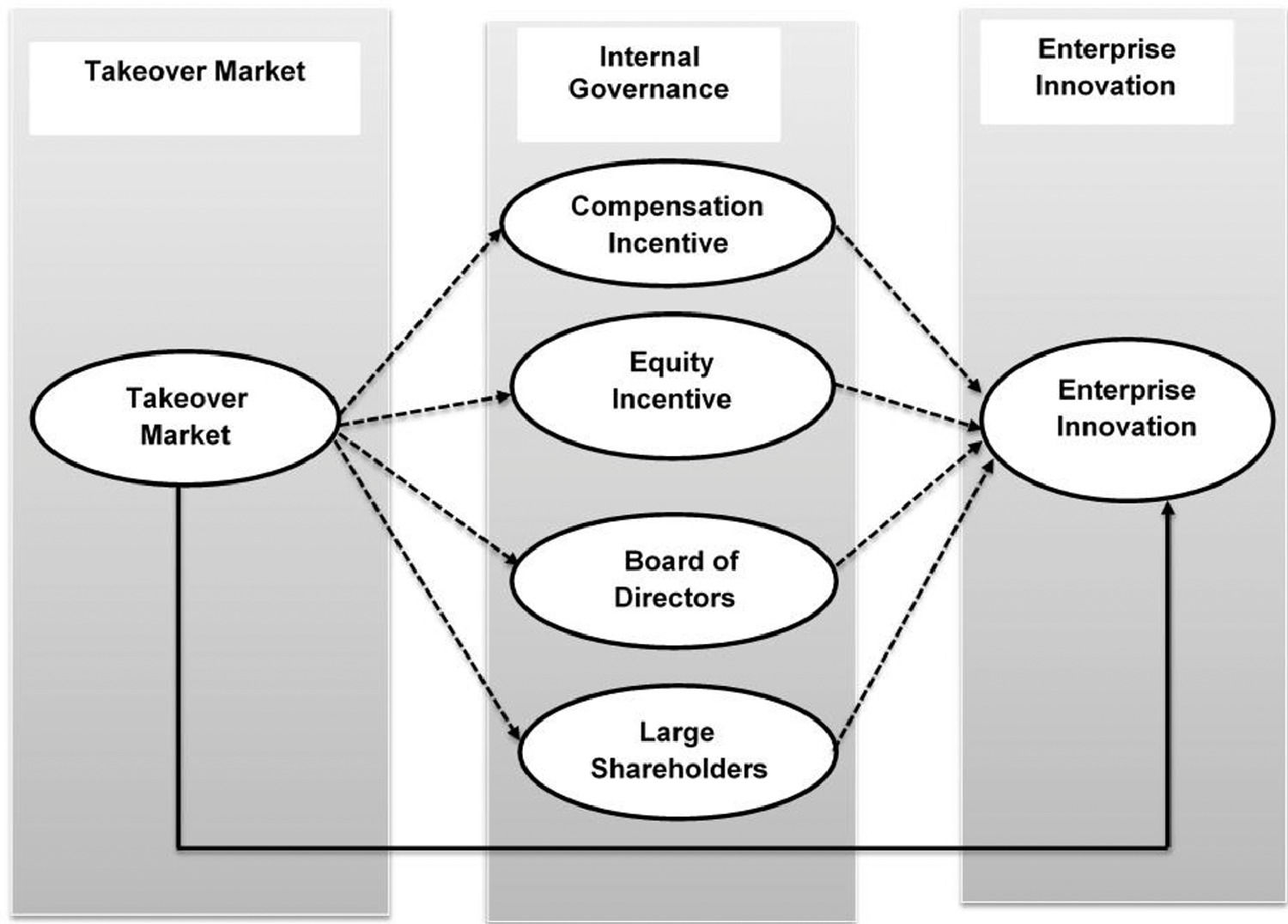

This study explores the relationship between the takeover market and enterprise innovation. We also investigate the mediating role of internal governance (managers’ compensation incentives, equity incentives, boards of directors, and large shareholders) on the relationship between the takeover market and enterprise innovation. We use comprehensive panel data of 1307 firms listed on the Shenzhen and Shanghai stock exchanges for 2006-2016 to meet the study's objectives. We find that the takeover market positively and significantly influences corporate innovation. It improves corporate innovation ability by increasing managers’ compensation incentives. However, enterprise innovation ability decreases with an increase in managers’ equity incentives, large shareholders, and the board of directors. Finally, this study recommends useful policy implications to increase enterprise innovation in the Chinese financial market.

Innovation is the driving force of economic development. As the main participant in social and economic innovation, enterprises contribute significantly to economic growth. As economic globalization and market competition increase, enterprises try to improve their market competitiveness through improvements in research and development (R&D) investment. Enterprise innovation is the key to economic structure promotion. Research on enterprise innovation driving factors is key to enterprise innovation development (Daksa et al., 2018).

Innovation activities present features of time and investment, as well as risk. Since ownership and management power are separated in most enterprises, innovation activities may be limited because of information asymmetry and interest inconsistency between owners and managers (Bendickson et al., 2016; Hoskisson et al., 2002). Therefore, research on the factors influencing enterprise innovation is essential. Corporate governance can encourage enterprise innovation in principal-agent problem alleviation and resource allocation optimization as a basic necessity in enterprise operations. Corporate governance includes internal and external governance (Chuntao & Min, 2010). First, Schumpeter (1950) proposed innovation theory, emphasizing the role of external governance. The takeover market is a key mechanism of external governance. It could alleviate conflicts of interest between shareholders and managers, reduce agency costs, improve corporate governance efficiency, and provide conditions for enterprise innovation activities through punishment and motivation functions (Munari et al., 2010; Sapra et al., 2014).

