Green product innovations offer a large number of compelling benefits to different stakeholders throughout their life cycle (raw material extraction, production, use and maintenance, end of life). However, in inert sectors such as the construction industry, the development of green products is still too slow to meet future needs. To push green innovation, this article investigates the application of a virtuous circle in the construction industry. Additionally, the potential of green product innovations to generate and sustain economic growth is analyzed. Finally, barriers and practical implications for a green construction industry are presented.

The qualitative study is based on a literature review, 25 expert interviews, and three case studies of green leaders. Results indicate that a virtuous circle is possible and has the potential to change the construction industry. Moreover, green product innovations strengthen efficiency and core competences. However, high perceived initial costs, outdated accounting methods, and the complexity of construction projects are identified as main barriers to implementation. These barriers can be counteracted by 1) increased awareness among consumers and institutional investors, 2) collaboration and knowledge transfer between stakeholders, and 3) a pull-effect of green leaders who communicate the financial and environmental benefits of green projects. The results support the resource dependence theory and demonstrate the relevance of the external environment on companies.

The built environment is a long-standing hotspot of resource use and environmental impacts. The construction industry is one of the largest sectors in terms of contributions to greenhouse gas emissions in the United States (Truitt, 2009) and one of the heaviest consumers of natural resources (USGBC, 2012). Thus, the building and construction sector has a large potential to contribute to the achievement of future sustainable development (UN, 2015). As environmental topics related to resource efficiency and low energy become increasingly pertinent, current construction methods and products must adapt (Kibert, 2016). Unlike other industrial sectors, construction has historically failed to generate and sustain economic growth through innovation (Murphy, Perera, & Heaney, 2015). This is mainly due to high cost pressures (Loforte Ribeiro, 2009) and the long-term characteristic of projects, including high uncertainties (Ilg, Scope, Muench, & Guenther, 2017).

Literature overviews discussing the benefits and barriers of a green construction industry currently exist (Häkkinen & Belloni, 2011; Zuo & Zhao, 2014). However, they fail to draw conclusions on the business actors and companies that plan and build such projects. Additionally, little is known about the role of new materials and products on the greening process. Finally, no connection has been made between the greening process and corporate financial performance (CFP). However, all these aspects are vital for the transition to a green construction industry.

The aim of the article is threefold. First, it investigates how a sustainable virtuous circle (Glass, 1996) capable of turning the construction industry into a leading green sector could be created. Second, the importance of product innovation is analyzed (Cheng, Chang, & Li, 2013). Finally, the article aims to investigate barriers and other factors that impede, delay, or completely block the greening process (Mirow, Hoelzle, & Gemuenden, 2008). Moreover, practical implications and best practices are presented on how to overcome these barriers. The research bases on a literature review, 25 expert interviews with planners and developers, and three in-depth case studies with green business leaders. The research questions created to identify the transition mechanisms to a green development and its impacts are as follows:

- 1.

What does a virtuous circle for a green construction industry look like?

- 2.

How does green product innovation (GPI) influence the virtuous circle?

- 3.

Which barriers hinder the greening process in an inert environment and how might these barriers be overcome?

The findings will guide construction companies in the greening process and demonstrate how to optimize their innovation processes to generate positive, long-term corporate environmental and financial performance (Menguc & Ozanne, 2005). Apart from the value added for corporate management, these findings help governments to approve regulations and certification schemes that encourage green development in the construction industry. Business science is provided with an in-depth understanding of the relationship between business (construction industry), GPI, and CFP.

The paper is structured as follows. First, an overview of the applied theories is provided in “Theoretical Background”. Afterwards, the used methods are explained. The following section presents the results, including the virtuous circle. The identified barriers are analyzed in “Barriers connected to a green construction industry”, followed by practical implications to overcome them. The next section entails the three case studies. The final section concludes the findings and provides an overview of future research.

