The effects of government R&D subsidies can vary across recipient firms, depending on the various characteristics of a firm, potentially including the firm's accounting information quality (AIQ). It has been well recognized that high AIQ helps to reduce information asymmetry between investors and firms and, consequently, improves investment efficiency. However, there is a lack of clear understanding about the specific role of corporate accounting information in the ex-post effectiveness of government R&D subsidies. This study thus examines the main effects of government R&D subsidies on both firms’ R&D inputs and innovation outputs, and the positive moderating role played by the quality of corporate accounting information. The data include 1,561 sample firms listed in the stock markets in China and 11,853 firm-year observations between 2007 and 2015. We find that the moderating effect of AIQ is economically sizable where an improved AIQ (discretionary accruals), by a standard deviation, increases the additionality effect by 16% for corporate R&D investment and 4% for the growth of firms’ R&D inputs. In addition, we find the subsidies have a stronger favorable effect on firms’ R&D outputs (the number of patents) for those firms with a higher AIQ.

Governments are important players in fostering and promoting firms’ innovations (Aghmiuni, Siyal, Wang, & Duan, 2020; Shu, Wang, Gao, & Liu, 2015; Zhang & Nuttall, 2011). Governments may develop policies to support innovations in general or target a specific type of new technology to achieve the objectives of public interest, for example, to develop and adopt green innovations for sustainability (Huang, Liao, & Li, 2019; Sun, Liu, Wang, & Yuan, 2019). There are various forms of support that governments can provide, for example, incentive policies or financial schemes such as R&D subsidies. The policy of R&D subsidy explicitly aims to encourage firms to undertake R&D activities that are expected to benefit the whole society. One key challenge for the government is to identify the right recipient firms. Supporting the wrong firms may result in the subsidy being wasted (e.g., substitute existing private R&D) or, even worse, crowd out private R&D (Dimos & Pugh, 2016).

Scholars have attempted to examine the effectiveness of government R&D subsidy schemes; however, the empirical evidence so far remains inconclusive, with scholars reporting positive, negative, and mixed effects of such schemes (Ahn, Lee, & Mortara, 2020; Bellucci, Pennacchio, & Zazzaro, 2019; Wu, Yang, & Tan, 2020; Yi, Murphree, Meng, & Li, 2021). The majority of the studies document the positive effects that government subsidies stimulate firms’ R&D activities. Some studies report a crowding-out effect where recipients substitute government funds for corporate investment in R&D (Dimos & Pugh, 2016), while other studies report no such crowding-out effect (Martin, 2016). Empirical evidence so far shows that the effects of government R&D subsidies can vary across industries (Hong, Feng, Wu, & Wang, 2016). Firm-level studies indicate that the success of R&D subsidy schemes depends on various characteristics of the firm such as corporate ownership structure (Wu, 2017) and size (Bianchi, Murtinu, & Scalera, 2019). What is little known, however, is the role of firms’ accounting information in the ex-post effectiveness of R&D subsidies, despite the fact that accounting information quality (AIQ) is well recognized to play a critical role in capital investment (Chen, Hope, Li, & Wang, 2011; Hope, Thomas, & Vyas, 2017) and the implementing of innovations (Ilg, 2019).

This study thus aims to narrow the research gap by investigating the role played by accounting information in the effects of R&D subsidies on the recipient firms’ R&D performance in terms of both innovation inputs and outputs. The main research question is “what is the role of accounting information in the effect of the government's R&D subsidy schemes on firms’ R&D input and innovation performance?”

We selected China as the field context studying this topic, which is timely and important for three reasons. First, the Chinese government plays a powerful role in supporting technological innovations and the country is expected to surpass the U.S. to be the largest R&D contributor in the near future (Abbas, Avdic, Peng, Hasan, & Ming, 2019; Amankwah-Amoah et al., 2021; Boeing, 2016; Guo, Guo, & Jiang, 2018; Wu et al., 2020; Zhao, Xu, & Zhang, 2018; Zhu, Zhao, & Abbas, 2020). Second, the usefulness of accounting information in emerging markets such as China has long been questioned, as it is of relatively low quality, compared with that in developed economies (Song, 2016). Third, the government in China may less be incentivized than private investors to collect private information from subsidized firms, while the outcomes of R&D activities are inherently uncertain (Hall, 2005). The data of this study were collected from multiple sources that cover 1561 firms listed in the stock markets in China, including 11,853 firm-year observations between 2007 and 2015.

The study provides fresh contributions to the product innovation literature by: (a) offering evidence to support the positive effects of both government's R&D innovation inputs and outputs, and (b) revealing whether and how accounting information plays a role in the success of the government's R&D subsidy schemes. Specifically, our evidence shows that the performance of government R&D subsidies in China is dependent on the AIQ of the subsidized companies in terms of both R&D inputs (self-funded R&D investment and its growth) and innovation outputs (the number of patents obtained) in that the subsidies have a greater effect for firms with a higher AIQ. The study findings offer both policy and managerial implications for the government as well as firms applying for government R&D subsidies. For the government, it should note that firm-level governance quality is the micro-basis for the success of a public policy. In addition to the technical and market indicators, the government must scrutinize firms’ accounting behaviors when implementing a public funding policy aiming at supporting private companies. Accounting information is important in the screening process by determining how much effective information applicants provide. For firms willing to apply for government funding, they should create and maintain a good governance system, strive to improve their AIQ, and control any moral hazard problem, to increase the chance of being funded and maximize the innovation outputs.