Takeover market theory is an important external governance mechanism. However, few studies focus on the interaction between the takeover market and internal governance. Therefore, this study discusses the interactive relationship between the takeover market and internal governance. The findings answer how corporate innovation can be improved through an internal governance mechanism. In addition, the mediating effect model explored the interactive relationship between takeover market and internal governance segmentation and the influence path on enterprise innovation. This is a new research study on influencing factors for enterprise R&D. This study makes meaningful contributions to future research theoretical studies and practice. First, it provides a new theoretical perspective for enterprise innovation and enterprise development based on internal and external governance. Second, the studies, such as the effectiveness and application of the internal governance structure and the takeover market mechanism, can improve the enterprise management level, promote the corporate governance structure, optimize enterprise resource configuration, eliminate conflicts of interest among different participants, diversify the risk of operators, and provide scientific and effective methods to improve performance appraisal systems. Third, the study introduces scientific solutions to help in enterprise innovation decision-making.

Many studies have attempted to identify the impact of corporate governance on enterprise innovation. However, some research directions on the relationship between corporate governance and enterprise innovation are still ignored. First, researchers do not focus on the relationship between the takeover market, internal governance, and enterprise innovation. Second, previous studies have not identified the four dimensions of internal governance: compensation incentives, equity incentives, boards of directors, and large shareholders. Third, this study is the first to investigate the intervening role of internal governance (compensation incentive, equity incentive, board of directors, and large shareholders) in the relationship between takeovers and enterprise innovation. Based on the above literature and discussion, we propose the following research questions (RQ):

RQ1: How does the takeover market influence enterprise innovation?

RQ2: What is the intervening role of internal governance (compensation incentive, equity incentive, board of directors, and large shareholders) in the takeover and enterprise innovation relationships?

The design of this study was as follows. Section 2 provides a review of the literature and hypotheses. Section 3 presents the research methodology. Section 4 presents and discusses the results. Finally, conclusions and policy recommendations are presented in Section 5.

Literature Review and HypothesisTakeover Market and Enterprise InnovationThe takeover market is an external governance mechanism that segregates ownership and management. Manne (1965) was the first to define this in his research on listed enterprises’ mergers and acquisitions. Fama and Jensen (1983) defined the takeover market as an enterprise's takeover market, a corporate control mechanism. This mechanism can supervise managers and alleviate agency conflicts (Fama & Jensen, 1983). Liao et al. (2014) demonstrated that the corporate takeover market is the market formed for purchasing equity or stock proxy, which takes control of enterprises.

The takeover market is the essence of external governance, affecting enterprise innovation by influencing an enterprise's internal governance. Research on control rights and internal corporate governance supports that internal corporate governance positively affects enterprise managers’ supervision and incentives and reduces agency costs (Holthausen & Larcker, 1996; Mian & Rosenfeld, 1993; Schumpeter, 1950). By contrast, other scholars believe that it may have negative effects. Xiaodong and Xiaoyue (2003) pointed out that it is not conducive to corporate governance mechanisms in enterprises with a high concentration of ownership since large shareholders have too strong power. Mei (2014) found that many enterprises’ investments are inefficient, fail, and fatal due to large shareholders' profit maximization behaviors. Ying and Wang (2013) illustrated that a change in control shareholders might bring better performance in equity transfer and asset divestiture but worse performance in equity transfers for non-control shareholders. There are three arguments in the takeover market and enterprise innovation research. First, some researchers believe that the takeover market positively correlates with enterprise innovation. Mergers and acquisitions result in market changes, and enterprises' innovation is affected by market mechanisms (Hitt et al., 1990). To maintain competitiveness, managers prefer to improve enterprise innovation; they will continuously enhance the enterprise's technical ability and gain competitive advantages (Tu & Wu, 2021). Belloc (2012) points out that the transfer mechanism of the takeover market is an important improvement, and social resources are distributed under the effect of the price mechanism, which is the most important external environmental factor that affects enterprise innovation. Second, some researchers have argued that the takeover market is negatively correlated with enterprise innovation. Dejardin (2011) found that when stakeholders believe that managers might change, rent-seeking behavior will appear, the former investment contracts will not be performed, and the enthusiasm for enterprise innovation will be discouraged. Long and Ravenscraft (1993) found that it decreases the motivation for enterprise innovation because of managers’ changes. Third, other researchers have found a nonlinear correlation between the takeover market and enterprise innovation. Long and Ravenscraft (1993) also found a “U-shaped” relationship between enterprise innovation and external takeover pressure. Although managers’ innovation activities may be encouraged by shareholders’ supervision, it is difficult to generate a strong driving force when the supervision intensity reaches a certain high level. This study finds that changes in dominant shareholders may improve an enterprise's operation; therefore, this study supports the opinion that the takeover market positively affects enterprise innovation. Based on the above literature and discussion, we propose the following hypotheses:

Hypothesis 1 Takeover market positively and significantly impacts enterprise innovation

Appropriate manager incentives could coordinate information asymmetry and conflict of interest due to the segregation of control power under a rational principal-agent relationship in enterprise innovation. Manager incentives could maintain the stability of enterprise management and stimulate their enthusiasm and creativity. Compensation, equity, promotion, and implicit incentives are the main activities adopted. However, it is difficult to determine the rational level of these encouraging behaviors. This study hypothesizes the mediation effect of internal governance on the relationship between the takeover market and enterprise innovation, and some previous studies support our hypotheses (Amore & Bennedsen, 2016; Cyert et al., 2002; Hoskisson et al., 2002). Prior studies highlight that internal governance has different names but generally falls within four categories: managers’ compensation incentives, managers’ equity incentives, boards of directors, and large shareholders (Samma et al., 2020). The literature below supports the mediating effect of internal governance on the relationship between the takeover market and enterprise innovation.

