The credit union's main functions are the provision of individual financial loans based on collective savings, reaching up to provide full banking services, with expansion of its social function. Cooperatives are an alternative to supply a credit demand in the market, because a third of the municipalities have no bank branches. Although the participation of cooperatives in credit operations is still small compared to the Brazilian national banking system, its continued growth demonstrates the importance of this sector. In this sense, the analysis of the performance of these cooperatives becomes relevant to the extent that incentives to industry expansion differ from other financial institutions. In this context, this study aimed to analyze which the financial and economic performance of Brazil's largest credit unions. This performance analysis was performed using the indicators proposed by the CAMEL model, then the data envelopment analysis (DEA). It can be seen that there is a positive relationship between the use of variables in the model and the measurement of financial performance of credit unions. Moreover, according to the results, it can be observed that Uniprime Northern Paraná, Sicoob Cocred and Sicredi North RS/SC were cooperatives that stood out as efficient.

Las principales funciones de las cooperativas de ahorro y crédito son la provisión de préstamos financieros individuales basados en ahorros colectivos que permiten la prestación de servicios bancarios completos, ampliando su función social. Las cooperativas son una alternativa para abastecer una demanda de crédito en el mercado, ya que un tercio de los municipios no tienen sucursales bancarias. Aunque la participación de las cooperativas en las operaciones de crédito sigue siendo pequeña en comparación con el sistema bancario nacional brasileño, su continuo crecimiento demuestra la importancia de este sector. En este sentido, el análisis del desempeño de estas cooperativas se hace relevante en la medida en que los incentivos a la expansión de la industria difieren de otras instituciones financieras. En este contexto, este estudio tuvo como objetivo analizar cuál es el desempeño financiero y económico de las cooperativas de crédito más grandes de Brasil. Este análisis de desempeño se realizó utilizando los indicadores propuestos por el modelo CAMEL y luego el análisis de envoltura de datos (DEA). Se puede observar que existe una relación positiva entre el uso de variables en el modelo y la medición del desempeño financiero de las cooperativas de ahorro y crédito. Además, según los resultados, se puede observar que Uniprime Norte de Paraná, Sicoob Cocred y Sicredi North RS/SC fueron cooperativas que destacaron por su eficiencia.

As Bressan, Braga, and Bressan (2003) attest, credit cooperatives’ main goal is to grant individuals financial loans based on collective savings, providing them with full banking services and expanding their own social mission. The cooperatives are an alternative to meeting the demand for credit in the market, due to a third of Brazilian municipalities with no bank branches.

Ferreira, Gonçalves, and Braga (2007) assert that, although the participation of cooperatives in the operations is still small compared to the Brazilian national banking system, their consistent growth demonstrates the importance of the sector. Accordingly, the analysis of the performance of the cooperatives becomes relevant, insofar as incentives for expanding the sector differ from other financial institutions.

Vilela, Nagano, and Merlo (2007) argue that credit cooperatives are effective in both credit democratization and income redistribution. They allow segments of the society to organize the search for solutions to problems of access to credit and banking services, autonomously and independently. In addition, the authors point out that this business sector is expanding and so does the demand for managerial information enabling greater monitoring and control within these organizations.

Thus, taking into account the competitive environment in which the Brazilian banking system is inserted, credit cooperatives seek to operate effectively. They aim not only at maximizing their results or at reducing costs, but also at augmenting the economy of scale (Da Silva Filho, 2002). According to Bressan et al. (2011), in recent years the insolvency of financial institutions has concerned not only shareholders, but also governments, companies and individuals, who apply their financial resources and trust in these institutions.

In this context, considering the social and economic importance of the sector, grows the need for evaluating the financial and economic performance of the credit cooperatives. Thus, stands out the research question guiding this study: what is the economic and financial performance of the largest credit cooperatives in Brazil? The objective of the research is, then, to evaluate the economic and financial performance of the largest Brazilian credit cooperatives.

The study is justified by the importance of the cooperatives in society, both in social and economic terms. Barroso (2009) asserts that the study on credit cooperatives is relevant for their importance in the regional development, and for the need to clarify the dynamics of these organizations. These aspects contribute to the managerial solutions contributing the development of the sector.

Guerra Junior and Silva (2013) ensure that the cooperative business has caught the interest of many researchers due to its specific type of organization. They include concerns with maintaining practices of democratic decisions and joint efforts. The attention focuses on the need to combine business results with social expectations related to a series of facts: unemployment or underemployment, employment and income creation, and regional sustainable development.

The period under analysis has included 5 years, from 2008 to 2012, due to the availability of information supporting the study. A longer period would certainly reduce to a greater extent the size of the sample, which would undermine the analysis of the data. Several studies on financial and economic performance and capital structure, among which those by Roque and Cortez (2006), Costa and Garcias (2009), and Nakamura et al. (2007), have used the 5-year period for their analysis. They have proven to be efficient for the analysis. Assaf Neto (2010) stresses the importance of an analysis with temporal comparison, as this ensures monitoring the development of indicators. The occurrence is usually three to five years.

This paper is divided into four sections. After the introduction, presented herein, it approaches the theoretical foundations that have supported the analysis of the results. Then, are defined the methodological aspects delineating the study's research techniques. In the following section, the results are presented. Finally, are introduced the final considerations about the financial and economic performance of Brazil's largest credit cooperatives.

Theoretical frameworkCooperatives in economic contextDel Arco (1973) clarifies that the first agricultural unions appeared in the 1900s. They have proliferated throughout the interior of Spain as a result of an intelligent action of the Catholic social movement, and have reached its peak in the 1910s and 1920s, with more than five thousand Catholic Agricultural Unions. This fact has made its founders to create an essential instrument of credit in order to finance their activities through economic cooperatives.

The rapid rise in the prices in the early years after the Second World War greatly increased the need for working capital in retail, so that they managed to keep the same physical volume of business. This fact resulted in the difficulty the retail stores – in special, the small and midsized ones – had to confront in order to raise the necessary funds to maintain their activities. They had problems to invest their own capital. Therefore they acquired the resources, primarily through short-term bank loans, and sought relatively little capital in the long-term-capital markets (Dauten, 1960).

Smith (1984) explains that the cooperatives’ main function is to provide financial services to society. Some of these services involve savings deposits and credit access. These services should be offered at prices at least as attractive as compared to those offered by other institutions. The author adds that for the recognition of a credit cooperative as a nonprofit institution oriented to services in competition with other financial institutions, it would be incongruous to shape them to make profit or to maximize the return on equity. Therefore, minimizing costs is considered to be its appropriate goal.

Goddard, McKillop, and Wilson (2002) believe that credit cooperatives worldwide have demonstrated the effectiveness of the cooperative principles in the management of the financial affairs of millions of people. Having equal voting rights the associate-members participate, regardless the size of their deposits. Their main strength lies in the appeal of this philosophy. The authors add, however, that the relaxation of the requirements of certain liabilities inevitably has brought closer competition with other financial institutions, especially the retail banks. The banks usually complain of the current tax exemptions providing the credit cooperatives with an unfair advantage.

Credit cooperatives are financial institutions making the associates’ access to credit easier and cheaper. They reduce bank interests, especially overdraft fees and loans. However, regarding financial services, they differ from other financial institutions by their goals, and the public they want to achieve (Ferreira, Gonçalves, & Braga, 2007).

