results in Column (2) of Table 6 show that the correlation coefficient between corporate ESG information disclosure and financing constraints was -0.005, which was significantly negative at the 1% level, indicating that good ESG information disclosure by corporations helps alleviate corporate financing constraints. The regression results in Column (3) of Table 6 show that after introducing the mediating variable of financing constraints in Column (1) of the main regression, the coefficient of ESG information disclosure was 0.037 and was significant at the 1% level, and the coefficient of financing constraints on corporate green innovation was -2.160, which was significant at the 1% level. The adjusted goodness-of-fit R2 increased from 0.194 to 0.210, which indicates that the model's overall regression effect was better. Therefore, according to the stepwise regression method, both corporate ESG information disclosure and financing constraints significantly affect corporate green innovation, with financing constraints playing a partial mediating role in the positive effect of ESG information disclosure on corporate green innovation, which verifies Hypothesis 2. Corporations actively undertake ESG responsibility to alleviate financing constraints and provide resources for green innovation, which, in turn, improves the level of corporate green innovation.

The transmission mechanism of financing constraints.

Good ESG information disclosure can significantly reduce information asymmetry between the enterprise and various stakeholders, thus enhancing the investment efficiency of the enterprise. For enterprises, good ESG information disclosure not only conveys to the outside world its commitment to sustainable and high-quality development but also attracts the attention and support of investors, governments, and institutions, optimizing the financing environment and easing the financing pressure of enterprises. Investors are more inclined to invest in enterprises with broad development prospects and transparent information disclosures. Therefore, to win investors’ trust and long-term investments, enterprises should be more motivated to strengthen ESG information disclosure and continuously improve their corporate green innovation levels. Good ESG information disclosure can reduce information asymmetry inside and outside the enterprise, obtain more support from stakeholders, reduce financing pressure, obtain resource support, and improve corporate green innovation levels.

To ensure the accuracy of the research conclusions and further verify the reliability of the mediation effect, this study employed the Sobel test and Bootstrap method for reexamination. As shown in Table 6, the results of the Sobel test indicated a Z-statistic of 2.235, which was statistically significant at the 5% level. The Bootstrap test results presented in Table 7 show that the 95% bias-corrected confidence interval for the indirect effect was (0.0004532, 0.0035143), and for the direct effect, it was (0.094469, 0.141745), with no interval including zero. Both methods confirm the validity and robustness of the transmission mechanism of financing constraints. Good ESG information disclosure not only directly enhances corporate green innovation but also indirectly influences it by alleviating financing constraints, indicating that financing constraints play a mediating role between ESG information disclosure and green innovation.