Manager's Compensation Incentive and Enterprise InnovationJenkinson and Mayer (1992) widely accept the external supervision of managers in the takeover market is widely accepted Jenkinson and Mayer (1992). Based on the principal-agent theory, different from managers who have the actual management power of the company, the owner of the company only has the nominal right of management (Berle & Means, 1991). Being owners, shareholders chase innovative projects with high returns and risks. At the same time, the agent (i.e., the managers) mainly considers the stability and reputation of their jobs and prefers to reduce enterprise innovation activities to reduce the private costs of non-routine management (Bertrand & Mullainathan, 2003). To address these problems, managers' compensation incentives implemented in enterprises are now accepted as the main incentive method. This is considered an effective way to solve information asymmetry and conflicts of interest between owners and managers. Many studies have been conducted on management compensation incentives, but the effect of managers’ compensation incentives remains a topic of discussion. There are currently two main opinions. First, managers’ compensation incentives are positively correlated with enterprise innovation. This point of view has been accepted by most researchers (Lu et al., 2020). Chen and Whalley (2014) analyzed the world's top 500 enterprises; these companies usually design and supervise the implementation of compensation plans by estimating compensation committees. The compensation committees can effectively reduce the managers’ “short-sighted” behaviors, and executive compensation increases the enterprise's investment in innovation. Canarella and Nourayi (2008) demonstrated that a reasonable compensation incentive could increase an enterprise's performance. Barros and Lazzarini (2012) state that both managers’ compensation and promotion incentives positively affect enterprise innovation. Similarly, Sarfraz et al. (2019) conclude that hierarchical CEO succession intensifies enterprise innovation. Barros and Lazzarini (2012) also find that enterprises can improve their innovation ability by providing targeted compensation incentives to senior managers. Hoskisson et al. (1993) studied the impact of senior manager incentives on a company's innovation capability. They find an obvious positive correlation between a manager's compensation incentive and enterprise innovation ability.

Chuntao and Min (2010) find that appropriate compensation incentives promote executives' innovation enthusiasm. Li et al. (2015) analyzed panel data of Chinese listed manufacturing enterprises from 2002 to 2013, and the results showed that an increase in executive compensation could persistently improve enterprise innovation. Shahzad et al. (2021) also obtained similar results. However, some researchers believe that there is no significant correlation between manager compensation incentives and enterprise innovation. Taussig and Barker (1925) pointed out that there is a low correlation between executive compensation and an enterprise's performance. Holmstrom and Costa (1986) pointed out that an increase in executive compensation incentives may lead to a shortage of enterprises’ innovation funds and reduce R&D investment. Lu et al. (2020) point out that compensation incentives have no significant correlation with an enterprise's R&D investment. Zahra and Neubaum (2000) and Zahra, Neubaum, et al. (2000) separately analyze traditional enterprises and high-tech enterprises and find that, compared with traditional enterprises, long-term compensation has a significant positive effect on R&D investment in high-tech enterprises. However, the relationship between short-term compensation and R&D investment was not significant. Lin et al. (2011) found that CEO compensation is independent of enterprises’ R&D innovation. Tang et al. (2011); (Xu, 2011) find an inverted "U"-shaped relationship between executive compensation incentives and R&D investment in China's state-owned enterprises. For non-state-owned companies, there is no correlation between executive compensation incentives and R&D investments. Hence, we propose the following hypothesis:

Hypothesis 2 Managers’ compensation incentives mediate the relationship between takeover market and enterprise innovation.

Innovation has many features such as strong professional requirements, high risk, time, and significant investment. Managers often hesitate or even reject enterprise innovation to achieve short-term benefits. However, shareholders aim to maintain continuous, long-term earnings. To effectively alleviate the principal-agent problem, researchers have focused on the impact of managers’ equity incentives on the level of enterprise innovation and enterprise performance (Wang et al., 2021). Previous scholars point out three views regarding managers’ equity incentives: First, managers’ equity incentives positively and significantly impact enterprise innovation. Barker III and Mueller (2002) show that the shareholding ratio of managers could reflect their attitude toward bearing operational risks, and the equity incentive could encourage managers to choose high-risk investments, which provides obvious evidence of the positive correlation between them. The managers who obtain the enterprise's equity may gain dividends; they are inclined to enterprise R&D at high risk, promoting enterprise innovations and achieving its business goals. Dong and Gou (2010) pointed out that equity incentives can stimulate enterprises' willingness to innovate. Artz et al. (2010) selected the number of patents owned by enterprises to indicate a company's R&D performance. TENG and HE (2010) (Xiaoyan & Yujing, 2014) show that executive equity incentives positively affect a company's innovation performance. A manager's equity incentive can promote a company's R&D and improve its performance (LIANG & ZHANG, 2005; Yang, 2007). Similar conclusions were drawn from 2012 to 2016 (Yan-ni, 2011; Yin & Sheng, 2019). Zhang and Zhao (2014) point out that managers’ equity incentives in non-state-owned enterprises have a stronger impact on enterprise innovation than in state-owned enterprises. Second, managers’ equity incentives negatively correlate with enterprise innovation. Bens et al. (2002) believe that after senior executives receive stock compensation, they are more likely to pursue higher short-term performance to obtain larger stock income, leading managers to decrease innovation investment.