Sales (2010) ensures that the basis of the existence of a cooperative is the conjunction of individuals joining in a cooperative manner, who have common purposes and interests. In the current technological context – the knowledge era and cooperative ventures – the cooperatives must show economic results, providing themselves with effective sustainable social function, and avoiding bankruptcy in this very competitive market. The author adds that with the globalization of the economic activities, regardless of the field in which a company operates, it must present a high level of administrative efficiency leading to its goals’ achievement. The cooperatives are at a competitive disadvantage because of their characteristics of governance, democratic principles, and lack of professional qualification.

Guerra Junior and Silva (2013) espouse the impression that the cooperative business is fundamental to society. That is, it is fundamental to the extent that it promotes the use of private resources and assumes those risks on behalf of the community, in which it develops, and in favor of local sustainable development as well. The emphasis lies in the formation of savings and offer of financings of entrepreneurial initiatives, which can bring obvious benefits for job creation.

Credit cooperatives’ financial and economic performanceIudícibus (2008) explains that the assessment of financial and economic performance, through the analysis of financial statements, is not new in the organizations.

The analysis of financial statements within bank systems appeared in the late nineteenth century in the United States. They have emerged from the moment the bankers began to require financial statements of companies borrowing loans. In Brazil, this analysis gained momentum after 1968, with the creation of the Centralized Banking Services SA (SERASA). Since then, SERASA has functioned as an analysis center of balance sheet for commercial banks (Ferreira, 1999).

Assaf Neto (2010, p. 35) warns that the purpose of performance appraisal is “to report, based on the financial information provided by companies, their current economic and financial position, the causes determining their evolution and the future trends”. Such an assessment makes it possible for the evaluator to obtain past information on the financial position of an organization leading future projections.

The use of performance indicators developed adequately to the needs of the institutions provides the managers with speed, efficiency and safety. It is through measurement that one obtains the information needed for evaluating the performance of a process or a system. Measurement gives the managers the chance to check whether the objectives or goals are being achieved. Besides, measurement gives room for the definition of new actions, if necessary (Holanda, Cavalcante, & Carvalho, 2009).

The analysis of indexes is an important tool to the financial manager. It has provided him with the ability to predict business failure by analyzing the characteristics of the different groups acting inside the companies (Altman, 1970). However, according to Macedo, Silva, and Santos (2006), the analysis of an organization's performance is subject to many discussions and questions about which indicators to use and how to consolidate them.

Meyer and Pifer (1970) have proposed a model of eight indicators predicting the banks’ bankruptcy. This set of indicators aims at evaluating the performance of banking activities. They are: managers’ indebtedness, loan growth, interest rates on deposits, cost growth, actual loans, returns on loans, asset quality, and asset growth. After further adjustments, this model was called CAMEL, with 5 groups of indicators, such as: capital adequacy, asset quality, management capability, returns efficiency, liquidity, and market-risk sensibility.

The research Sinkey (1975) highlights the work started by Meyer and Pifer (1970), examined the problems of the banks, especially good discriminant indicators such as the composition of assets, the characteristics of the loan, the adequacy of capital, origins and applications of revenues, efficiency and profitability. Stuhr and Wicklen (1974), Korobow and Stuhr (1975) and Thomson (1991) highlight the use of data published by banks to analyze the economic and financial situation, especially the structure presented by the CAMEL model that considers the 5 groups indicators (Capital adequacy, Asset quality, Management expertise, Liquidity and sensitivity to market risk) expressing adequacy of capital, quality of assets, capacity management, efficiency of returns, liquidity and sensitivity to market risk. The measurement of financial performance for the CAMEL model was developed as financial indicators in banks, and this research was used to measure the natural risk in the credit activity of credit unions.

In the models described in the literature, the CAMEL model (adequacy Capital, Asset quality, Management expertise, Liquidity and Sensitivity to market risk) stands due to be original research, as Meyer and Piffer (1970), Stuhr and Wicklen (1974), Martin (1977), Hartwick (1977), Parliament, Lennan, and Fulton (1990), Thomson (1991), Cornett and Tehranian (1992), Barr, Seiford, and Siems (1994), Fischer and Smaoui (1997), Nikolsko-Rzhevskyy (2003), among others, that structured the valuation model of financial performance in financial institutions.

Corroborating the studies by Meyer and Pifer (1970), researchers such as Parliament, Lerman, and Fulton (1990) have pointed out that the measuring tools of the financial performance of the cooperatives must be approached from five financial indexes highlighting corporate objectives. These assessment guidelines include profitability, leverage, solvency, liquidity and efficiency.

Others like Evans et al. (2000) suggest that each of the 5 groups of CAMEL model results in various types of information needed for performance evaluation. The capital adequacy group establishes the level of risk that is acceptable in a given operation. The behavior of the capital must be constantly monitored, for it shows both qualitative and quantitative aspects. The analysis of both the composition and the evolution of the structure of the asset is an important aspect allowing the knowledge of the operating direction and the level of quality to take place. Likewise, the volume of results earned by the banking system in each country is a critical variable to performance assessment. The ability to create results is crucial to the continuity of the institutions and the financial system under capitalism. Moreover, liquidity reveals problems caused by both the credit's poor quality and lack of receipts.

Several studies have accompanied the use of financial and economic indicators in the banking sector. Among them stands out Capelletto (2006) research. He sought to measure the level of systemic risk in the financial sector, using part of the CAMEL model to demonstrate that financial indicators and risks show informational content. The results have indicated that both accounting and economic variables most associated with the occurrence of seizures were related to the credit quality, to the volume of results and the level of interest rates. In addition, all indicators emerging from these variables were identified as relevant in the classification process. The emphasis is on those variables related to the volatility of default, of returns and of interest rates, as well as to the average of profitability and credit risk.

Methodological proceduresThe analysis of the economic and financial performance of the largest Brazilian credit cooperatives followed a descriptive-qualitative research through documentary and bibliographic procedures.

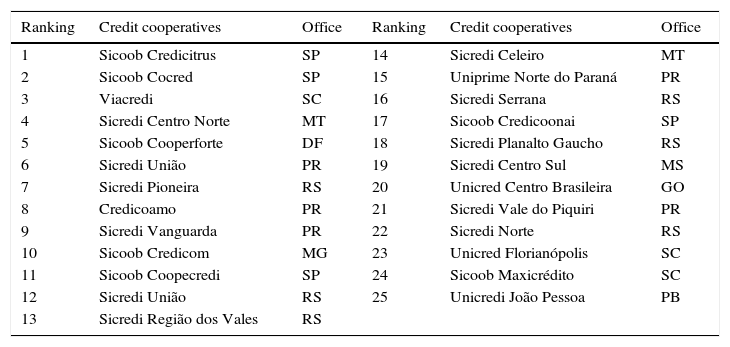

Data from the Central Bank of Brazil (BACEN, 2013) indicate that, in 2013, there were 1,192 credit cooperatives in operation in Brazil. However, the sample used by our research consists of the 25 largest credit cooperatives, in accordance with Central Bank of Brazil's December 2013 data which have provided the data for the period under review. The composition of this sample can be seen in Table 1.