(2) Analyst attention

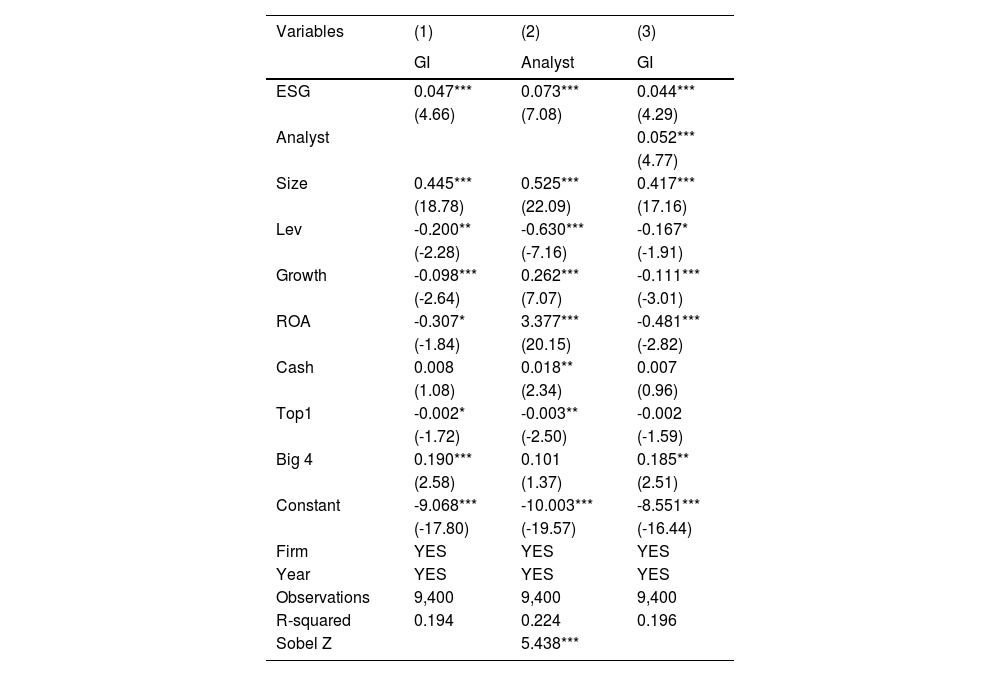

After the main effects regression, the transmission mechanism of analyst attention was tested. The regression results in Column (2) of Table 8 show that the correlation coefficient between firms’ ESG information disclosure and analyst attention was 0.073 and significant at the 1% level, indicating that firms’ good ESG information disclosure attracts more analyst attention. The regression results in Column (3) of Table 8 show that after introducing the mediating variable of analyst attention in Column (1) of the main regression, the correlation coefficient of ESG information disclosure was 0.044, which was significant at the 1% level; the correlation coefficient of analyst attention to green innovation was 0.052, which was significant at the 1% level; and the adjusted goodness-of-fit R2 increased from 0.194 to 0.196, indicating that the model's overall regression effect was better. The results indicate that ESG information disclosure and analyst attention significantly affect green innovation; good ESG information disclosure attracts more analyst attention, and analyst attention has a partial mediating role between ESG information disclosure and corporate green innovation, which verifies Hypothesis 3.

The transmission mechanism of analyst attention.

The specific reason is that, on the one hand, when investors make decisions, they not only pay attention to the disclosure of corporate financial information but also incorporate ESG information disclosure into the investment decision framework. Good ESG information disclosure is a positive signal to the outside world, which shows the commitment and actual action of the enterprise to ESG responsibilities; such disclosure can attract more analyst attention. As professional financial and industry analysts, their attention enhances information transparency and liquidity, which is conducive to transferring information to disadvantaged stakeholders, thereby alleviating the problem of information asymmetry. On the other hand, analyst attention makes companies more transparent and standardized in terms of ESG information disclosure. Analysts, as professional third-party monitors, monitor and evaluate the business behaviors and decisions of enterprises by digging deeper and analyzing their ESG information disclosure. Such monitoring and assessment will prompt enterprises to pay more attention to core issues, such as environmental protection, social responsibility, and corporate governance, thus motivating them to continuously improve their green innovation capability and realize sustainable development. It can be seen that good ESG information disclosure can attract more analysts’ attention, and analysts’ attention will have an information and monitoring effect on the corporate, promoting the corporate green innovation level.

Similarly, to ensure the accuracy of the findings, this study utilized the Sobel and Bootstrap tests for the mediation effect retest. As shown in Table 8, the Sobel test results indicated a Z-statistic of 5.438, which was statistically significant at the 1% level. The Bootstrap test results presented in Table 9 show that the 95% bias-corrected confidence interval for the indirect effect was (0.005664, 0.011399) and that for the direct effect was (0.088826, 0.132643), with no interval including zero. Both methods confirmed the validity and robustness of the transmission mechanisms of analysts’ attention. Good ESG information disclosure not only enhances corporate green innovation directly but also indirectly influences corporate green innovation by attracting more analysts, indicating that analyst attention plays a mediating role between ESG information disclosure and green innovation.