Literature reviewThe effects of R&D subsidiesInnovation has been widely accepted as one of the driving forces of corporate success and long-term economic growth. However, R&D activities may be under-invested due to the problem of asymmetric information (Hall, 2005) and limited access to external finance (Rajan & Zingales, 2001). Therefore, to promote corporate innovation activities, governments provide support for firms to mitigate the risk of market failure (Hong et al., 2016).

The main rationale of such a policy is to address market inefficiency, specifically the underinvestment of private funds in R&D activities (Arrow, 1972), because of the nature of R&D, which involves three major issues (Link & Scott, 2013). First, there are positive externalities, which refer to the situation that the benefits of a firm's R&D can be spilled over to its competitors fairly easily (Haskel & Westlake, 2018); as a result, the investing firm cannot fully capture the potential return on its R&D investment. Consequently, the market investment in R&D as a whole will become less than socially desirable. Second, there is information asymmetry between the firm and its financers, which could lead to problems of moral hazard and adverse selection (Bakker, 2013), creating barriers for the firm from accessing commercial funding. Third, the R&D activity inherently involves uncertainty and risk, from technical, strategic, and market to profit aspects, which increase the difficulty and costs of private financing (Bakker, 2013). To address these issues, it is important that governments provide support for private R&D investment.

Successful public support should enable recipients to increase investment in innovation (Cin, Kim, & Vonortas, 2017; Lach, 2002), resulting in lower costs of innovation and better access to external finance (Takalo, Tanayama, & Toivanen, 2013). R&D subsidies are an input-driven policy for supporting firms’ innovation capacity, reducing the costs of R&D, improving market success rate (Dimos & Pugh, 2016; Guo, Zou, Zhang, Bo, & Li, 2020), and increasing margin (Chen & Xu, 2021). First of all, R&D subsidies can help the firm reduce the investment risk in R&D, allowing the firm greater flexibility in leveraging the financial resources to explore and exploit new opportunities from the R&D endeavors (Gao, Hu, Liu, & Zhang, 2021).

Secondly, there is an additionality effect, i.e., the subsidies motivate the firm to increase R&D investment from their own resources (Guo et al., 2020). Moreover, R&D subsidies create signaling effects (Wu, 2017), attenuating the information asymmetry problem, helping the subsidy recipient firm to gain access to external funding (Yan & Li, 2018), and to attract collaborations from both academic and corporate partners (Bianchi et al., 2019). Strategic collaboration is particularly encouraged for promoting knowledge transfer in the high-tech sector and, consequently, innovation performance (Abbas, Avdic, Xiaobao, Zhao, & Chong, 2018; Zhao, Jiang, Peng, & Hong, 2020). Recently, Ahn et al. (2020) have provided evidence that government subsidy helps alleviate R&D externalities’ concern for business. They find that increased innovation collaborations were statistically significant between the recipients of R&D subsidies, confirming the role of such subsidies in stimulating firm collaboration and reducing market inefficiency.

Different effects can occur simultaneously (Ahn et al., 2020). Ultimately, it is expected that recipient firms have more resources to commercialize their innovations and, consequently, improve the outputs of their R&D and overall firm performance (Guo et al., 2020). Nevertheless, not all R&D subsidies achieve their desired effects. A well-documented negative effect is crowding-out, i.e., the recipient firms use the grants to replace their own R&D investments, undermining the expected additionality effect (Gao et al., 2021; Marino, Lhuillery, Parrotta, & Sala, 2016).

Empirical studies have suggested that the effects of subsidies vary across industries or firms, signifying that there are moderating variables in the effectiveness of the policy Hong et al. (2016). suggest the subsidies have positive effects on innovations in some industries, but negative effects in others. Bianchi et al. (2019) find that R&D subsidies’ effect on technological partnership is stronger for smaller than larger firms. Examination of heterogeneity in firm characteristics is important for understanding the differences in the outcome of a public policy (Dimos & Pugh, 2016) Gao et al. (2021). suggest that central R&D schemes are not as effective as local ones in facilitating firm innovation. However, the extant literature seems to have neglected the role played by the accounting information, which could potentially moderate the ex-post effectiveness of government subsidies.

The role of accounting informationCorporate accounting information is known to play a pricing function in determining the costs of external finance and stock prices (Christensen, Nikolaev, & Wittenberg-Moerman, 2016), while it also has a governance function, which receives less attention in the literature. The governance function refers to its role in alleviating information asymmetries and restraining the opportunistic behavior of the management team (Zhai & Wang, 2016). In China, the governance role is particularly important where the acceptance of R&D subsidies is viewed as the course of a contract between the supplier (i.e., government) and the recipient firm.