Credit cooperative ranking.

| Ranking | Credit cooperatives | Office | Ranking | Credit cooperatives | Office |

|---|---|---|---|---|---|

| 1 | Sicoob Credicitrus | SP | 14 | Sicredi Celeiro | MT |

| 2 | Sicoob Cocred | SP | 15 | Uniprime Norte do Paraná | PR |

| 3 | Viacredi | SC | 16 | Sicredi Serrana | RS |

| 4 | Sicredi Centro Norte | MT | 17 | Sicoob Credicoonai | SP |

| 5 | Sicoob Cooperforte | DF | 18 | Sicredi Planalto Gaucho | RS |

| 6 | Sicredi União | PR | 19 | Sicredi Centro Sul | MS |

| 7 | Sicredi Pioneira | RS | 20 | Unicred Centro Brasileira | GO |

| 8 | Credicoamo | PR | 21 | Sicredi Vale do Piquiri | PR |

| 9 | Sicredi Vanguarda | PR | 22 | Sicredi Norte | RS |

| 10 | Sicoob Credicom | MG | 23 | Unicred Florianópolis | SC |

| 11 | Sicoob Coopecredi | SP | 24 | Sicoob Maxicrédito | SC |

| 12 | Sicredi União | RS | 25 | Unicredi João Pessoa | PB |

| 13 | Sicredi Região dos Vales | RS |

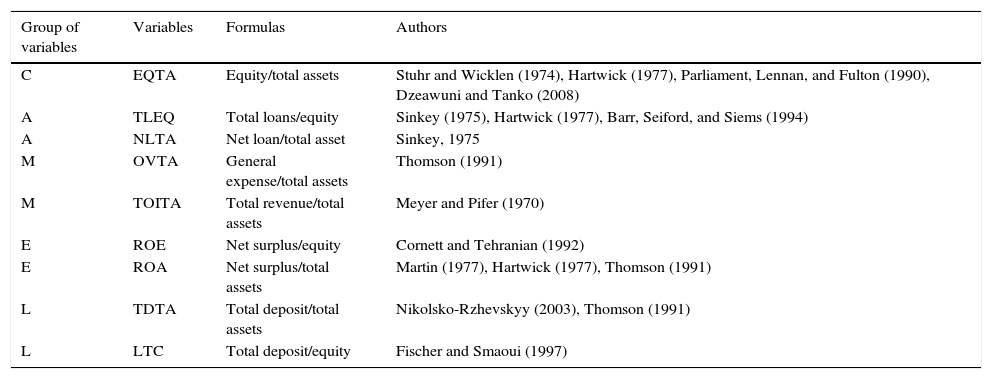

The collection of data took place in December 2013, and the study period covered 5 years, from 2008 to 2012. Financial indicators based on the CAMEL model were considered, as Table 2 shows.

Variables.

| Group of variables | Variables | Formulas | Authors |

|---|---|---|---|

| C | EQTA | Equity/total assets | Stuhr and Wicklen (1974), Hartwick (1977), Parliament, Lennan, and Fulton (1990), Dzeawuni and Tanko (2008) |

| A | TLEQ | Total loans/equity | Sinkey (1975), Hartwick (1977), Barr, Seiford, and Siems (1994) |

| A | NLTA | Net loan/total asset | Sinkey, 1975 |

| M | OVTA | General expense/total assets | Thomson (1991) |

| M | TOITA | Total revenue/total assets | Meyer and Pifer (1970) |

| E | ROE | Net surplus/equity | Cornett and Tehranian (1992) |

| E | ROA | Net surplus/total assets | Martin (1977), Hartwick (1977), Thomson (1991) |

| L | TDTA | Total deposit/total assets | Nikolsko-Rzhevskyy (2003), Thomson (1991) |

| L | LTC | Total deposit/equity | Fischer and Smaoui (1997) |

Note: C=capital; A=assets; M=management; E=efficiency; L=liquidity.

For analysis of the financial performance we used the Camel model (adequacy Capital, Asset quality, Management expertise, Liquidity and Sensitivity to market risk) which are Capital, Assets, Management Capacity, results, liquidity and sensitivity to risk in the market, recommended Meyer and Piffer (1970), used in credit unions by similarity in developed financial activities. Besides being the pioneer model highlighted by foreign research showed the large volume of research in finance journals. As pointed out by Sangmi and Nazir (2010), the CAMEL model has been used successfully by many researchers to assess the financial performance of banks in one of the most recent studies done. Already Shar, Shah, and Jamali (2010) highlighted the feasibility of performance evaluation of financial institutions using the CAMEL model. In Brazil, this model was used to estimate the systemic risk in the banking sector with the use of financial and economic variables (Capelletto and Corrar, 2008; Capelletto, 2006).

To measure the economic and financial performance of Brazilian credit cooperatives made use of data from financial statements provided by the Central Bank of Brazil (BCB). In the context of this work, we used the data envelopment analysis (DEA) to check the efficiency of the credit unions that make up the sample. In DEA, mathematical programming is used to measure the efficiency in terms of distance of each DMU (Decision Making Units) of their respective border efficiency, determined from the unit assembly production data (Ferreira, Gonçalves, & Braga, 2007). In this sense, this technique allows you to compare business performance, measuring the effectiveness of each cooperative in relation to it.

The DEA converts the various inputs and outputs on a scale of measure of efficiency, building a nonparametric frontier of having a great efficiency on a set of data allowing a measure of comparative efficiency, thus generating a scale of relative efficiency for the group analyzed (Hu, Iq, & Yang, 2012). This analysis provides an indicator that varies from 0 to 1 or from 0% to 100%. The closer to 1, the more efficient is considered the DMU and scores equal to 1 indicates efficiency.

Thus, it is possible to assess how many DMUs are efficient and those that are not effective and for these, the DMUs that serve as a reference (benchmark) to increase efficiency (Macedo, Barbosa, & Cavalcante, 2009). Only companies that achieve efficiency ratio is equal to 1 that are actually effective. The model seeks to identify the efficiency of comparing the company with the best observed performance. When companies use the market as a benchmark, according to performance standards competition, you must use a so-called benchmarking approach. This approach is the relative performance of the companies in terms of a set of pre-selected competitors (Slack et al., 2002).

There are two traditional DEA models. The first model is the CCR developed by Charnes, Cooper, and Rhode (1978), also known as CRS (Constant Return to Scale). The second model is the BBC, or VRS (Variable Retur to Scale) developed by Banker, Charne, and Cooper (1984). In this study, we use the BCC model-orientation to maximize the business performance indicators (output). The BCC model allows the projection of each inefficient DMU on the boundary surface (envelope) determined by the efficient DMUs compatible size (Macedo et al., 2009). The mathematical Eq. (1) represents the BCC model with output orientation:

Subject to

Uj, vi≥0, i, j.

We used the TLEQ variables NLTA, OVTA, TOITA, ROE, ROA, TDTA and LTC as inputs and variable EQTA as output. For this, we used the statistical software MaxDEA®.

In this sense, we seek to identify the economic and financial performance of Brazilian credit cooperatives and to identify factors associated with efficiency, enabling inefficient cooperatives improve their performance, mirroring us their benchmarks. Specifically intended to measure the degree of technical efficiency and scale through the relationship between variables and identify the determinants of efficiency. This approach will highlight the factors that determine the greater business efficiency of a company in relation to others.

Data description and analysisOf the total of the indicators from CAMEL model, we were able to show the calculation of 9 of them. This number was limited by the non-disclosure of certain variables in the accounting statements submitted by the credit cooperatives.

The analysis of the indicator EQTA for both the five years of analysis and the 25 Brazilian credit cooperatives are viewed in Table 3.