Similarly, a manager's equity incentives do not correlate with enterprise innovation. Tien and Chen (2012) analyzed high-tech Chinese firms and concluded that neither long-term equity incentives nor short-term salary incentives could improve innovation. Managers’ preferences are essential factors in R&D investment decision-making, which equity incentives cannot affect. Han and Tang (2019) chose listed manufacturing enterprises as a sample. The results showed that equity incentives have weak positive effects on enterprises’ performance, while the shares compensated by managers have a weak correlation with company innovation. Guozhong and Xue (2019) point out that equity incentives are ineffective in increasing a company's R&D investment because of loss avoidance. Third, a non-linear correlation exists between equity incentives and enterprise innovation. Feng et al. (2007) found an inverted U-shaped relationship between managers’ incentives and innovation input. The number of shares held is a threshold value; when it is less than this value, a positive correlation will be observed, while a negative correlation will be found if the number of shares held is greater than the threshold value. Xu and XU (2012) found that takeover market incentives positively influence dynamic technological innovation capability when the takeover market incentive is less than a critical value. There is a significant inverted U-shaped relationship between takeover market incentives and takeover market incentive innovation performance. Hoskisson et al. (1993) point out an inverted U-shaped relationship between equity incentives and enterprise innovation. Zhao et al. (2018) found a significant inverted U-shaped relationship between the shareholding ratio of senior executives and enterprises’ R&D efficiency. Scholars find that granting some equity to executives could prevent them from pursuing short-term interests and alleviate the conflict between owners and executives, encouraging managers to continuously invest in enterprise innovation (Zahra, Ireland, et al., 2000). Therefore, we propose the following hypotheses:

Hypothesis 3 Equity incentives mediate the relationship between the takeover market and enterprise innovation.

As the decision-maker, the board represents shareholders’ benefits. Scholars have mainly studied the relationship between board governance and enterprise innovation through board size, structure, power concentration level, number of meetings, and ownership concentration. Bhagat and Black (1999) point out that small-sized director boards perform better in terms of reaction speed under dangerous circumstances. However, Zahra, Neubaum, et al. (2000) analyzed 239 medium-sized American manufacturing companies from 1991 to 1997; the results show that the size of the board and enterprise innovation ability represent an inverted U-shaped relationship. Yermack (1996) found that independent directors may bring innovative suggestions and that an appropriate proportion of independent directors will be helpful for enterprise innovation. Xue and Guozhong (2019) studied Chinese listed companies and pointed out that the level of enterprise technological innovation is improving. However, Yang (2007) failed to find a significant relationship between board size and enterprise innovation.

Similarly, based on contingency theory, Zona et al. (2013) find that the proportion of independent directors has no direct effect on enterprise innovation. Some researchers have found that the education level of the board of directors has a positive correlation with enterprise innovation (Chen & Whalley, 2014; Wincent et al., 2010; Zhu, 2020). David and Foray (2001) studied 73 American enterprises from 1987 to 1993 and found that board structure does not significantly affect enterprise R&D input and output. Guozhong and Xue (2019) pointed out a positive correlation between independent directors and enterprise innovation. Enterprises with a high proportion of independent directors invest significantly more in innovation than those with a low proportion of independent directors. Zhao and Wen (2011) pointed out that enterprise innovation levels increase with the proportion of independent directors. However, Zahra, Neubaum, et al. (2000) found that the greater the proportion of outside directors, the lower the enterprise's R&D innovation enthusiasm. Previous studies also discussed the effect of the board of directors on enterprise innovation (Rejeb et al., 2019). Mallette and Fowler (1992) point out that the combination of chairperson and general manager positions has a significant and positive correlation with enterprise innovation. Mallette and Fowler (1992) also point out that the combination of chairman and general manager positions promotes more flexible enterprise innovation decision making. FENG and Wen (2008) point out that combining the chairman and general manager positions would avoid conflicts and ensure the consistency of enterprise innovation decisions. Zhao and Wen (2011) analyzed the relationship between the power structure of board directors and enterprise innovation ability. The results show that the separation of the chairman and general manager positions is conducive to increasing the enterprise's R&D investment. However, Wu et al. (2007) find that the separation of chairman and general manager positions has no significant effect on an enterprise's technological innovation. Prior studies have also discussed the relationship between ownership structure and enterprise innovation (Baysinger et al., 1991). Parrino et al. (2005) find that large shareholders intend to share more benefits gained from an enterprise's technological innovation and are more willing to increase their investment through their control rights. Some researchers have shown that a chairman's shareholding ratio positively affects enterprise innovation (LI & LIU, 2012; XU & YIN, 2011). From the perspective of the shareholding ratio of board directors, Zhao and Wen (2011) point out that it is conducive to improving enterprise innovation. Lu and Dang (2014) analyze the panel data of 1,344 enterprises on the main boards of the Shanghai and Shenzhen Stock Exchanges from 2006 to 2010. Their research showed that an enterprise's R&D investment increases with an increase in the shareholding ratio of directors and supervisors. This study also discusses how board meetings affect enterprise innovation. Some researchers have found that the number of board meetings can enhance enterprise innovation ability. Qi and Dongzhi (2001) believe that board directors’ decisions and behaviors are reflected in board meetings. Directors supervise enterprise managers through board meetings, which is conducive to the implementation of innovative decisions. However, Mallette and Fowler (1992) show that if board directors represent shareholders of state-owned shares, enterprise innovation activities may be reduced because of innovation risks. Therefore, we propose the following hypotheses:

Hypothesis 4 Board of directors mediates between takeover market and enterprise innovation

Dyck and Zingales (2004) showed that an enterprise's major shareholder governance affects incentives and entrenchment. The incentive effect is that major shareholders can supervise managers, which would improve the company's value and increase profits. The entrenchment effect is that large shareholders “occupy” the benefits of minority shareholders by using their controlling power to maximize their interests. This study categorizes large shareholders into three dimensions (to measure enterprise innovation). First, there is a positive relationship between the governance of large shareholders and enterprise innovation. For example, Jacobs (1979) analyzed high-tech enterprises and found that concentration of ownership positively affects a company's innovation input. Shleifer and Vishny (1997) indicate that a few major shareholders control a company's equity. Large shareholders actively supervise managers and promote innovation to obtain long-term benefits. Lee and O'neill (2003) found that when the concentration of a company's ownership is low, increasing the shareholding ratio of larger shareholders could encourage small shareholders to supervise managers and prevent managers from reducing innovation input for short-term interests (Rasool et al., 2019). An increase in the shareholding ratio of larger shareholders improves enterprise innovation. In addition, Hosono, Hosono, et al. (2004) analyzed the panel data of Japanese manufacturing enterprises from 1987 to 1998. Empirical results show that the shareholding ratio of major shareholders is positively correlated with corporate R&D. LIU et al. (2005) find that the higher the shareholding ratio of large shareholders, the more managers would pay attention to a company's long-term goals and promote enterprise innovation. Second, it investigates the negative relationship between large shareholder governance and enterprise innovation. Yafeh and Yosha (2003) conducted an empirical analysis. They pointed out that when ownership concentration is high, large shareholders can embezzle the benefits of minority shareholders. However, the enterprise's controlling authority, i.e., the “entrenchment defense effect,” is significant; the gradually concentrated ownership will hinder the enterprise's innovation investment. Haiyun (2015) analyzed panel data from manufacturing companies of listed A-shares and found that if the ownership of the company is relatively concentrated, the major shareholders may infringe on the R&D funds to maximize their own short-term interests, leading to low R&D utilization efficiency. Third, we examine the non-linear relationship between large shareholders’ governance and enterprise innovation. Wen (2008) used the empirical analysis and showed an “N-shaped” relationship between the ownership concentration of large shareholders and enterprise innovation. Both Yang (2011) and TENG and HE (2010) show a significant inverted U-shaped relationship between ownership concentration and technological innovation; only some ownership concentration values can promote managers to actively carry out innovation activities. Therefore, we propose the following hypotheses:

Hypothesis 5 Large shareholders mediate the relationship between takeover market and enterprise innovation

Considering the impact of China's reform of non-tradable shares in 2005 on the capital market and the availability of research data, this study selects panel data of A-share listed industrial companies in Shenzhen and Shanghai stock exchanges from 2006 to 2016. In particular, the following data were excluded from the initial sample. First, ST and *ST listed firms with abnormal financial status1since their financial conditions or other conditions are unnormal. Second, listed financial firms have financial accounting that is significantly different from industrial firms. Third, the samples had incomplete or extreme values. The final sample consists of 1307 firm-year observations 6501. The data source was the China Tai’ an database.

VariablesEnterprise innovation capability is expressed by FMZL. According to Iqbal et al. (2020), the number of invention patents can be used to measure the output innovation capability of listed enterprises. The independent variable was the market mechanism of corporate control (KZQSC). According to the method provided by Yao (2010), considering that the industry is a prerequisite for driving M&A, the M&A activity of listed companies in the industry is measured. The mediating variable was the management incentive mechanism (GLZJL). The management compensation incentive (XCJL) is measured by the natural logarithm of managers’ total annual monetary compensation. Management equity incentive (GQJL) is measured by the shareholding ratio of management at the end of the year. Suppose that the chairperson and general manager are the same people. In that case, it could weaken its governance effect; the proportion of independent directors reflects the characteristics and intelligence structure of the board; the responsibility fulfillment situation of the board directors could be reflected by the times of the meeting; the larger the board size, the more conducive it is to improve the efficiency of management. Therefore, board governance (DSHZL) is explained by the integrated position of the chairman and general manager, the proportion of independent directors, meeting frequency, and the scale of the board directors. The detailed calculation process is as follows: First, the variables are logically valued. If the proportion of independent directors is higher than the average industry value, the value is 1; otherwise, it is 0. If there is another post situation, the value is 0; otherwise, it is 1. If the number of board meetings is higher than the average industry value, the value is 1; otherwise, it is 0. If the size of the directors is larger than the average industry value, the value is written as 1; otherwise, the value is written as 0. Second, we add the logical values of the board governance index. Third, a linear regression analysis was carried out. We take the logical value of corporate board governance as the dependent variable and the other variables as independent variables. Then, a regression model was adopted, and the regression coefficients of each variable were estimated. Finally, the board governance index is calculated based on the results of the regression model. The larger the board governance index, the more effective the corporate board governance mechanism—large shareholders governance mechanism (DGDZL). The motivation of large shareholders to supervise managers is closely related to the proportion of their shares. The higher the proportion of shares held by large shareholders, the more motivated they are to supervise their managers. This study measures the governance of large shareholders based on the degree of ownership concentration of the largest shareholders.