According to the contracting theory in accounting (Lambert, 2001; Sunder & Cyert, 1997), accounting information plays a key role in determining the contractual mechanism. On one hand, by alleviating the problem of asymmetric information, the provision of high AIQ facilitates the fulfillment of contracts. On the other hand, high AIQ also alleviates the problem of adverse selection by reducing the costs of information collection so that a contract could be reached at lower costs. The economic consequences of providing high AIQ have been widely documented in terms of its favorable effects on reducing the cost of capital (Chen & Zhu, 2013; Hsieh, Shiu, & Chang, 2019) and debt agency costs (Billett, King, & Mayer, 2007), improving access to loans (Kim & Yasuda, 2019; Palazuelos, Crespo, & del Corte, 2018), investment efficiency (Chen et al., 2011; Hidayat & Mardijuwono, 2021) and reducing bid-ask spreads (Zhou, 2007).

The AIQ is important for the success of an R&D subsidy, because corporate R&D activities carry the nature of uncertainties and information opaqueness, while the government may lack strong incentives to scrutinize private information possessed by applicant firms. Due to such an asymmetric information problem, it is difficult for policymakers to assess the effectiveness of public policies (Butler, 2012). At a micro-level, the critical question is whether the government has the ability to identify the right R&D projects that private firms are reluctant to fund but those projects have the potential to generate high social returns. However, government authorities often face an information disadvantage that comes from the uncertainties of R&D projects, such as the variation of project returns over time (David, 2011) and the difficulty of measuring social returns (Hubbard, 2011). Information disadvantage could increase the risk of adverse selection in grants distribution and, consequently, result in government failure in subsidy policy implementation.

Studies have shown that Chinese government subsidy decisions are more reliant on ‘hard’ corporate information (e.g., assets and R&D investment) than the quality of financial and accounting information (Lee, Walker, & Zeng, 2014) Chen, Wang, Hu, and Zhou (2020). find government even uses some external indicators, such as whether a firm is listed on both Shanghai and Hong Kong Stock Markets, as an information agent to make a subsidy decision. Their empirical results show that the firms targeted by the Shanghai-Hong Kong Stock Connect are more likely to receive R&D subsidies from the government. This indicates that there are severe information asymmetry problems between government and subsidy applicants. The application for R&D subsidies could be taken as a self-selection behavior at the firm level to reduce risks and the cost of financing R&D activities (Takalo et al., 2013). In an attempt to obtain a larger subsidy, business managers tend to exaggerate their demand for R&D investment and to engage in earnings management in the application process. Opportunistic business managers are likely to provide incomplete or even distorted accounting information if the AIQ is not taken into consideration in the process of allocating public R&D subsidies. Moreover, public choice theory (Butler, 2012) suggests that government may also take opportunistic actions to prioritize certain firms, give credit to their agency managers, and gain a short-term reputation for the ‘effectiveness’ of its programs.

Potential moderation effect of accounting informationThe importance of accounting information has been well captured in theoretical frameworks, such as the theory of incomplete contract to help information users make more informed decisions (Christensen et al., 2016). Empirical evidence from China has shown that accounting information exerts a significant favorable effect on the efficiency of resource allocation with capital flowing to the best industries (Zhai & Wang, 2016). Based on the data of Spanish small and medium enterprises (SMEs), Palazuelos et al. (2018) show that AIQ is an important factor for firms to access external loans. Based on the data of Japanese SMEs, Kim and Yasuda (2019) reveal that accounting information is effectively used in the guaranteed loans screening process, highlighting the importance of AIQ for firms. Furthermore, Hsieh et al. (2019) indicate that AIQ helps firms to reduce the cost of capital Hidayat and Mardijuwono (2021). examine the effect of AIQ on investment efficiency on Indonesian manufacturing firms and find that those with high AIQ are associated with high efficiency of investment decisions and performance.