Theoretical backgroundIn this article, the relation between GPI and a greening process of an inert industry is analyzed with the concept of a virtuous circle. The greening process is quantified by the number and quality of green real estate projects. Similar to UNEP (2012) or USGBC (2015a), green real estate projects are understood as projects that are more durable, more energy efficient, nontoxic, easier to deconstruct and recycle, and have a much smaller environmental footprint than conventional homes, while remaining economically profitable.

The resource dependency theory (RDT) is used as a theoretical background in this article as it analyzes the organization within its environment, focusing on the organization's uncertainty reduction and its interfirm relationships. The two main pillars of the theory state that 1) organizations are open systems that continuously exchange material and information with their environment, and 2) their survival depends on the resource exchange with the environment (Pfeffer & Salancik, 1978). Tashman (2011) extended that theory and added the biophysical sphere to the external environment, allowing RDT to investigate the direct relationship between organizations and the natural environment (Bergmann, Stechemesser, & Guenther, 2016).

As the influence of the environment on corporations is complex, a virtuous circle is appropriate to analyze that topic and its connection to GPI (Glass, 1996). Similarly, the concept of virtuous circles was applied by Orlitzky (2005), who detects a positive correlation between social performance and financial performance, suggesting the relation forms a virtuous circle. Additionally, innovation and the influence of regions on greening the economy can lead to a virtuous circle (Antonioli, Borghesi, & Mazzanti, 2014), as well as competition within a sector (Castaño, Méndez, & Galindo, 2016), or innovation, economic growth, and entrepreneurship (Galindo & Méndez, 2014). Finally, a virtuous circle in the construction industry is discussed by Brady, Davies and Gann (2005), who conducted research on private finance initiatives. However, these articles do not combine product innovation and greening within an industry to create a virtuous circle, nor are barriers and conditions discussed that are essential to starting that circle.

A strategically managed GPI starts and steers the virtuous circle (Lai, Lin, & Wang, 2015). GPIs are goods or services which are new or significantly improved (OECD, 2005) and have a lower environmental impact than their predecessors. The importance of market orientation and firm innovativeness, and the moderating effect of managerial attitudes of top managers toward the natural environmental, has been shown by Dibrell (2011).

As some authors argue that learning from mistakes motivates learning more than success (Eisenhardt & Martin, 2000), barriers in this non-linear system are identified in order to provide recommendations on how to initiate the virtuous circle and foster organizational learning. Therefore, the EOI model (external environment, organization, and individual barriers) by Hueske, Endrikat, and Guenther (2015) is applied to identify potential barriers.

MethodThe article is based on a literature review, focusing on the creation of a virtuous circle and GPI in the construction industry. The review considers existing virtuous circles from innovation and greening (e.g. Guenther & Hoppe, 2014). Subsequently, a more sophisticated circle is developed.