There are five control variables. According to Ke-qin (2010), the growth rate of total assets (Growth), operational years of the company (Firmage), profitability (ROA), free cash flow (FCF), and CEO's management experience (CEOAGE) were taken as control variables. In particular, the growth rate of total assets = (total assets at the beginning of year–total assets at the end of year)/ total assets at the beginning of the year, and the operation years of the company are the period from the beginning of the company establishment to the time of sample selection. Net interest rate of total assets = net interest / total assets at the end of the year. The independent director's proportion is the number of independent directors/board directors. Free cash flow = (profits before interest and tax + depreciation and amortization–capital expenditures – increase in operation capital)/ total assets at the end of the year. CEO management experience is explained by the natural logarithm of CEOs’ ages. Equity distribution = the top five shareholders' shareholding/large shareholders’ stakes. Simultaneously, annual and industry factors were controlled. Year and industry effects were explained using dummy variables 0 and 1.

ModelsAccording to the mediating effect test method from Wen and Ye (2014), "takeover market → manager incentive → enterprise innovation", the models are constructed as follows:

another two mediating effect models are similar as follows“Takeover market → board governance → enterprise innovation” and "takeover market → major shareholder governance → enterprise innovation".Results and discussionDescriptive analysis

Table 1 presents the descriptive statistics for the main variables. The maximum value of FMZL is 8.6635, the minimum value is 0, and the standard deviation is 1.2888, all of which indicate large differences in enterprise innovation among listed companies. The mean value of FMZL is 1.8217, and the median value is 1.6094, which indicates that the listed companies’ innovation level is low. The maximum value of KZQSC is 7.0296, the minimum value is 0, the mean value is 5.1722, and the standard deviation is 1.0266, indicating that the market difference in control rights among listed companies is great and the development is unbalanced. The maximum value of DSHZL was 5.3259, the minimum value was 0.2456, the mean value was 2.0394, and the standard deviation was 0.6193, indicating that the governance level and effectiveness of the board of directors are significantly different. The maximum, minimum, and mean values of DGDZL are 0.8999, 0.0029, and 0.3589, respectively, indicating that the governance of large shareholders is relatively significant. However, the degrees of ownership concentration are significantly different. The maximum value of GQJL is 0.8092, the minimum value is 0, and the standard deviation is 0.1363, indicating that management equity incentives are rarely applied and the differences are small. The maximum value of xCJL is 17.7348, the minimum value is 11.0021, and the standard deviation is 0.8224, indicating that compared with the equity incentive, the management compensation incentive is applied more, and the differences are relatively great.

Descriptive statistics.

Note: SD, Standard deviation; N, Sample size.

Table 2 shows Pearson's correlation analysis of the two major variables. The correlation coefficient between FMZL and KZQSC was 0.126, indicating that the takeover market positively affects enterprise innovation. The correlation coefficient between FMZL and GQJL is -0.029, indicating that managers' equity incentives restrain enterprise innovation. The correlation coefficient between FMZL and xCJL is 0.341, indicating that managers' compensation incentives inspire enterprise innovation. The correlation coefficient between FMZL and DSHZL is 0.107, indicating that board governance improves an enterprise's innovation ability. The correlation coefficient between FMZL and DGDZL is 0.060, which indicates that the improvement in large shareholders’ governance promotes enterprise innovation ability. The correlation coefficients among the variables were less than 0.8, indicating that collinearity was less likely to occur in the model test.

Pearson correlation analysis.

Table 3 shows the results of the empirical analysis of the influence of the takeover market mechanism on enterprise innovation through managers’ equity incentives. In Table 2, the test path is "KZQSC → FMZL", the regression coefficient of KZQSC is 0.1168, and the T value is 6.39, which is significant at the 1% level, which indicates that the takeover market is significantly and positively correlated with the enterprises’ innovation ability. In other words, the takeover market promotes enterprise innovation positively. Thus, Hypothesis 1 is verified. According to the test path "KZQSC → GQJZ", the regression coefficient of KZQSC is 0.0088, and the T value is 4.68, indicating that the takeover market is significantly positively correlated with the managers' equity incentive, i.e., the takeover market improves the managers' equity incentive level. According to the test path "KZQSC → GQJZ → FMZL,” the regression coefficient of KZQSC was 0.1224, the T value was 6.70, and the regression coefficient of GQJL was -0.6456, and the T value was -5.33, all of which were significant at the 1% level. The results indicate that managers’ equity incentives are negatively correlated with enterprise innovation. Based on the mediating effect, managers’ equity incentives inhibit the positive effect of the takeover market on enterprises’ innovation; that is, the takeover market can inhibit enterprise innovation by improving managers’ equity incentives.

Takeover market, Manager Equity incentive and Enterprise Innovation.

Note: *** means significant at 1% level, ** means significant at 5% level, and * means significant at 10% level.

Because managers’ equity incentives are improved by the takeover market, they are not widely used in China, and the high risk of enterprise innovation will reduce the effect of managers’ equity incentives, managers’ innovation enthusiasm is affected, and enterprise innovation ability is reduced. Thus, Hypothesis 2 is not verified.