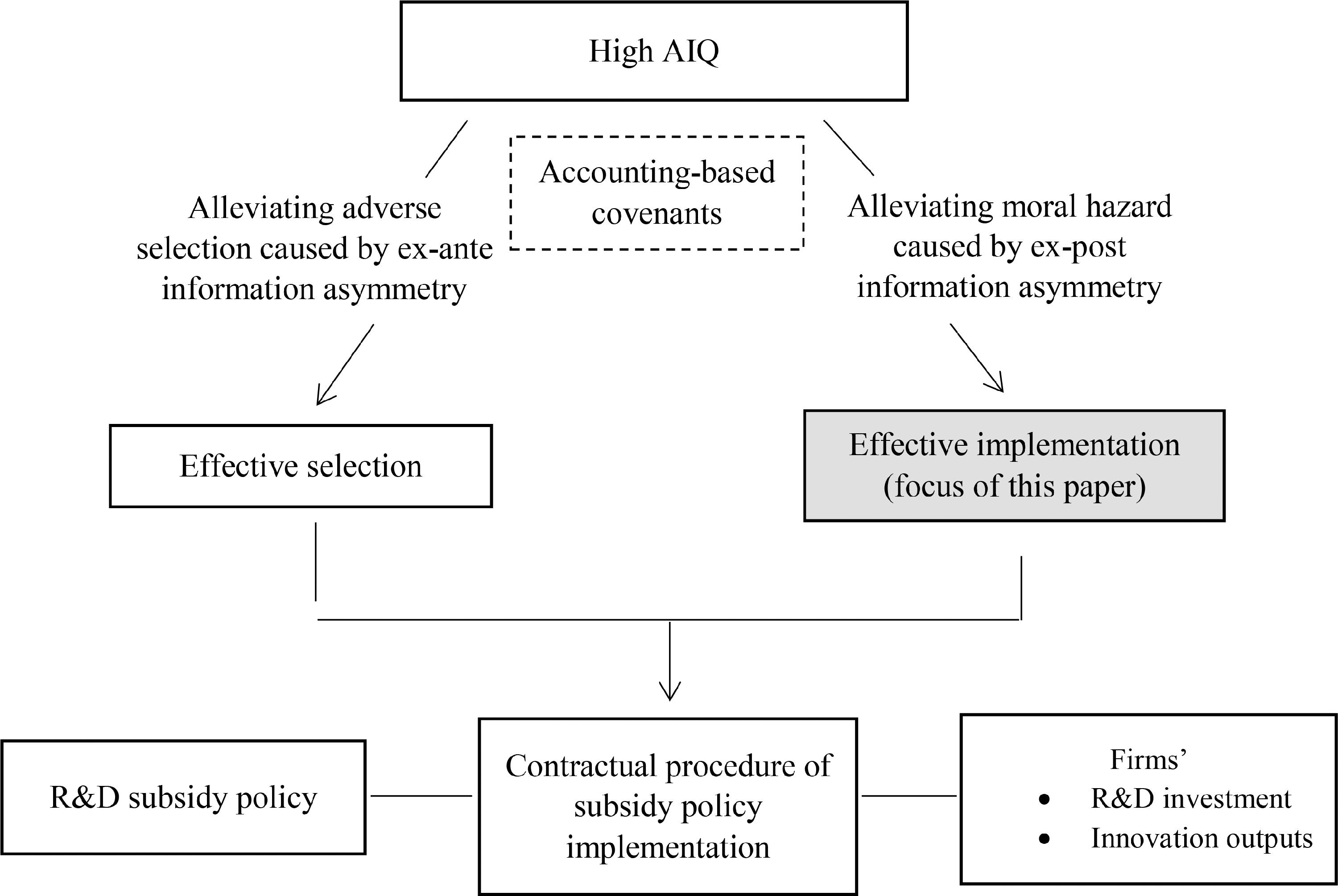

A reasonable conjecture would be that accounting information helps to enhance R&D subsidy effectiveness via both effective selection and effective implementation (Fig. 1). On one hand, by reducing the chance of adverse selection due to the ex-ante information asymmetry, high AIQ improves the effectiveness of subsidy selection (Dimos & Pugh, 2016). On the other hand, high AIQ alleviates the moral hazard problem caused by ex-post information asymmetries in financing R&D activities. The implementation effectiveness of subsidy covenants is subject to the problem of the moral hazard of subsidy recipients, due to agency conflicts in corporate governance mechanisms and contract incompletion, such as the possibility of misusing or deferred use of subsidized funds. For example, recipient firms may shirk, transfer subsidies to other usages, or reduce their own R&D investment. Improved AIQ could reduce the possibility of subsidy recipients taking such actions and, hence, the moral hazard problem is alleviated.

Based on these above-mentioned two mechanisms, we posit that R&D subsidy recipients with a higher AIQ would have a stronger self-funded R&D investment motivation and better R&D outputs. Our rationales are threefold. First, high AIQ signals a good governance mechanism, which reduces the likelihood of the subsidy being diverted to activities other than those agreed (Dimos & Pugh, 2016). Second, high AIQ is verifiable, which serves as an effective measuring tool and enhances the willingness of interested parties to monitor the implementation of a subsidy contract (Hope et al., 2017). Third, high AIQ is transparent, which may increase the government's effective information load and enables the government to dynamically monitor contractual performance.

MethodsData and sampleWe collect relevant financial data and basic information of firms from the database of China Stock Market & Accounting Research (CSMAR) for all listed firms in China, including firms in the Growth Enterprise Board (GEM), Small and Medium Enterprise (SME) Board, and the Mainboard between 2007 and 2015. CSMAR is widely used in the literature as the data source of Chinese listed company research (e.g., Kwak, Chang, & Jin, 2021; Tian, Kou, & Zhang, 2020; Zhang, Wang, & Chen, 2021), which collects, codes and cleans all listed companies’ financial and operational activity information from their compulsory or voluntary disclosures. We capture the effectiveness of government R&D subsidies based on both the input (e.g., stimulating further R&D investment by recipient firms) and output (e.g., the number of patents obtained) of R&D investment. We exclude non-subsidized firm samples1 for the following reasons. First, the allocation of subsidies has been widely examined (e.g., Boeing, 2016). Second, existing empirical materials do not allow us to apply a two-stage approach to examine both subsidy allocation and effectiveness. This is because, on one hand, allocation error may exist, and some applicants were mistakenly rejected. On the other, the current empirical data do not allow us to make a distinction between rejected non-subsidized firms or non-applicant firms. Third, subsidized firms and non-subsidized firms may have different accounting practices and pooling the samples may generate selection bias.We hand-collect R&D subsidy and patent information of sample firms from WIND, which is the most popular data service platform for investors in China that provides a wide range of detailed information useful for investment decisions, including detailed financial, operational information of firms, macro-economic data, government policy, and other business-related news. It has also been used as a data source in literature for case studies and other studies that require in-depth information about firms (e.g., Ali, Qiang, & Ashraf, 2018; Duan & Jin, 2014; Yang, Orzes, Jia, & Chen, 2021). WIND collects information about the detailed subsidy items a company has received from the government for any reason. We exclude subsidies that are not related to an R&D purpose, identified by keywords in the subsidy item description, and then summarize the R&D-related subsidy value to firm-year panel data. WIND also collects companies’ innovation-related information, such as patent applications and grants, research spending, and so on. Following Daim, Monalisa, Dash, and Brown (2007) and Lahr and Mina (2016), we choose the number of patents granted in a year as the R&D output. To fully capture the effects of R&D subsidies on corporate R&D performance, we exclude samples with information less than two years, industries with little R&D investment and sample firms without R&D activities or R&D subsidies2. Overall, we have 1561 sample firms and 11,853 firm-year observations.