Equity over total assets (EQTA) indicator.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.855 | 0.923 | 0.893 | 0.858 | 0.906 | 0.894 | 0.877 | 0.886 | 0.854 | 0.859 | 0.849 | 0.853 | 0.851 |

| 2009 | 0.861 | 0.918 | 0.890 | 0.871 | 0.907 | 0.899 | 0.886 | 0.889 | 0.854 | 0.857 | 0.848 | 0.867 | 0.857 |

| 2010 | 0.860 | 0.921 | 0.843 | 0.864 | 0.907 | 0.894 | 0.880 | 0.898 | 0.867 | 0.845 | 0.842 | 0.872 | 0.878 |

| 2011 | 0.862 | 0.918 | 0.888 | 0.869 | 0.907 | 0.895 | 0.883 | 0.898 | 0.863 | 0.847 | 0.849 | 0.876 | 0.882 |

| 2012 | 0.865 | 0.915 | 0.888 | 0.870 | 0.908 | 0.866 | 0.882 | 0.896 | 0.866 | 0.852 | 0.854 | 0.876 | 0.885 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.873 | 0.929 | 0.856 | 0.836 | 0.874 | 0.877 | 0877 | 0.845 | 0.855 | 0.898 | 0.802 | 0.927 | – |

| 2009 | 0.879 | 0.924 | 0.863 | 0.844 | 0.885 | 0.884 | 0.885 | 0.851 | 0.854 | 0.896 | 0.822 | 0.921 | – |

| 2010 | 0.872 | 0.917 | 0.860 | 0.843 | 0.878 | 0.832 | 0.885 | 0.818 | 0.861 | 0.894 | 0.834 | 0.914 | – |

| 2011 | 0.869 | 0.917 | 0.893 | 0.840 | 0.879 | 0.885 | 0.887 | 0.861 | 0.863 | 0.894 | 0.840 | 0.909 | – |

| 2012 | 0.869 | 0.916 | 0.851 | 0.851 | 0.879 | 0.880 | 0.890 | 0.865 | 0.861 | 0.892 | 0.849 | 0.910 | – |

The indicator's comparability represents the subscribed resources or the provision of the assemblies on the total potential that the cooperatives have, financially and economically, to capitalize on the initial investments of the associates. The results presented highlight the lack of significant differences among the cooperatives. The indicators show balance and the cooperatives do not show behaviors apart from the group. However, three cooperatives – Sicoob Cocred, Sicredi Celeiro and Uniprime Norte do Paraná – show a reduction slope in this indicator over the five years. These three companies had a lower concentration of resources in equity compared to total assets. In addition, six cooperatives have reported an increase of the indicator, due to the increase in equity holdings over total assets. These companies were Sicoob Credicitrus, Sicredi União, Sicredi Região dos Vales, Unicred Centro Brasileiro, Sicredi Norte and Sicoob Maxicredito.

In addition, in the years 2008, 2009 and 2012, Uniprime Norte do Paraná became the cooperative with greater indicator of equity by total assets. In 2010 and 2011, Sicoob Cocred was the cooperative with the highest indicator. The lowest indicators in 2008, 2009 and 2010 were reached by Socoob Maxicrédito. In 2010, the lowest score was obtained by Sicredi Vale do Piquiri ABCD; and in 2011, by Sicoob Credicoonai.

The analysis of the indicators Capital and net assets over total assets shows the comparability between the credit cooperatives, as Stuhr and Wicklen (1974) and Hartwick (1977) point out. The best relation to capital to be used by banks’ regulators should be that between the shareholders’ fund and total assets (Dzeawuni and Tanko, 2008).

In the case of the group of assets, in Table 4, one can view the performance of the cooperatives with regard to the relationship of their total loans with equity.

Indicator of total credit on equity.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 1.050 | 0.970 | 1.044 | 1.108 | 0.936 | 1.094 | 1.062 | 1.057 | 1.075 | 1.050 | 1.064 | 1.096 | 1.067 |

| 2009 | 1.041 | 0.976 | 1.049 | 1.089 | 1.055 | 1.073 | 1.051 | 1.050 | 1.072 | 1.054 | 1.056 | 1.081 | 1.055 |

| 2010 | 1.038 | 0.976 | 1.074 | 1.097 | 1.056 | 1.084 | 1.059 | 1.033 | 1.072 | 1.057 | 1.068 | 1.072 | 1.039 |

| 2011 | 1.037 | 0.979 | 1.051 | 1.094 | 1.057 | 1.087 | 1.054 | 1.033 | 1.079 | 1.055 | 1.054 | 1.065 | 1.034 |

| 2012 | 1.041 | 0.983 | 1.053 | 1.090 | 1.057 | 1.086 | 1.059 | 1.034 | 1.079 | 1.064 | 1.051 | 1.064 | 1.030 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 1.080 | 0.995 | 1.048 | 1.088 | 1.079 | 1.073 | 1.077 | 1.086 | 1.099 | 1.035 | 1.117 | 0.993 | – |

| 2009 | 1.072 | 1.005 | 1.029 | 1.074 | 1.059 | 1.066 | 1.068 | 1.080 | 1.101 | 1.047 | 1093 | 1.013 | – |

| 2010 | 1.079 | 1.012 | 1.047 | 1.074 | 1.072 | 1.063 | 1.074 | 1.075 | 1.087 | 1.055 | 1.076 | 1.032 | – |

| 2011 | 1.081 | 1.013 | 1.022 | 1.080 | 1.067 | 1.060 | 1.068 | 1.079 | 1.079 | 1.057 | 1.074 | 1.039 | – |

| 2012 | 1.086 | 1.013 | 1.071 | 1.071 | 1.070 | 1.073 | 1.064 | 1.081 | 1.088 | 1.069 | 1070 | 1.040 | – |

On average the indicator of the total loans by equity of the credit cooperatives was 1.058. The number indicates that the total loans provided by the cooperatives are approximately 6% higher than their equity. One can observe that Sicredi Centro Norte was the cooperative receiving the highest indicators of impairment of its equity with its total loans available to members. Sicoob Cocred, in the years 2009, 2010, 2011 and 2012, was the cooperative with the lowest indicator of impairment of its equity with total loans. In 2008, Sicredi Cooperforte presented the lowest indicator.

The other indicator of the group's assets matches the indicator of net loans on total assets. This indicator, less the provision for doubtful accounts, over the period, represents the possibility of increasing of the commitment of the cooperative's management of credits. This indicates the need for changes in the instruments of management control. The results found for the cooperatives under study can be seen in Table 5.

Indicator of total credit on total assets.

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.898 | 0.897 | 0.933 | 0.952 | 0.959 | 0.981 | 0.933 | 0.938 | 0.921 | 0.904 | 0.904 | 0.937 | 0.911 |

| 2009 | 0.897 | 0.899 | 0.934 | 0.952 | 0.958 | 0.970 | 0.934 | 0.935 | 0.919 | 0.905 | 0.896 | 0.941 | 0.910 |

| 2010 | 0.893 | 0.902 | 0.908 | 0.951 | 0.959 | 0.973 | 0.935 | 0.930 | 0.932 | 0.896 | 0.899 | 0.940 | 0.918 |

| 2011 | 0.895 | 0.902 | 0.935 | 0.953 | 0.960 | 0.976 | 0.934 | 0.929 | 0.934 | 0.895 | 0.895 | 0.939 | 0.919 |

| 2012 | 0.902 | 0.902 | 0.937 | 0.951 | 0.960 | 0.943 | 0.937 | 0.927 | 0.937 | 0.908 | 0.897 | 0.936 | 0.917 |

| Year | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.946 | 0.925 | 0.902 | 0.913 | 0.948 | 0.944 | 0.947 | 0.920 | 0.943 | 0.931 | 0.897 | 0.922 | – |

| 2009 | 0.946 | 0.930 | 0.890 | 0.908 | 0.943 | 0.945 | 0.947 | 0.922 | 0.945 | 0.939 | 0.900 | 0.934 | – |

| 2010 | 0.944 | 0.930 | 0.902 | 0.908 | 0.944 | 0.888 | 0.952 | 0.882 | 0.939 | 0.944 | 0.899 | 0.944 | – |

| 2011 | 0.942 | 0.930 | 0.914 | 0.909 | 0.941 | 0.940 | 0.949 | 0.931 | 0.938 | 0.947 | 0.903 | 0.947 | – |

| 2012 | 0.946 | 0.929 | 0.913 | 0.913 | 0.943 | 0.946 | 0.948 | 0.937 | 0.940 | 0.954 | 0.910 | 0.948 | – |

With respect to this indicator, the cooperatives under analysis had a similar behavior in the five years studied. On average, net credits accounted for 92% of the total assets of the cooperatives. Presenting a decline, during the period of analysis, stood out Sicredi União PR, Crediamo and Sicoob Coopecredi.