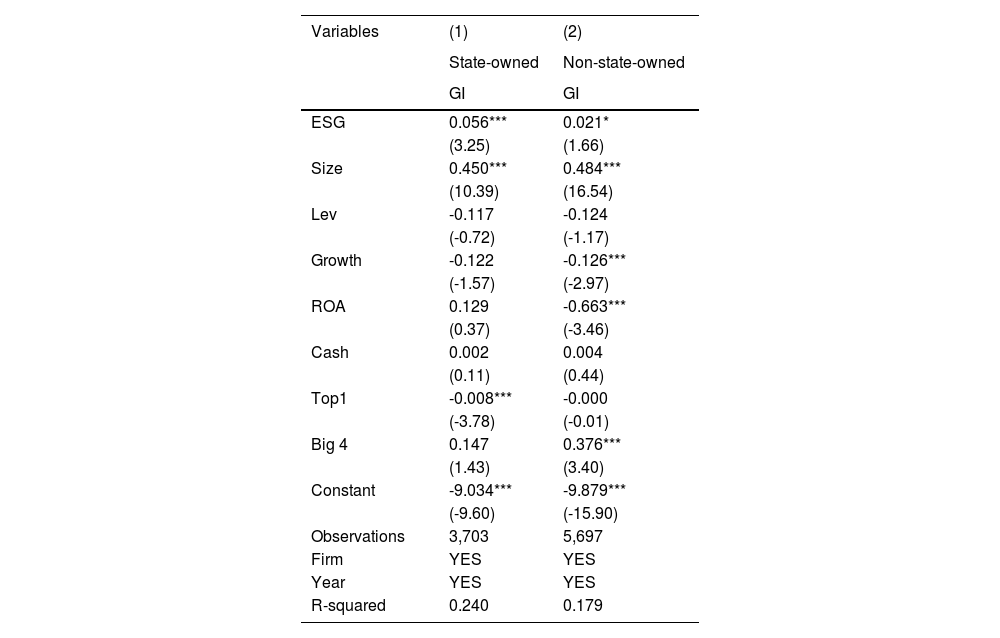

Heterogeneity analysis(1) Nature of property rights

Considering that there may be differences in the relationship between ESG information disclosure and corporate green innovation among corporations with different ownership backgrounds, this study classified the sample corporations into state-owned and non-state-owned enterprises based on the nature of their ownership and used dummy variables to make the distinction, where 1 represents state-owned enterprises and 0 represents non-state-owned enterprises. Table 10 presents the regression results for the effect of heterogeneity such as property rights on the relationship between ESG information disclosure and green innovation. Column (1) shows the results of the analysis for state-owned enterprises, and Column (2) shows the results of the analysis for non-state-owned enterprises. The subgroup regression results show that state-owned and non-state-owned enterprises presented different characteristics in the relationship between ESG information disclosure and green innovation. ESG information disclosure by state-owned enterprises significantly promoted corporate green innovation at the 1% level, with an estimated coefficient of 0.056. ESG information on non-state-owned enterprises significantly promoted corporate green innovation at the 10% level, with an estimated coefficient of 0.021.

Analysis of heterogeneity like property rights.

Specific reasons for the analysis: First, state-owned enterprises, by their special status, must participate in market competition and accept the state's macro-control. Therefore, while pursuing economic benefits, state-owned enterprises have greatly increased their emphasis on social benefits. Against the background of carbon neutrality, state-owned enterprises (SOEs) are actively improving their ESG information disclosure to achieve the country's overall economic goals. SOEs regard green innovation as an important means of realizing sustainable development and have invested large amounts of resources in R&D. Meanwhile, non-state-owned enterprises consider profit maximization their primary goal and focus more on short-term projects that can quickly bring economic gains. Due to its high input and high-risk nature, corporate green innovation has received relatively little attention from non-state-owned enterprises. By contrast, the close political ties between SOEs and local governments make their top managers more susceptible to the influence of the political market when making decisions, and they tend to choose projects that can enhance political interests while ignoring economic benefits. This factor promotes the development of green innovation activities by SOEs and their integration into the core corporate strategy. Additionally, the state-owned attributes of SOEs make it easier for them to receive government subsidies, tax incentives, and investor support, thereby promoting green corporate innovation. Although the promotion of corporate green innovation by non-state-owned enterprises assuming ESG responsibilities is not significant, good ESG information disclosure still helps enhance corporate image and alleviate financing constraints, thus stimulating their motivation to improve economic efficiency and green innovation.