VariablesEffectiveness of government R&D subsidiesWe measure the effectiveness of R&D subsidies by both R&D input (the firm's self-funded R&D investment) after the subsidies were received in the main tests and the output (the number of patents) in the robustness tests. We follow previous studies (e.g., Lach, 2002) and define R&D input as the amount of self-funded R&D investments (= total R&D investment – R&D subsidies) standardized by revenue.

Accounting information qualityWe measure the AIQ primarily by discretionary accruals, DA (Kothari, Leone, & Wasley, 2005) but deflated by revenue to DArr and then transfer it to one-way measurement, DArrN, in the main tests, and financial restatement (Clinton, Pinello, & Skaife, 2014), restate, in the robustness tests. Financial restatement (restate) is coded as 1 if a sample firm amended its financial statements in a specific year; 0 otherwise.

We construct the measure of DArrN as follows:

First, we follow the model suggested by Kothari et al. (2005) to calculate discretionary accruals (DA) as the product of the estimated residual (εt) of the following equation multiplies the deflator (At-1):

where TAt is the total accruals in year t, At-1 is the asset value in year t-1, ΔREVt is the difference of revenues between year t and year t-1, ΔARt is the yearly change in accounts receivable between year t and year t-1, PPEt is the value of fixed assets in year t andROAt−1 is the return on assets in year t-1. We estimated Eq (1) by year and industry, then the error term (εt) multiplies the deflator (At-1) is the scale of discretionary accruals (DA) in year t.

Second, DArrt, the degree of discretionary accruals, is then defined as the discretionary accruals standardized by revenue in year t to make it more comparable across sample firms with different sizes. Finally, we use DArrNt (=1-|DArrt|) as a comparable one-way measure of the degree of discretionary accruals. By taking the absolute value of DArrt, both negative and positive discretionary accruals are treated equally as a deviation from the optimal quality (DArrt=0). DArrNt, which is 1 minus the absolute value of accruals, transforming the measure into a nature of ‘the higher the better’, where a sample firm has the best (worst) AIQ when DArrNt = 1 (0).

Government R&D subsidiesThe information on R&D subsidies is reported as supplementary information in financial statements and we hand-collect such information from all listed firms. We follow Lach (2002), measuring the R&D subsidies (SUBrr) using a revenue-standardized value of the R&D subsidies received by the sample firm.

Control variablesWe control for both firm and market-level heterogeneity. First, we control for the corporate financial position, including the debt ratio (DR............) and cash holding (cashR), given that R&D investment is heavily dependent on the corporate financial position and lower debt ratio and higher cash holding position would enable the firm to have greater financial resources to invest in R&D. Second, the effectiveness of R&D subsidies varies depending on the ownership structure of companies (Wu, 2017) and, hence, we control for corporate governance by state-ownership (SOE), management shareholding (Rmgm), dual-role (CEO), shareholding balance (Bshr), and controlling shareholding (Rctrl). We expect that better-governed firms would pursue long-term development by increasing R&D investment. Third, we use asset value (LnAsset), industry classification (ind), technological asset ratio (techAsset), sales growth rate (saleG) and gross profit margin (margin) to control other heterogeneities of the sample firms. We expect that firms with a larger size, greater technological intensity, greater profit margin and lower sales growth would have a stronger motivation to invest in R&D. We define the variables in Table A2.