In the years 2008, 2009, 2010 and 2011, Sicredi União PR was the cooperative showing the greatest indicator of net credit on total assets. In 2012, Sicredi Cooperforte had the highest indicator. The cooperatives Sicoob Cocred and Sicoob Maxicredito were those with lower indicator in 2008. In 2009, Sicredi Serrana RS was the one with lower indicator. In 2010, Sicredi Vale do Piquiri ABCD, in 2011, Sicoob Credicom, and in 2012, Sicredi Coopecredi, also had lower indicators, respectively.

The management of credits represents the cooperatives’ commitment with the associates’ interests. This corresponds to the associates’ adequate analysis in the granting of credit. This also matches the susceptibility to the cooperative principle of “risk, mutual responsibility and sharing” (Barr, Seiford, & Siems, 1994; Sinkey, 1975).

The results of the group of indicators related to the management of the entity, Overhead over Total Assets (OVTA) and Total Income over Total Assets (TOITA), can be seen in Tables 6 and 7.

Indicator overheads over total assets.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.825 | 0.880 | 0.865 | 0.926 | 0.883 | 0.939 | 0.896 | 0.838 | 0.883 | 0.881 | 0.836 | 0.897 | 0.873 |

| 2009 | 0.827 | 0.859 | 0.872 | 0.908 | 0.883 | 0.946 | 0.894 | 0.833 | 0.877 | 0.866 | 0.822 | 0.897 | 0.876 |

| 2010 | 0.835 | 0.878 | 0.832 | 0.911 | 0.883 | 0.935 | 0.902 | 0.828 | 0.891 | 0.866 | 0.833 | 0.890 | 0.891 |

| 2011 | 0.834 | 0.878 | 0.876 | 0.916 | 0.883 | 0.935 | 0.897 | 0.841 | 0.890 | 0.868 | 0.841 | 0.910 | 0.893 |

| 2012 | 0.832 | 0.867 | 0.871 | 0.909 | 0.877 | 0.900 | 0.899 | 0.836 | 0.888 | 0.860 | 0.833 | 0.906 | 0.886 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.913 | 0.877 | 0.882 | 0.838 | 0.889 | 0.914 | 0.884 | 0.885 | 0.895 | 0.876 | 0.839 | 0.869 | – |

| 2009 | 0.909 | 0.875 | 0.865 | 0.835 | 0.897 | 0.905 | 0.878 | 0.883 | 0.903 | 0.865 | 0.827 | 0.857 | – |

| 2010 | 0.910 | 0.870 | 0.856 | 0.832 | 0.905 | 0.850 | 0.883 | 0.846 | 0.899 | 0.869 | 0.827 | 0.857 | – |

| 2011 | 0.904 | 0.877 | 0.861 | 0.832 | 0.882 | 0.899 | 0.887 | 0.889 | 0.910 | 0.874 | 0.835 | 0.853 | – |

| 2012 | 0.882 | 0.868 | 0.837 | 0.837 | 0.885 | 0.892 | 0.884 | 0.886 | 0.891 | 0.867 | 0.843 | 0.847 | – |

Indicator revenue over total assets.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.809 | 0.839 | 0.845 | 0.894 | 0.868 | 0.905 | 0.868 | 0.824 | 0.851 | 0.851 | 0.812 | 0.863 | 0.844 |

| 2009 | 0.805 | 0.826 | 0.843 | 0.876 | 0.862 | 0.912 | 0.862 | 0.821 | 0.848 | 0.835 | 0.793 | 0.864 | 0.847 |

| 2010 | 0.807 | 0.843 | 0.808 | 0.885 | 0.862 | 0.903 | 0.872 | 0.826 | 0.864 | 0.833 | 0.815 | 0.861 | 0.862 |

| 2011 | 0.810 | 0.829 | 0.847 | 0.885 | 0.865 | 0.905 | 0.873 | 0.832 | 0.863 | 0.836 | 0.813 | 0.878 | 0.863 |

| 2012 | 0.808 | 0.823 | 0.845 | 0.880 | 0.856 | 0.871 | 0.870 | 0.824 | 0.861 | 0.830 | 0.804 | 0.878 | 0.859 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.881 | 0.841 | 0.850 | 0.813 | 0.861 | 0.882 | 0.858 | 0.853 | 0.861 | 0.855 | 0.813 | 0.852 | – |

| 2009 | 0.877 | 0.847 | 0.829 | 0.809 | 0.866 | 0.871 | 0.858 | 0.853 | 0.875 | 0.848 | 0.808 | 0.833 | – |

| 2010 | 0.880 | 0.843 | 0.821 | 0.808 | 0.878 | 0.822 | 0.860 | 0.819 | 0.869 | 0.854 | 0.810 | 0.835 | – |

| 2011 | 0.875 | 0.848 | 0.834 | 0.810 | 0.857 | 0.871 | 0.864 | 0.864 | 0.876 | 0.856 | 0.818 | 0.840 | – |

| 2012 | 0.857 | 0.845 | 0.816 | 0.816 | 0.857 | 0.865 | 0.862 | 0.860 | 0.860 | 0.844 | 0.824 | 0.838 | – |

The indicator of overheads over total assets highlights the overall consumption of resources in the maintenance activity of credit activities. This depends on the equity that the cooperative disposes for the generation of wealth to shareholders. Thus, it can be observed that the cooperatives have a balanced index relative to the indicator. Moreover, on average, the cooperatives studied consume 87.7% of resources in the maintenance of the credit activities.

Sicoob União PR was the cooperative that got the highest indicator of overheads by total assets in 2008, 2009, 2010 and 2011. In 2012, Sicredi Centro Norte MT was the one with the highest indicator. Sicoob Credicitrus had lower indicator in 2008 and 2012. The indicator reports on the cooperative's lower consumption of resources to maintain its activities. Moreover, Sicoob Coopecredi, Sicoob Maxicrédito and Sicoob Credicoonai obtained the lowest indicator in the years 2009, 2010 and 2011, respectively.

The indicator of income over total assets (TOITA) highlights the creation of revenues over total assets. This indicates how efficiently are used the assets of the cooperative promote revenue. The results can be seen in Table 7.

The cooperatives have reached a rate of 84.85%, on average, in efficiency in the use of their equity to promote revenue. Sicoob União PR was the cooperative with the highest overheads indicator by total assets in the years 2008, 2009, 2010 and 2011. In 2012, Sicredi Centro Norte MT showed the highest indicator. Sicoob Credicitrus had lower indicator in the years 2008, 2010 and 2011. Moreover, Sicoob Coopecredi had the lowest indicator in the years 2009 and 2011.