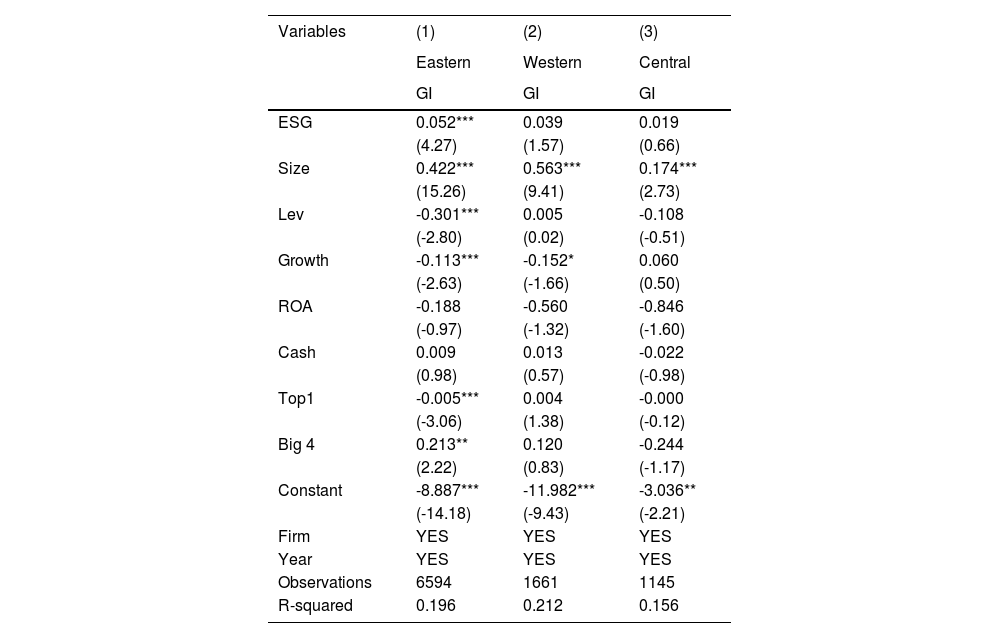

(2) Region

In China, economic development status, policy environment, and leading industries differ in the eastern, western, and central regions, and the effects of corporate ESG information disclosure on corporate green innovation differ for companies located in different regions. In this study, the sample firms were divided into three regions–eastern, western, and central–according to the provinces and municipalities where they are registered. Table 11 reports the results of the regional heterogeneity analysis. Column (1) shows the effects of corporate ESG information disclosure on corporate green innovation among firms in the eastern region. Column (2) presents the impact of corporate ESG information disclosure on green innovation for corporations in the western region. Column (3) shows the effect of corporate ESG information disclosure on green corporate innovation in the central region. According to the group regression results, ESG information disclosure by enterprises in the east significantly promoted corporate green innovation at the 1% level, and the estimated coefficient of the two was 0.052, while ESG information disclosure by enterprises in the west and center did not significantly promote corporate green innovation.

Analysis of heterogeneity in the region.

Specific reason for the analysis: The eastern region is experiencing rapid economic development, and industrial development focuses on high-tech fields, including energy saving, environmental protection, medical research, and new materials. In these fields, corporate green innovation and ESG concepts are increasingly emphasized, reflecting their emphasis on sustainable development and social responsibility. Simultaneously, the eastern region has a perfect market mechanism and policy environment, and the government's support for green innovation is relatively strong. As a result, corporations in the eastern region achieved higher performance in green innovation through good ESG information disclosure. At the center, the manufacturing industry is more advanced and includes traditional machinery, mining, and smelting. Although new energy and other industries have gradually developed in Central China in recent years, the industrial structure of the region remains dominated by manufacturing. Although the western region is rich in mineral resources and clean energy, such as wind and solar energy, these resources have not been fully developed and utilized. Simultaneously, the western region still faces challenges in enhancing its green innovation capacity and lacks efficient methods. The limited number of local enterprises engaged in green innovation R&D, attributable in part to abundant energy reserves and low labor costs, has led to a traditional development model that is still dominant and has a relatively slow pace of transformation, with corporations often preferring to improve efficiency by reducing costs rather than carrying out green innovation. Additionally, the western region suffers from a shortage of human resources and backward economic development. This has led to the more common phenomenon of brain drain, which further inhibits enthusiasm for green innovation. Therefore, the promotion of corporate green innovation through ESG information disclosure by enterprises located in the western and central regions is not significant.