Data analysisAfter eliminating data-missing observations, our data consist of 1561 observations over nine years with the nature of an unbalanced panel. To explicitly consider the nature of the sustainability of R&D investment, we include a one-year lagged R&D measure as an explanatory variable. Due to the lagged effects of R&D subsidies and the possible endogeneity where the government could be more likely to subsidize firms with more self-funded R&D investment, we use lagged value in the empirical models following David, Hall, and Toole (2000), and we employe a dynamic panel data approach, a two-step system GMM estimate method clustered with robust standard errors, as recommended by Blundell and Bond (1998):

where R&D activities are measured by either input (self-funded R&D investment and its growth) or output (new patents obtained each year) and the estimate β4 in Eq(3) captures the moderating effect of AIQ on the effectiveness of R&D subsidies on corporate R&D activities. Control variables include all available measures of the sample firm's heterogeneity, like financial performance, corporate governance, industry, location and other attributions. ui is the individual fixed effect. To control for the outlier effects, we winsorize continuous variables at a 1% level from both tails. In System GMM, we use lagged first differences of RDrr and SUBrr as instruments, and the individual effect is eliminated by first differencing in the GMM estimation.ResultsDescriptive statistics

As presented in Table 1, corporate self-funded R&D investment3 accounted for about 2.9% of revenue on average and increased by 0.5% annually. Total R&D investment, including government subsidies, was about 3.1% of total revenue and, on average, sample firms received an amount equivalent to 0.2% revenue from the government as R&D subsidies. In terms of R&D output, on average, the sample firms acquired 69 patents annually. The sample firms had discretionary accruals at -0.3% of revenue and 20% of the sample firms amended their financial statements.

Descriptive statistics.

At the firm level, a typical sample firm in our data had a debt ratio of 43%, a cash holding of 18%, a 0.3% growth rate on revenue, and a 26% gross profit margin. In terms of corporate governance, 37.9% of our samples were state-owned enterprises (SOE), 75% of CEOs played a dual role as board directors and the management team held an average of 13.2% ownership.

Subsidies’ additionality effect on firms’ R&D performanceWe commenced our analysis by a baseline model without the interaction term in Eq. (2) and measured the R&D activities by both the value and growth, i.e., self-funded R&D investment (RDrr) and its growth (△RDrr). As Table 2 shows, the self-funded R&D investment in year t was positively associated with R&D subsidies in year t-1 (Model 1) and the incremental R&D investment was also driven by the increasing R&D subsidies a sample firm received from the government (Model 2). Specifically, by controlling for revenue at a constant, every CNY1,000 (ca. USD150) R&D subsidy could encourage sample firms to invest CNY490 (ca. USD73.5) by self-funding per annum and per CNY1,000 increases in government subsidy would stimulate an additional self-funded R&D investment by CNY367 (ca. USD55). Such a result provides evidence of the additionality created by government R&D subsidies, indicating that government R&D subsidy has a positive effect on firms’ R&D investment.

Effects of governmental subsidies on firm R&D investment performance.

Notes: Standard errors in parentheses.

***

** and * denotes significant level at 1%, 5% and 10% respectively. The decrease of observation amount is due to the time lag.

The results also support the model specification where the insignificant AR2 shows that the error terms have no serial correlation. The insignificant Hansen test also ensures the validity of the instruments and confirms that over-identification issues did not exist in the estimations. Additionally, our baseline results show that firm-level characteristics could affect corporate R&D investment which increases over management shareholding, balance shareholding, cash holding, technological asset ratio and profitability margin and decreases with debt ratio and sales growth. There is evidence that state-owned enterprises had a slightly higher propensity to undertake corporate R&D investment.

Similarly, we find governmental subsidies have an additional effect on firms’ R&D output. Due to the lagged effects of R&D investment (input) on patents (output), we considered the effects of lagged R&D investment for two years (t-1 and t-2) for both corporate investment (RDrr) and government subsidies (SUBrr). The results are reported in Table 3, which show that the lagged effect did exist, and corporate R&D investment and governmental subsidy in t-2 have positive impacts on patent obtaining, indicating that government R&D subsidy has a positive effect on firms’ innovation outputs.

Effects of governmental subsidies on firm R&D output performance.

We employ a system GMM approach and include an interaction term to capture the moderating effects of accounting information quality as shown by Eq. (3). The significant positive coefficients of interaction terms as shown in Table 4 suggest that the favorable effects of R&D subsidies were positively associated with the AIQ of the subsidy recipient. Meanwhile, the coefficients of subsidy (SUBrr) and its growth (△SUBrr) were no longer significant, which indicates that the effect of the subsidy on corporate R&D investment performance depended heavily on the AIQ of the sample firm. Quantitatively, an improvement of AIQ (DarrN) by one standard deviation (0.155) increases the additionality of the subsidies by about 16% (=1.044 × 0.155) in Model 1 for the value of self-funded R&D investment and about 4% in Model 2 for the growth of corporate R&D investment. In other words, AIQ significantly moderates the effect of government R&D subsidy on firms’ R&D investment.

Moderating effect of AIQ on governmental subsidies’ impact on firm R&D investment performance.

Notes: Standard errors in parentheses; ***, ** and * denotes significant level at 1%, 5% and 10% respectively. We also include control variables and the industry, year and geography effects in all models and the results are not reported but available on request from the authors. The same in following tables.

The test results reported in Table 5 show that AIQ significantly moderates the effect of government R&D subsidy on firms’ R&D output.

Moderating effect of AIQ on governmental subsidies’ impact on firm R&D output performance.

Standard errors in parentheses.

* p < 0.1.