The results visible in the companies’ management of group indicators highlight the competent performance of the cooperatives’ resources indicating the balanced outcome in the credit activity. When compared with the studies conducted by Meyer and Pifer (1970) and Thomson (1991), these results stress the efficient management and its connections with the variables of income and dividends from a positive point of view; and with fundraising from a negative perspective.

Efficiency group's indicators are measured by the returns obtained when compared with the total assets and equity. These indicators provide an assessment of the real potential of wealth production by using the assets and equity of the cooperative. The use of ROE, in Table 8, evidences the cooperatives’ management of higher returns on the partners’ capital.

ROE.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.867 | 0.824 | 0.859 | 0.848 | 0.879 | 0.864 | 0.860 | 0.872 | 0.840 | 0.825 | 0.861 | 0.799 | 0.868 |

| 2009 | 0.862 | 0.703 | 0.863 | 0.899 | 0.887 | 0.760 | 0.865 | 0.877 | 0.867 | 0.852 | 0.847 | 0.863 | 0.870 |

| 2010 | 0.857 | 0.802 | 0.852 | 0.743 | 0.874 | 0.802 | 0.817 | 0.865 | 0.863 | 0.858 | 0.856 | 0.756 | 0.871 |

| 2011 | 0.861 | 0.828 | 0.868 | 0.876 | 0.878 | 0.800 | 0.989 | 0.861 | 0.881 | 0.882 | 0.861 | 0.874 | 0.879 |

| 2012 | 0.873 | 0.815 | 0.886 | 0.875 | 0.873 | 0.856 | 0.868 | 0.871 | 0.882 | 0.883 | 0.794 | 0.846 | 0.862 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.871 | 0.778 | 0.829 | 0.583 | 0.864 | 0.867 | 0.857 | 0.808 | 0.813 | 0.880 | 0.865 | 0.800 | – |

| 2009 | 0.884 | 0.807 | 0.880 | 0.838 | 0.888 | 0.880 | 0.887 | 0.832 | 0.840 | 0.860 | 0.905 | 0.812 | – |

| 2010 | 0.866 | 0.838 | 0.795 | 0.852 | 0.838 | 0.820 | 0.889 | 0.826 | 0.788 | 0.907 | 0.889 | 0.836 | – |

| 2011 | 0.880 | 0.814 | 0.836 | 0.859 | 0.887 | 0.881 | 0.893 | 0.873 | 0.832 | 0.873 | 0.893 | 0.815 | – |

| 2012 | 0.886 | 0.781 | 0.847 | 0.847 | 0.896 | 0.877 | 0.883 | 0.894 | 0.805 | 0.859 | 0.877 | 0.858 | – |

Unicred Florianópolis showed higher performance in the years 2008 and 2010. During 2009, 2011 and 2012, the cooperatives Sicoob Maxicredito, Sicredi Pioneira RS and Sicredi Planalto Gaucho RS had higher performance, respectively. Lower performance in the five years were with the following cooperatives: in 2008, Sicoob Credicoonai with an index of 0.583; in 2009, Sicoob Cocred with an index of 0.703; in 2010, Sicredi Centro Norte with an index of 0.743; in 2011, Sicredi União with an index of 0.800; finally, in 2012, Uniprime Norte do Paraná with an index of 0.781.

Net Income over Total Assets (ROA) measures the net income provided by the use of the total resources of the cooperative, represented by total assets. The results are in Table 9.

ROA.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.741 | 0.760 | 0.767 | 0.727 | 0.797 | 0.772 | 0.755 | 0.772 | 0.717 | 0.709 | 0.731 | 0.682 | 0.738 |

| 2009 | 0.743 | 0.646 | 0.768 | 0.784 | 0.805 | 0.683 | 0.766 | 0.780 | 0.741 | 0.730 | 0.718 | 0.749 | 0.745 |

| 2010 | 0.737 | 0.738 | 0.719 | 0.641 | 0.793 | 0.717 | 0.719 | 0.777 | 0.748 | 0.725 | 0.721 | 0.659 | 0.764 |

| 2011 | 0.742 | 0.760 | 0.771 | 0.761 | 0.796 | 0.716 | 0.873 | 0.773 | 0.760 | 0.746 | 0.731 | 0.766 | 0.776 |

| 2012 | 0.755 | 0.745 | 0.787 | 0.761 | 0.793 | 0.741 | 0.765 | 0.780 | 0.764 | 0.752 | 0.678 | 0.741 | 0.763 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.761 | 0.723 | 0.709 | 0.487 | 0.756 | 0.760 | 0.752 | 0.683 | 0.695 | 0.791 | 0.693 | 0.741 | – |

| 2009 | 0.777 | 0.745 | 0.759 | 0.707 | 0.786 | 0.778 | 0.785 | 0.708 | 0.717 | 0.771 | 0.744 | 0.748 | – |

| 2010 | 0.755 | 0.769 | 0.683 | 0.719 | 0.735 | 0.683 | 0.787 | 0.675 | 0.678 | 0.811 | 0.742 | 0.764 | – |

| 2011 | 0.765 | 0.746 | 0.747 | 0.722 | 0.780 | 0.779 | 0.792 | 0.752 | 0.719 | 0.780 | 0.750 | 0.742 | – |

| 2012 | 0.770 | 0.715 | 0.721 | 0.721 | 0.788 | 0.772 | 0.786 | 0.773 | 0.693 | 0.766 | 0.744 | 0.781 | – |

The cooperative Sicredi Cooperforte showed higher performance in its assets, in the years 2008, 2009 and 2012. Unicred Florianópolis obtained higher performance in 2010; and Sicredi Pioneira RS, in 2011. Regarding the lower performance, Sicoob Credicoonai, Sicoob Cocred, Sicredi Centro Norte MT, Sicredi União PR and Sicoob Coopecredi showed lower indicator in the 5 years, respectively.

The results above allow us to establish connections with the researchers Parliament, Lennan, and Fulton (1990), Martin (1977), Hartwick (1977), Thomson (1991), Cornett and Tehranian (1992). These comparisons highlight the cooperatives’ potential tendency to lower investment in their base of assets. These smaller investments may result in lower rates of return on total assets for the cooperatives than for financial institutions.

The indicator of the total deposit on total assets shows the representativeness of the deposit made by the cooperative client partner, which, in case of the cooperative settlement, highlights the level of liquidity that will indicate the cooperative's involvement with its lender. The results are in Table 10.

Full tank indicator of total assets.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.874 | 0.934 | 0.938 | 0.887 | 0.954 | 0.961 | 0.952 | 0.883 | 0.911 | 0.961 | 0.899 | 0.937 | 0.935 |

| 2009 | 0.869 | 0.936 | 0.940 | 0.891 | 0.956 | 0.968 | 0.951 | 0.881 | 0.923 | 0.958 | 0.902 | 0.934 | 0.931 |

| 2010 | 0.878 | 0.934 | 0.883 | 0.899 | 0.958 | 0.968 | 0.952 | 0.899 | 0.939 | 0.948 | 0.908 | 0.938 | 0.949 |

| 2011 | 0.882 | 0.933 | 0.942 | 0.900 | 0.958 | 0.970 | 0.953 | 0.901 | 0.945 | 0.948 | 0.909 | 0.937 | 0.952 |

| 2012 | 0.884 | 0.933 | 0.941 | 0.900 | 0.958 | 0.936 | 0.952 | 0.914 | 0.940 | 0.954 | 0.913 | 0.936 | 0.954 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 0.902 | 0.930 | 0.921 | 0.870 | 0.908 | 0.927 | 0.952 | 0.915 | 0.934 | 0.960 | 0.907 | 0.924 | – |

| 2009 | 0.903 | 0.925 | 0.921 | 0.874 | 0.913 | 0.926 | 0.951 | 0.916 | 0.938 | 0.958 | 0.898 | 0.920 | – |

| 2010 | 0.904 | 0.931 | 0.914 | 0.883 | 0.911 | 0.884 | 0.952 | 0.890 | 0.942 | 0.958 | 0.898 | 0.917 | – |

| 2011 | 0.911 | 0.938 | 0.945 | 0.877 | 0.916 | 0.937 | 0.955 | 0.939 | 0.945 | 0.958 | 0.899 | 0.926 | – |

| 2012 | 0.900 | 0.942 | 0.882 | 0.882 | 0.919 | 0.931 | 0.953 | 0.936 | 0.940 | 0.955 | 0.905 | 0.933 | – |