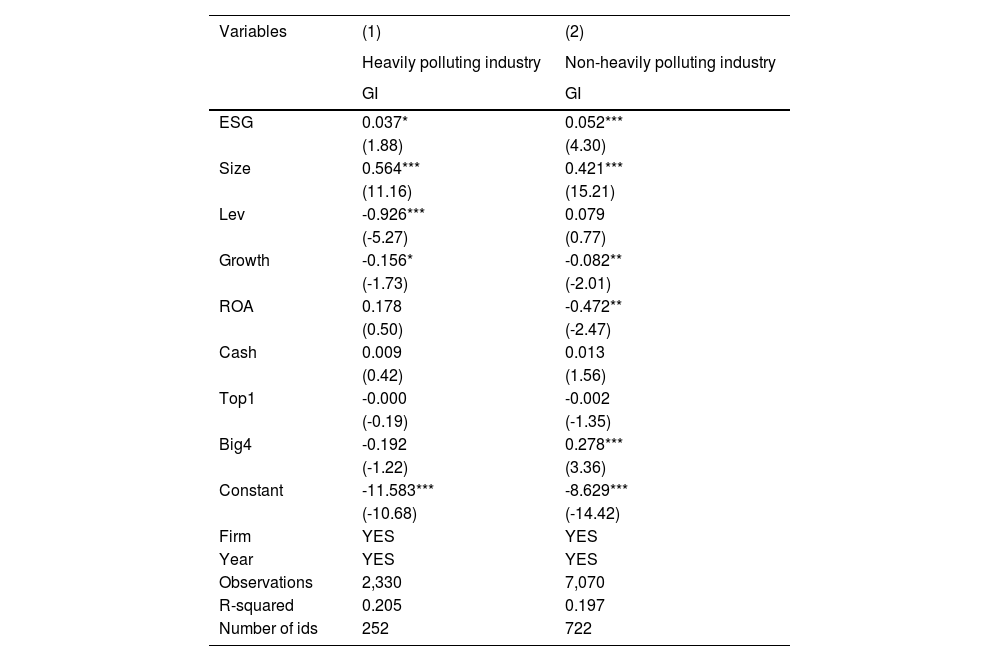

(3) Heavily polluting industry

Considering that the effect of ESG information disclosure on corporate green innovation may differ across industries, this study distinguished the degree of pollution among enterprises. We drew on related research to classify 15 types of industries, such as coal mining and washing and oil and gas development, as heavy polluting industry enterprises and other industry enterprises as non-heavily polluting industry enterprises. Distinctions were made with dummy variables 0 and 1, where 1 represents heavily polluting industry firms and 0 represents non-heavily polluting industry firms. Table 12 reports the results of the industry heterogeneity analysis. Column (1) shows the effect of ESG information disclosure on corporate green innovation for firms in heavy-polluting industries, and Column (2) shows the effect of ESG information disclosure on corporate green innovation for firms that are not in heavy-polluting industries. According to the group regression results, ESG information disclosure by firms in non-heavily polluting industries significantly promoted corporate green innovation at the 1% level, and the estimated coefficient of the two was 0.052. The ESG information disclosure by firms in heavily polluting industries significantly promoted corporate green innovation only at the 10% level, with an estimated coefficient of 0.037.

Analysis of heterogeneity in the industry.

Specific reasons are analyzed as follows: on the one hand, due to the factor of industry attributes, the business of enterprises in heavily polluting industries often involves a large amount of environmental damage and resource depletion, and will face greater institutional constraints. Enterprises in these industries need to invest more in enhancing the quality of ESG information disclosure by disclosing more information to demonstrate their commitment and actions toward environmental protection and sustainable development. By contrast, firms in non-heavily polluting industries face less pressure. At the same time, enterprises in non-heavily polluting industries pay more attention to environmental protection and sustainable development and can establish a better corporate image. Therefore, when non-heavily polluting enterprises disclose good ESG information, they accumulate better reputation and receive more support from social resources. Compared with corporations in heavily polluting industries, those in non-heavily polluting industries face less financial pressure for green innovation. Thus, ESG information disclosure by corporations in non-heavily polluting industries has a more significant impact on corporate green innovation. On the other hand, good ESG information disclosure can reflect the governance level and transparency of enterprises. For enterprises in non-heavily polluting industries, their lower reliance on the environment makes them more dependent on good corporate governance and transparency to build trust and maintain competitive advantage. Therefore, the role of ESG information disclosure in promoting corporate green innovation may be more significant for firms in non-heavily polluting industries.