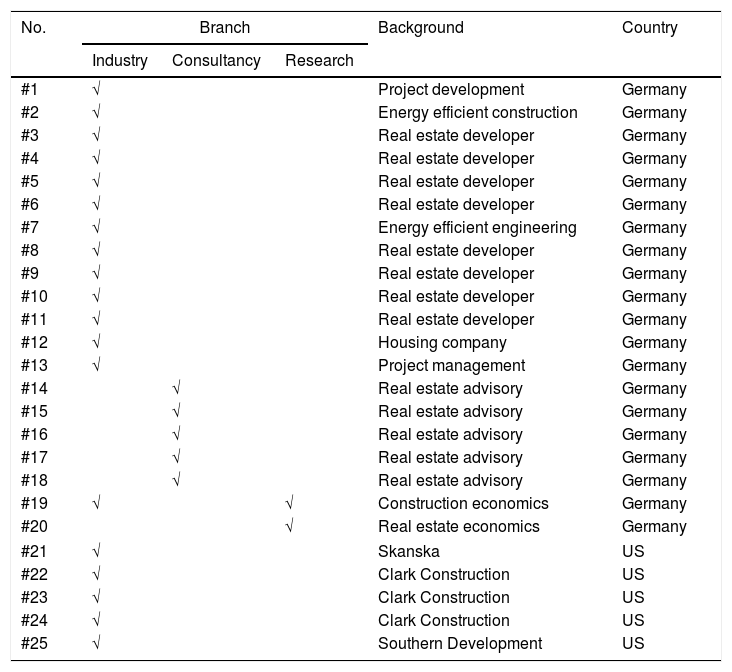

Secondly, the designed circle was assessed by practitioners and scientists. The experts were selected from the construction and real estate industry by theoretical sampling (Eisenhardt, 1989; Sandelowski, 1995). Interview requests were sent to the ten largest real estate developers, the largest consulting companies, and real estate academics in Germany. Germany was chosen as it serves as a forerunner in certifying green building. Theoretical saturation (Sandelowski, 1995) was reached after 20 interviews. The sample was supplemented by a representative of an investor-driven organization (interviewee #26) and an architect committed to green building (interviewee #27). An overview of the interviewees is provided in Table 1. Interviews were conducted from October 2016 to February 2017 via telephone or in person.

Overview of experts.

| No. | Branch | Background | Country | ||

|---|---|---|---|---|---|

| Industry | Consultancy | Research | |||

| #1 | √ | Project development | Germany | ||

| #2 | √ | Energy efficient construction | Germany | ||

| #3 | √ | Real estate developer | Germany | ||

| #4 | √ | Real estate developer | Germany | ||

| #5 | √ | Real estate developer | Germany | ||

| #6 | √ | Real estate developer | Germany | ||

| #7 | √ | Energy efficient engineering | Germany | ||

| #8 | √ | Real estate developer | Germany | ||

| #9 | √ | Real estate developer | Germany | ||

| #10 | √ | Real estate developer | Germany | ||

| #11 | √ | Real estate developer | Germany | ||

| #12 | √ | Housing company | Germany | ||

| #13 | √ | Project management | Germany | ||

| #14 | √ | Real estate advisory | Germany | ||

| #15 | √ | Real estate advisory | Germany | ||

| #16 | √ | Real estate advisory | Germany | ||

| #17 | √ | Real estate advisory | Germany | ||

| #18 | √ | Real estate advisory | Germany | ||

| #19 | √ | √ | Construction economics | Germany | |

| #20 | √ | Real estate economics | Germany | ||

| #21 | √ | Skanska | US | ||

| #22 | √ | Clark Construction | US | ||

| #23 | √ | Clark Construction | US | ||

| #24 | √ | Clark Construction | US | ||

| #25 | √ | Southern Development | US | ||

Note: More specific descriptions of expert backgrounds are not shown to ensure anonymity.

All interviews had an average length of 30–40min. The interviews were conducted on the basis of a semi-structured interview guide (see Appendices 1 and 2). The definition of green construction, as mentioned in “Theoretical Background”, was provided in order to start on a common basis. After transcribing the audio-recorded interviews, MaxQDA, a software for computer-aided qualitative data analysis, was used to code and analyze the interviews (Mayring, 2014).

Thirdly, the study follows the methodological approach of Olsen, Prenkert, Hoholm, and Harrison (2014) and compiles three case studies to understand the strategic decisions that are necessary to foster GPI. The case study approach offers the possibility to address the dynamic interactions between innovation, greening, and strategy over time (Herrera, 2016). Moreover, the interrelations between innovation, greening, and strategy are rather complex and thus a case study is preferable to quantitative analysis or experiments (Gerring, 2004). The case studies comprise in-depth interviews with senior managers and detailed study of documents and further information provided by the company. The questions asked in the interviews were arranged according to the steps of the virtuous circle and were backed up by theoretical approaches in business economics provided by Lewin (2004).

Results for the virtuous circleGreen and sustainable products have long enjoyed high consumer demand and have become more and more required by governmental regulation. Since 2007, this trend for green projects has been visible in the construction and real estate industry as well (#22; #23). Annual spending on green construction in the US is projected to increase from $150.6 billion in 2015 to $224.4 billion in 2018 (USGBC, 2015b).