Sicredi União PR showed the highest indicator of total deposit on total assets, in the years 2009, 2010 and 2011. Sicoob Credicom and Sicredi Cooperforte had higher indicators in 2008 and 2012, respectively. Sicoob Credicoonai obtained the lowest indicators in the years 2008 and 2011. Sicoob The Credicitrus had lower indicators in the years 2009 and 2010 and Sicredi Serrana RS showed lower indicator in 2012. These cooperatives have lower assets impairment compared with the deposits received.

Regarding the total deposit on equity, which measures the capability to settlement of the deposits received by cooperatives using the equity, the results are seen in Table 11.

Indicator of total deposit on equity.

| YEAR | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 1.022 | 1.012 | 1.051 | 1.034 | 1.052 | 1.075 | 1.085 | 0.997 | 1.067 | 1.119 | 1.059 | 1.098 | 1.099 |

| 2009 | 1.009 | 1.019 | 1.057 | 1.022 | 1.054 | 1.077 | 1.073 | 0.990 | 1.080 | 1.117 | 1.064 | 1.076 | 1.086 |

| 2010 | 1.021 | 1.015 | 1.046 | 1.041 | 1.056 | 1.082 | 1.083 | 1.000 | 1.083 | 1.121 | 1.079 | 1.076 | 1.081 |

| 2011 | 1.023 | 1.016 | 1.060 | 1.036 | 1.056 | 1.084 | 1.079 | 1.003 | 1.094 | 1.120 | 1.071 | 1.069 | 1.079 |

| 2012 | 1.022 | 1.019 | 1.059 | 1.035 | 1.055 | 1.081 | 1.079 | 1.020 | 1.085 | 1.120 | 1.069 | 1.069 | 1.079 |

| YEAR | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | – |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 1.033 | 1.002 | 1.076 | 1.041 | 1.038 | 1.057 | 1.085 | 1.083 | 1.092 | 1.068 | 1.131 | 0.996 | – |

| 2009 | 1.027 | 1.002 | 1.067 | 1.035 | 1.032 | 1.048 | 1.075 | 1.076 | 1.097 | 1.069 | 1.092 | 0.999 | – |

| 2010 | 1.036 | 1.015 | 1.064 | 1.046 | 1.038 | 1.063 | 1.075 | 1.088 | 1.094 | 1.072 | 1.077 | 1.004 | – |

| 2011 | 1.048 | 1.024 | 1.059 | 1.044 | 1.042 | 1.059 | 1.077 | 1.090 | 1.094 | 1.072 | 1.070 | 1.018 | – |

| 2012 | 1.036 | 1.028 | 1.037 | 1.037 | 1.046 | 1.058 | 1.071 | 1.082 | 1.091 | 1.071 | 1.066 | 1.025 | – |

The cooperative with lower capacity to settlement, if used the equity to refund the amounts deposited, was the Crediamo. In the 5 years of the analysis, the cooperative showed a higher degree of impairment to settle the deposits received. Sicoob Credicom was the cooperative with higher degree of settlement capacity, in the years 2009, 2010, 2011 and 2012. In 2008, the Sicoob Maxicredito showed higher capacity indicator.

The results above allow a comparative analysis of the research conducted by Parliament, Lennan, and Fulton (1990). These researchers show that a high liquidity is a conservative approach, designed to protect the company against the risk of default on the part of current liabilities. Besides, they argue that the behavior of moral hazard may induce the cooperatives to accept lower rate of liquidity. These results are also shared by Martin (1977), Thomson (1991), Fischer and Smaoui (1997) and Nikolsko-Rzhevskyy (2003).

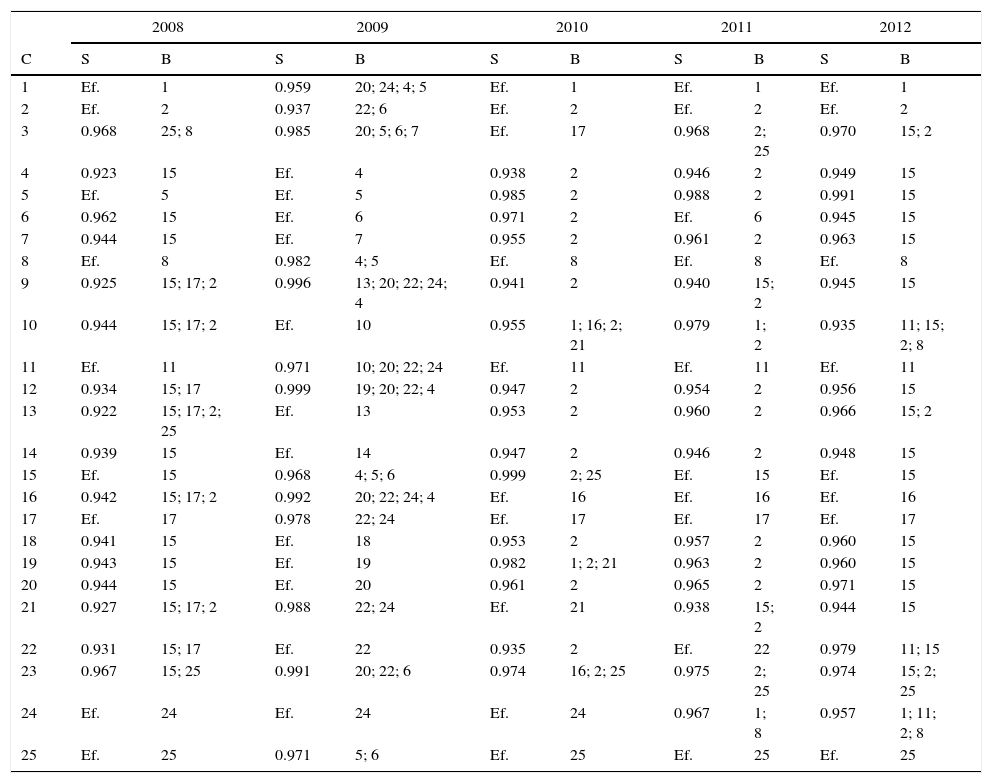

As the potential to a general comparison between the cooperatives, the Data Envelopment Analysis was conducted with data from the financial and economic performance, as a way to benchmark the performance. These results can be seen in Table 12.