** p < 0.05.

*** p < 0.01.

We test the robustness of our earlier results by using different empirical approaches and measures. First, instead of using interaction terms, we categorize the samples into groups with low and high AIQ, i.e., samples with greater or lower discretionary accruals than average and samples with or without financial restatement, respectively. More specifically, samples with greater (lower) discretionary accruals and with (without) financial restatement would have low (high) AIQ and, therefore, the favorable effects of R&D subsidies in Table 2 would be weaker (stronger) Table 6. presents the results by using a grouping approach and shows that our earlier results are robust. Similar to the above test, we considered the effects of R&D subsidy (SUBrr) and its growth (△SUBrr) on both the quantity (RDrr) and the growth (△RDrr) of self-funded R&D investment of the sample firms Table 6. and Table 7 show that the favorable effects of R&D subsidies were only statistically significant in those sample groups with high AIQ and such effects were insignificant for those firms with low-AIQ.

Robustness test on R&D investment performance – an alternative empirical approach (group regression).

Notes: ***, ** and * denotes significant level at 1%, 5% and 10% respectively.

Robustness test on R&D output performance – an alternative empirical approach (group regression).

Further, we use the occurrence of financial re-statement as an alternative measure of AIQ, and run a robustness test again. A sample firm is defined as having high AIQ if it does not have a financial re-statement (restate=0); low AIQ otherwise. The results are reported in Tables 8 and 9.

Robustness test on R&D investment performance – an alternative measurement of AIQ.

Robustness test on R&D output performance– an alternative measurement of AIQ.

| Dependent variable | lnPatent | △lnPatent | |||

|---|---|---|---|---|---|

| Group | Restate=0 | Restate=1 | Restate=0 | Restate=1 | |

| lnPatent t-1 | 0.960⁎⁎⁎(0.025) | 0.899⁎⁎⁎(0.043) | -0.039(0.025) | -0.103⁎⁎(0.043) | |

| RDrr t-1 | -0.069(0.669) | -1.848(1.806) | 0.116(0.652) | -1.753(1.730) | |

| RDrr t-2 | 1.729⁎⁎(0.815) | 2.590(1.883) | 1.621⁎⁎(0.800) | 2.721(1.844) | |

| SUBrr t-1 | -1.393(4.231) | 6.065(5.738) | |||

| SUBrr t-2 | 4.423⁎⁎(3.058) | 7.484(9.682) | |||

| △SUBrr t-1 | -5.126(4.449) | 10.676(8.370) | |||

| △SUBrr t-2 | 2.682*(4.002) | 12.211(7.408) | |||

| Constant | -5.803⁎⁎⁎(0.509) | -5.826⁎⁎⁎(0.940) | -5.745⁎⁎⁎(0.509) | -5.713⁎⁎⁎(0.935) | |

| Control variables | Yes | Yes | Yes | Yes | |

| AR2 p value | 0.437 | 0.616 | 0.443 | 0.796 | |

| Hansen test | 74.116 | 23.777 | 74.107 | 23.349 | |

| Hansen p value | 0.674 | 0.371 | 0.560 | 0.241 | |

| Number of Obs | 5860 | 2614 | 5859 | 1612 | |

Standard errors in parentheses.

Prior research on government R&D subsidies has examined the roles played by various firm characteristics in the effectiveness of the policy while neglecting the role of corporate accounting information. In this study, we attempt to narrow this gap by focusing on firm heterogeneity in AIQ. We argue that accounting information plays a governance function in the course of contract implementation between the subsidy supplier (government) and recipients (innovative companies) by alleviating the problems of ex-post moral hazard. This study, thus, examines the main effects of government R&D subsidies on both firms’ R&D inputs and innovation outputs, and the positive moderating role played by the quality of corporate accounting information. This is one of the first studies to test the moderating effects of accounting information on the effectiveness of government R&D subsidies. The study provides fresh empirical evidence on the effectiveness of public R&D subsidies in terms of both corporate R&D input and output.

The results of our study show clear evidence that government R&D subsidy has a positive effect on both firms’ R&D investment and innovation outputs, and the AIQ plays a moderating role in the effectiveness of government R&D subsidies. Specifically, we found that recipient firms with higher AIQ had greater self-funded R&D investment and greater R&D outputs in terms of the number of patents obtained. Such a moderating effect is economically sizable where an improved AIQ (e.g., discretionary accruals) by a standard deviation would increase the additional effect of R&D subsidies by 16% for corporate R&D investment and up to 4% for its growth. In addition, R&D output (e.g., patent) by recipient firms with high AIQ also benefits more from government subsidies.

Theoretical implicationsThe study extends the literature on government innovation policy by investigating the effectiveness of government R&D subsidies and the role played by accounting information. Our contributions are twofold. First, the study results help to clarify the inconsistent findings regarding the effectiveness of R&D subsidies (Bellucci et al., 2019; Yi et al., 2021). Our results provide support for the idea that government R&D subsidies can effectively promote innovations in the country in terms of both inputs and outputs (Ahn et al., 2020; Wu et al., 2020). However, unlike Ahn et al. (2020) who focus on the subsidies’ effect on inter-firm collaboration, and Wu et al. (2020) who focus on the subsidies’ role in increasing the chance of being further funded by venture capital, thus boosting the overall investment in renewable energy, we examine the direct effect of both R&D inputs and innovation outputs. Our findings confirm the additionality effects of government R&D subsidies, which are consistent with findings in a provincial survey conducted by Zhai and Wang (2016), which show a positive relation between subsidy amount and the numbers of employees carrying out R&D functions in a firm.