Takeover market, executive compensation incentive, and enterprise innovationTable 4 shows the results of the empirical analysis of the takeover market's influence on enterprise innovation through managers' compensation incentives. In Table 4, the test path is "KZQSC → FMZL", the regression coefficient of KZQSC is 0.1168, and the T value is 6.39, which is significant at the 1% level, which indicates that the takeover market is significantly and positively correlated with the enterprises’ innovation ability, i.e., takeover market promotes the enterprise innovation. Thus, Hypothesis 1 is verified. According to the test path "KZQSC → XCJL", the regression coefficient of KZQSC is 0.039, and the T value is 3.60, which is significant at the 1% level. They indicate that the takeover market is significantly and positively correlated with the manager compensation incentive, i.e., the takeover market improves the managers’ compensation incentive. According to the test path "KZQSC → XCJL → FMZL", the regression coefficient of KZQSC is 0.0963, the T value is 5.53, the regression coefficient of XCJL is 0.5260, and the T value is 26.38, all of which are significant at the 1% level, they indicate that the manager compensation incentive is positively correlated with enterprise innovation. The manager compensation incentive, which has a mediating effect, further improves the takeover market's influence on enterprise innovation. In other words, the takeover market promotes enterprise innovation by increasing the compensation incentives of managers. Thus, Hypothesis 2 is verified.

Takeover market, manager's compensation incentive and enterprise innovation.

Note: *** means significant at 1% level, ** means significant at 5% level, and * means significant at 10% level.

Table 5 shows the results of the empirical analysis of the takeover market's influence on corporate innovation through board governance. In Table 4, the test path is "KZQSC → FMZL", the regression coefficient of KZQSC is 0.1168, and the T value is 6.39, which indicates that the takeover market is significantly and positively correlated with the enterprises' innovation ability, i.e., the takeover market promotes the enterprises’ innovation. Thus, Hypothesis 1 is verified. The test path is "KZQSC → DSHZL", the regression coefficient of KZQSC is -0.0347, and the T value is -3.98, which indicates that the takeover market is significantly negatively correlated with the board governance, i.e., the takeover market inhibits the level of board governance. About the test path, i.e., "KZQSC → DSHZL → FMZL", the regression coefficient of KZQSC is 0.1262, the T value is 6.95, the regression coefficient of DSHZL is 0.2726, and the T value is 10.51, all of which were significant at the 1% level. This shows that board governance is positively correlated with enterprises’ innovation abilities. However, the effect of board directors’ governance on the takeover market will decline, and board directors’ governance will harm enterprises’ innovation. In other words, the takeover market reduces enterprise innovation by reducing board governance. The board of directors has the right to decide the enterprise's strategy, and the improvement of its governance level will promote the implementation of the enterprise's innovation. However, with the enterprise's transfer, the change in board directors will decline governance level, development strategy will also change, and the resources for enterprise innovation will require reconfiguration, which will decline enterprise innovation ability. Therefore, Hypothesis 3 was verified.

Takeover market, board governance and enterprise innovation.

Note: *** means significant at 1% level, ** means significant at 5% level, and * means significant at 10% level.

Table 6 shows the results of the empirical analysis of the takeover market's influence on enterprise innovation through shareholder governance. In Table 5, the test path is "KZQSC → FMZL", the regression coefficient of KZQSC is 0.1168, and the T value is 6.39, which are significant at the 1% level, they indicate that the takeover market is significantly and positively correlated with the enterprises’ innovation, i.e., takeover market promotes enterprise innovation. Thus, Hypothesis 1 is verified. About the test path "KZQSC → DGDZL", the regression coefficient of KZQSC is -0.0242, and the T value is -11.63. They indicate that the takeover market is significant and negatively correlated with the governance of large shareholders; that is, the takeover market inhibits the governance level of large shareholders. About the test path "KZQSC → DGDZL → FMZL", the regression coefficient of KZQSC is 0.1329, and the T value is 7.21. The regression coefficient of DGDZL is 0.6659, and the T-value is 6.11; all of them are significant at the 1% level. They show that the governance level of large shareholders is positively correlated with enterprise innovation; the governance level of large shareholders is reduced with the effect of the takeover market; thus, enterprise innovation is reduced. In other words, the takeover market reduces enterprise innovation by reducing the governance of large shareholders. Large shareholders have decision-making rights, and improving their governance level could promote enterprise innovation. However, the takeover market causes market pressure and a change in ownership structure, which reduces the governance level of large shareholders and enterprise innovation. Therefore, Hypothesis 4 was not verified.

Takeover market, major shareholder governance and enterprise innovation.

Note: *** means significant at 1% level, ** means significant at 5% level, and * means significant at 10% level.

To verify the robustness of the above regression results, fixed effects estimates were used to re-regress the original model. The robustness results in Table 7 show that takeover market power still positively correlates with enterprise innovation, and they are significantly and positively correlated at the 1% level. The takeover market and managers’ incentives were positively correlated at the 1% level. However, the mediating effect of equity incentives on the relationship between takeovers and enterprise innovation has not been verified. The takeover market and manager's compensation incentive are significantly and positively correlated at the 1% level. Managers’ compensation incentives significantly affect the relationship between the takeover market and enterprise innovation. Considering the manager's compensation incentive, the regression coefficient between the takeover market and enterprise innovation is 0.096, which is the regression coefficient, i.e., 0.117. Therefore, the manager's compensation incentive has a mediating effect on the relationship between takeover and enterprise innovation. The takeover market is significantly negatively correlated with board governance, and the mediating effect of board governance on the relationship between takeover and enterprise innovation is not significant. Finally, the takeover market is negatively correlated with major shareholder governance, and the mediating effect of major shareholder governance on the relationship between the takeover market and enterprise innovation has not yet been verified. In summary, in addition to the difference in regression coefficients, all the results are consistent with the above regression results, which proves the robustness of the results above.

Results of FE estimates.