Cooperatives’ efficiency measured by DEA.

| 2008 | 2009 | 2010 | 2011 | 2012 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| C | S | B | S | B | S | B | S | B | S | B |

| 1 | Ef. | 1 | 0.959 | 20; 24; 4; 5 | Ef. | 1 | Ef. | 1 | Ef. | 1 |

| 2 | Ef. | 2 | 0.937 | 22; 6 | Ef. | 2 | Ef. | 2 | Ef. | 2 |

| 3 | 0.968 | 25; 8 | 0.985 | 20; 5; 6; 7 | Ef. | 17 | 0.968 | 2; 25 | 0.970 | 15; 2 |

| 4 | 0.923 | 15 | Ef. | 4 | 0.938 | 2 | 0.946 | 2 | 0.949 | 15 |

| 5 | Ef. | 5 | Ef. | 5 | 0.985 | 2 | 0.988 | 2 | 0.991 | 15 |

| 6 | 0.962 | 15 | Ef. | 6 | 0.971 | 2 | Ef. | 6 | 0.945 | 15 |

| 7 | 0.944 | 15 | Ef. | 7 | 0.955 | 2 | 0.961 | 2 | 0.963 | 15 |

| 8 | Ef. | 8 | 0.982 | 4; 5 | Ef. | 8 | Ef. | 8 | Ef. | 8 |

| 9 | 0.925 | 15; 17; 2 | 0.996 | 13; 20; 22; 24; 4 | 0.941 | 2 | 0.940 | 15; 2 | 0.945 | 15 |

| 10 | 0.944 | 15; 17; 2 | Ef. | 10 | 0.955 | 1; 16; 2; 21 | 0.979 | 1; 2 | 0.935 | 11; 15; 2; 8 |

| 11 | Ef. | 11 | 0.971 | 10; 20; 22; 24 | Ef. | 11 | Ef. | 11 | Ef. | 11 |

| 12 | 0.934 | 15; 17 | 0.999 | 19; 20; 22; 4 | 0.947 | 2 | 0.954 | 2 | 0.956 | 15 |

| 13 | 0.922 | 15; 17; 2; 25 | Ef. | 13 | 0.953 | 2 | 0.960 | 2 | 0.966 | 15; 2 |

| 14 | 0.939 | 15 | Ef. | 14 | 0.947 | 2 | 0.946 | 2 | 0.948 | 15 |

| 15 | Ef. | 15 | 0.968 | 4; 5; 6 | 0.999 | 2; 25 | Ef. | 15 | Ef. | 15 |

| 16 | 0.942 | 15; 17; 2 | 0.992 | 20; 22; 24; 4 | Ef. | 16 | Ef. | 16 | Ef. | 16 |

| 17 | Ef. | 17 | 0.978 | 22; 24 | Ef. | 17 | Ef. | 17 | Ef. | 17 |

| 18 | 0.941 | 15 | Ef. | 18 | 0.953 | 2 | 0.957 | 2 | 0.960 | 15 |

| 19 | 0.943 | 15 | Ef. | 19 | 0.982 | 1; 2; 21 | 0.963 | 2 | 0.960 | 15 |

| 20 | 0.944 | 15 | Ef. | 20 | 0.961 | 2 | 0.965 | 2 | 0.971 | 15 |

| 21 | 0.927 | 15; 17; 2 | 0.988 | 22; 24 | Ef. | 21 | 0.938 | 15; 2 | 0.944 | 15 |

| 22 | 0.931 | 15; 17 | Ef. | 22 | 0.935 | 2 | Ef. | 22 | 0.979 | 11; 15 |

| 23 | 0.967 | 15; 25 | 0.991 | 20; 22; 6 | 0.974 | 16; 2; 25 | 0.975 | 2; 25 | 0.974 | 15; 2; 25 |

| 24 | Ef. | 24 | Ef. | 24 | Ef. | 24 | 0.967 | 1; 8 | 0.957 | 1; 11; 2; 8 |

| 25 | Ef. | 25 | 0.971 | 5; 6 | Ef. | 25 | Ef. | 25 | Ef. | 25 |

C=cooperative; S=score, B=benchmark; Ef.=efficient.

By means of DEA's analysis, one can see that no cooperative was found efficient in the 5 years. Just to mention, six cooperatives were efficient in 4 of the 5 years under analysis: Sicoob Credicitrus, Sicred Cocred, Crediamo, Sicredi Coopecredi, Sicoob Credicoonai and Unicred João Pessoa. In addition, three cooperatives – Uniprime Norte do Paraná, Sicredi Serrana RS and Sicoob Maxicrédito – were efficient in 3 of the 5 years of the study. Moreover, Sicredi Vanguarda PR, Sicredi União RS and Unicred Florianópolis were not considered efficient in either of the periods studied.

However, it can be seen that all cooperatives have obtained efficiency scores close to 100%. In 2008 and 2012, Uniprime Norte do Paraná stood out. It was considered a 15 times benchmark for other cooperatives in 2008; in 2012, 16 times. In 2010 and 2011, Sicoob Cocred stood out and was a 15 times benchmark for other cooperatives in 2010; 14 times, in 2011. In 2009, Sicredi Norte RS/SC was considered a benchmark for 8 cooperatives.

Thus, the units regarded as effective in the model actually require some modifications. Thus, the improvement of analysis helps to understand and distinguish the really efficient units and display units that serve as the benchmark for others (including those taken initially as efficient).

Note also that these results confirm the individual results of each indicator. The cooperatives were efficient. The cooperatives more often considered benchmark for the others were those with a more conservative view. These cooperatives had lower impairment of its assets and equity with their risky activities.

Concluding remarksThe aim of this study was to analyze the economic and financial performance of the largest Brazilian credit cooperatives. The performance, measured on the financial statements, can be used as part of the process of credit analysis (Altman, 1969). This also allows verifying the financial and economic performance of credit activities within credit cooperatives: temporally, in the same cooperative; transversally, among the cooperatives.

Based on the analysis of the indicators highlighted by the CAMEL model, it can be seen that there is a positive relationship between the use of the CAMEL model variables and the measurement of the financial and economic performance of the credit cooperatives. The indexes computed by the financial and economic indicators allow the analysis of performance to occur, regarding the indexes’ increase or decrease. Thus, the expected result would consider two aspects: the first would show that the higher the rates of the economic and financial performance of CAMEL model, the higher the performance addressed to the capacity for growth in loans activity to the associate clients; the second would indicate that the greater the gap in the capital growth indicator the greater the loan capacity dispensed to associate clients (Hartwick, 1977; Meyer & Pifer, 1970; Sinkey, 1975).

Increase in financial and economic performance provides an augmentation in the availability of resources within the cooperatives. This results in the indicators’ elasticity and represents capital growth, which also allows an increase in the ability to provide resources to the associate members (Dzeawuni & Tanko, 2008).

The results show that Uniprime Norte do Paraná, Sicoob Cocred and Sicredi Norte RS/SC were the cooperatives standing out as efficient. They have also worked as benchmarks for the largest number of inefficient cooperatives. The results also confirm a more conservative position from the part of these cooperatives, since they have not risked the capital of their associate members.

It was, throughout this research, which did not exist intend to exhaust the subject, nor the use of all possible tests, however, the use of methods and models chosen may represent a limiting fact. A possible limitation from the point of view of the research choices, was the establishment of the CAMEL model, the possibility of use with variables obtained in the publications of credit unions, as of the balance sheet, the income statement of the surplus or loss report administration and some time, sites of cooperatives, can be limiting if considered other methodologies or models for evaluating financial performance.

As the research's potential limitation one can point out data obtaining from the cooperatives. Such a dependence on data limits the number of indicators of the CAMEL model in the analysis. As recommendations for future studies on the same environment, one can apply other methodologies for the assessment of the financial and economic performance. One available is PEARLS model (Protection, Effective Financial Structure, Asset Quality, Rates of Return and Costs, Liquidity, Signs of Growth).

Peer Review under the responsibility of Universidad Nacional Autónoma de México.