Second, this is the first study to investigate AIQ as a moderator on the effects of R&D subsidy on both innovation inputs and outputs. The findings of this study thus advance our understanding of the mechanism in government R&D subsidy efficiency, by highlighting that the production of high AIQ serves as a governance function for recipients to implement subsidy-related covenants. The study results are in line with the financial investment literature, which suggests that high AIQ helps to alleviate information asymmetries and moral hazards (Lambert, 2001; Sunder & Cyert, 1997), restrain the opportunistic behavior of the management (Dimos & Pugh, 2016; Zhai & Wang, 2016), facilitate contract fulfillment (Hope et al., 2017), access to credit (Kim & Yasuda, 2019; Palazuelos et al., 2018), reduce the cost of capital (Chen & Zhu, 2013; Hsieh et al., 2019) and improve investment efficiency (Chen et al., 2011; Hidayat & Mardijuwono, 2021). However, unlike those financial studies, this study offers the first empirical evidence on whether and how AIQ strengthens the effectiveness of the government's innovation policy.

The study's finding of AIQ's moderation effect implies that firms with higher AIQ will be less opportunistic, i.e., commit more effort to make better use of the subsidy. This is in line with the literature in investment and corporate governance studies. For instance, Chen et al. (2011) find that firms with a higher quality of financial reporting have less incentive to minimize earnings for tax purposes, a sort of earnings management opportunity Elliott, Fanning, and Peecher (2020). find that investors ascribe value to firms that use higher financial reporting quality because they perceive higher financial reporting quality as cooperative behavior, signaling that the firms are more credible. Our results extend the function of AIQ to the information asymmetry problem in the government subsidy context, helping explain the R&D performance inconsistency of subsidy recipients. For example, the studies of Bellucci et al. (2019) using Italy data, and Yi et al. (2021) using China data, both find different, even conflicting, performance results among the subsidy recipients that are similar in location, business, and other aspects.

Practical implicationsThe findings of this study offer several important policy implications for China and other countries with similar government R&D support programs. Our results suggest that the governing bodies in those countries should place more emphasis on accounting information when screening or monitoring subsidy recipients. First, accounting information is essential in the screening process by determining how much effective information applicants provide. Second, the AIQ reflects the effectiveness of the recipient's corporate governance in controlling the moral hazard problem. As shown in this study, firm-level governance quality is the micro-basis for the effectiveness of a public policy; thus, besides the technical and market indicators, it is crucial that authorities scrutinize firms’ accounting behaviors when implementing or assessing public funding policy aiming at supporting private companies. For firms that intend to apply for government R&D subsidies, they should devote effort to improving their governance system, thus raising the level of AIQ, to enhance their potential of being funded and, consequently, achieve better innovation outputs.

Limitations and future researchThis study does not examine the role of firms’ accounting information in the selection process when government allocates R&D subsidies (i.e., effective selection, Fig. 1), due to data limitation. Future research could investigate such effects and additional determinants of the effectiveness of government R&D subsidies. In addition, future research could examine the impact of subsidies on unsubsidized firms because these firms may increase their R&D activities in response, in order to maintain their competitiveness.

This work was partly supported by Soft Science Research Project of Guangdong Province in China [Grant No.: 2019B101001018]

Initially, our raw data include information about all listed companies in the China A-share market, i.e., 3345 firms in 16,321 observations. We exclude those firms from the financial sector and other sectors seldom with R&D activities. These excluded sectors are agriculture, utility, wholesale and retailing, hotel and restaurant, finance, real estate, leasing and service, consultancy, household service, education, and culture. Hereafter, we eliminate observations with missing values. Finally, our sample includes 2041 firms and 12,414 observations, consisting of a group of 1561 firms that received R&D subsidy at least once and a group of 480 firms that never received R&D subsidy. In other words, we use all available samples of China's listed firms in R&D intensive sectors.

Number and proportion (%) of observations with R&D activities across industry.

Variable definition.

Additional t-tests show that our subsidized observations have similar values in most key variables with full samples but non-subsidized samples show different firm-level characteristics from full samples. Therefore, we find little evidence on sample selection bias by excluding non-subsidized observations. Our key results still hold by including those non-subsidized observations.

We define a sector having little R&D as those industries which have less than 10% observations taking R&D activities. Please see Table A1 for more detailed information. We exclude such sectors for two reasons. First, we follow existing literature (e.g. Yuan, Hou, & Chen, 2015) to focus on those sectors which government R&D subsiding programs have mainly targeted. Second, we exclude such sectors to minimize extreme value effects. Additional tests by including such sectors were performed and the results are available on request from the authors.

There is a total number of 726 (less than 7% of total) observations with negative self-funded R&D investment (RDrr), referring to the sample firms which did not self-fund R&D investment and did not fully use government R&D subsidies. Negative self R&D investment (total R&D less than subsidies) does not necessarily mean that such firms use R&D subsidies for other purposes. Such firms may not fully invest in R&D in a particular year and would delay the investment in the following years. In such cases, the government does not usually force them to return the money unspent.