Note:t statistics in parentheses, * p < 0.1, ⁎⁎p < 0.05, ⁎⁎⁎p < 0.01

To test the endogeneity of the model, following Fareed et al. (2022a) and Shahzad et al. (2022), we checked the robustness of the model using the two-stage least squares (2SLS) method with one lag of the independent variable. The robustness checks in Table 8 show that the independent and dependent variables are still significantly and positively correlated.

Robustness of 2SLS estimates.

Note: t statistics in parentheses, * p < 0.1, ** p < 0.05, *** p < 0.01.

The natural logarithm of R&D investment is replaced by the explained variable, enterprise innovation. The fixed effects method was used to perform a regression of the model again. The results in Table 9 show that replacing the variables is consistent with the results of the above regression and fixed effects regression, proving that the results are robust.

Results of Variable Substitution.

Note: t statistics in parentheses, * p < 0.1, ** p < 0.05, *** p < 0.01.

This study explores the relationship between the takeover market and enterprise innovation. We also investigate internal governance (managers’ compensation incentives, managers’ equity incentives, boards of directors, and large shareholders) as a mediating variable between the takeover and enterprise innovation relationship. Furthermore, we analyzed China's A-share listed industrial companies in Shenzhen and Shanghai from 2006 to 2016. First, combining current theory and reality, the significance of enterprise innovation and the influence of enterprise governance on enterprises’ innovation is discussed. Second, we analyzed the influence of the takeover market, managers’ incentives, board governance, and large shareholders’ governance on enterprise innovation. Finally, the mediating effect model, descriptive statistics, and Pearson's correlation were applied to test the influence of the takeover market and internal enterprise governance on enterprise innovation. The conclusions are as follows:

First, the takeover market has a significantly positive effect on enterprise innovation. Under the circumstances of an enterprise principle-agent structure, the development of the takeover market is capable of promoting the optimization of enterprise innovation resource allocation and stimulating enterprises’ innovation. It is also proven that the takeover market has accomplished its duty to promote enterprises' innovation in China. The takeover market improves enterprise innovation by increasing managers' compensation incentives but reduces enterprise innovation by increasing managers' equity incentives. Generally, the takeover market positively affects managers’ incentives, but the influences of different managers’ incentives on enterprise innovation are different. Currently, compensation incentives are popular among Chinese enterprises. An increase in manager compensation can stabilize these managers, stimulate their enthusiasm, and improve enterprise innovation. However, equity incentives reduce enterprise innovation because managers want to maximize their benefits. Therefore, to improve enterprise innovation, it is important to choose a reasonable incentive according to the market and policy environment.

Second, the takeover market reduces enterprise innovation by reducing board governance. The takeover market is negatively correlated with the board's governance level. The structure and size of the board of directors are altered because of takeover market affection, which may lead to a decline in the enterprise governance level, and enterprise innovation strategy may be harmed.

Third, the takeover market can reduce enterprise innovation by reducing the governance level of large shareholders. Large shareholders support enterprise innovation activities to maximize profit. However, the takeover market affects enterprise ownership structures, which partially restricts large shareholders' governance levels. Owing to the pressure of the takeover market, large shareholders might reduce their support for high-risk and long-periodicity enterprise innovation. Finally, this reduces enterprise innovation activities.

Policy RecommendationsAs an effective external governance mechanism, the takeover market is positive in terms of resource allocation and enterprise innovation, but ownership structure and relative registration restrict its development. Therefore, it is necessary to perfect the legal environment, improve the stock market, and release the vitality of the takeover market.

The level of manager incentives will directly impact enterprise managers, and enterprise operations and development will also be affected. Therefore, enterprises should focus on optimizing the internal governance structure, diversifying incentive methods, improving the supervision mechanism, and selecting the most effective manager incentive method. This will improve the governance level of managers and promote enterprise innovation.

Efficient board governance is conducive to decision-making in enterprise innovation and development. Enterprises should focus on the comprehensive quality of board members and improve the board's decision-making ability. The level of internal governance can be improved by optimizing the control environment and allocating management authority. This can create rational conditions for enterprise innovation and development.

The principle, which is based on strong property rights, affects the corporate governance structure. Ownership concentration can partially reflect an enterprise's internal governance level. The level of large shareholder governance can be increased by optimizing the equity structure and strengthening the supervision of large shareholders. Then, the optimal configuration of the enterprise's resources and governance can be improved. Finally, enterprise innovation is also promoted. Future studies could use researchers involved in R&D activities as a more reliable proxy for enterprise innovation (Fareed et al., 2022b).

DeclarationsCompeting interests: The authors declare that they have no competing interests.

Authors’ contributions: All authors equally contributed to this study.

Funding: This research work is supported by the National Social Science Fund of China (No. 20BGL070), the research project of Philosophy and Social Sciences of Hubei Provincial Department of Education (No.20Q136), and R&D project DATA4LOWDENSity COLab, FCT - Fundação para a Ciência e a Tecnologia, Portugal (UIDP/04011/2020).Attachment.

ST is abbreviation of “special treatment”. A listed company's stock number with ST means that this company which listed in China stock market is in financial trouble or other abnormal conditions now. On April 22, 1998, the Shanghai and Shenzhen Stock Exchanges announced that they would mark special treatment to the stock transactions of listed companies with abnormal financial trouble or other conditions. Such as their stock prices are limited to 5% increase and 5% decrease per day. Moreover, the *ST means that the listed company keep suffering losses in last three years, an early warning of delisting is given. price of the company with*ST is also limited to 5% increase and 5% decrease per day.