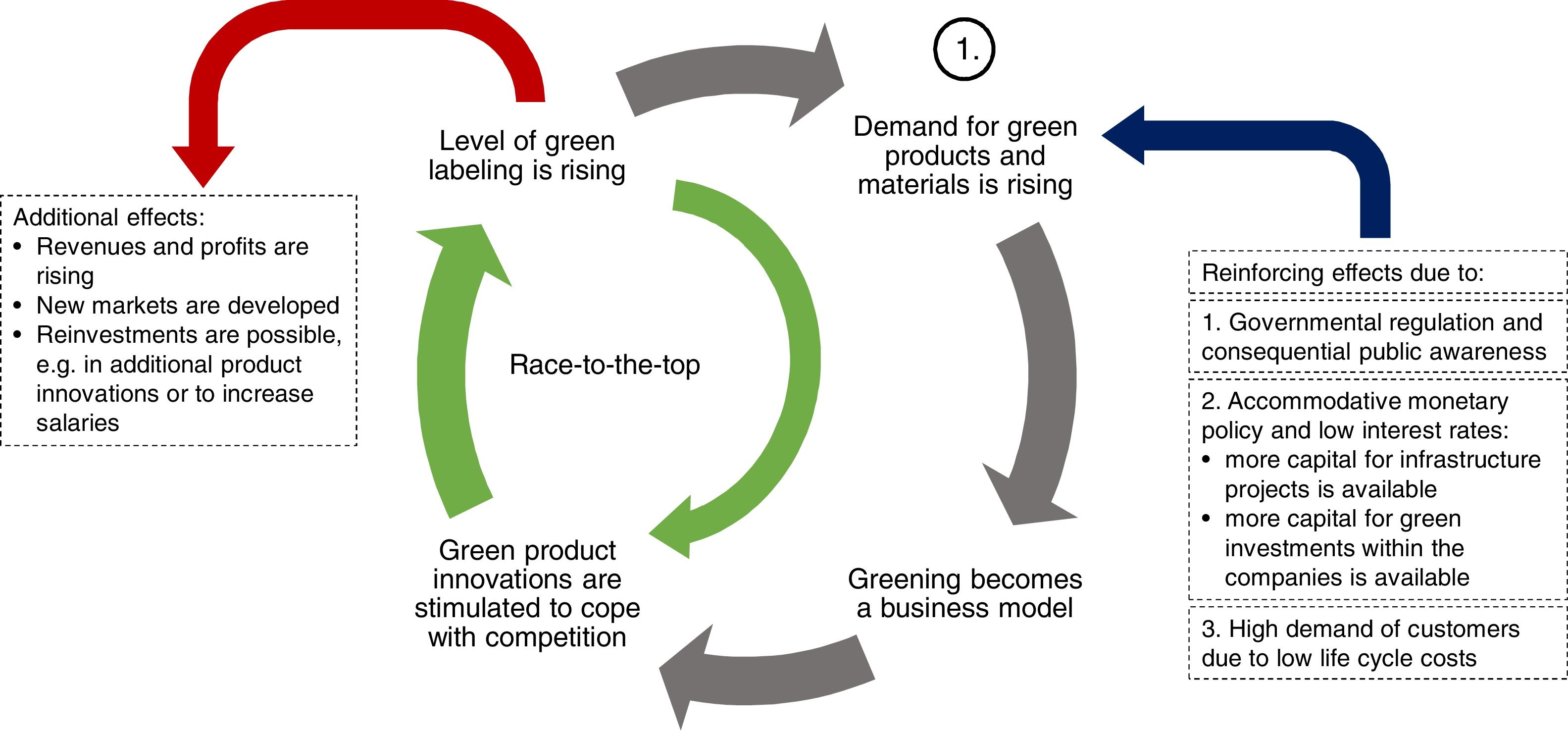

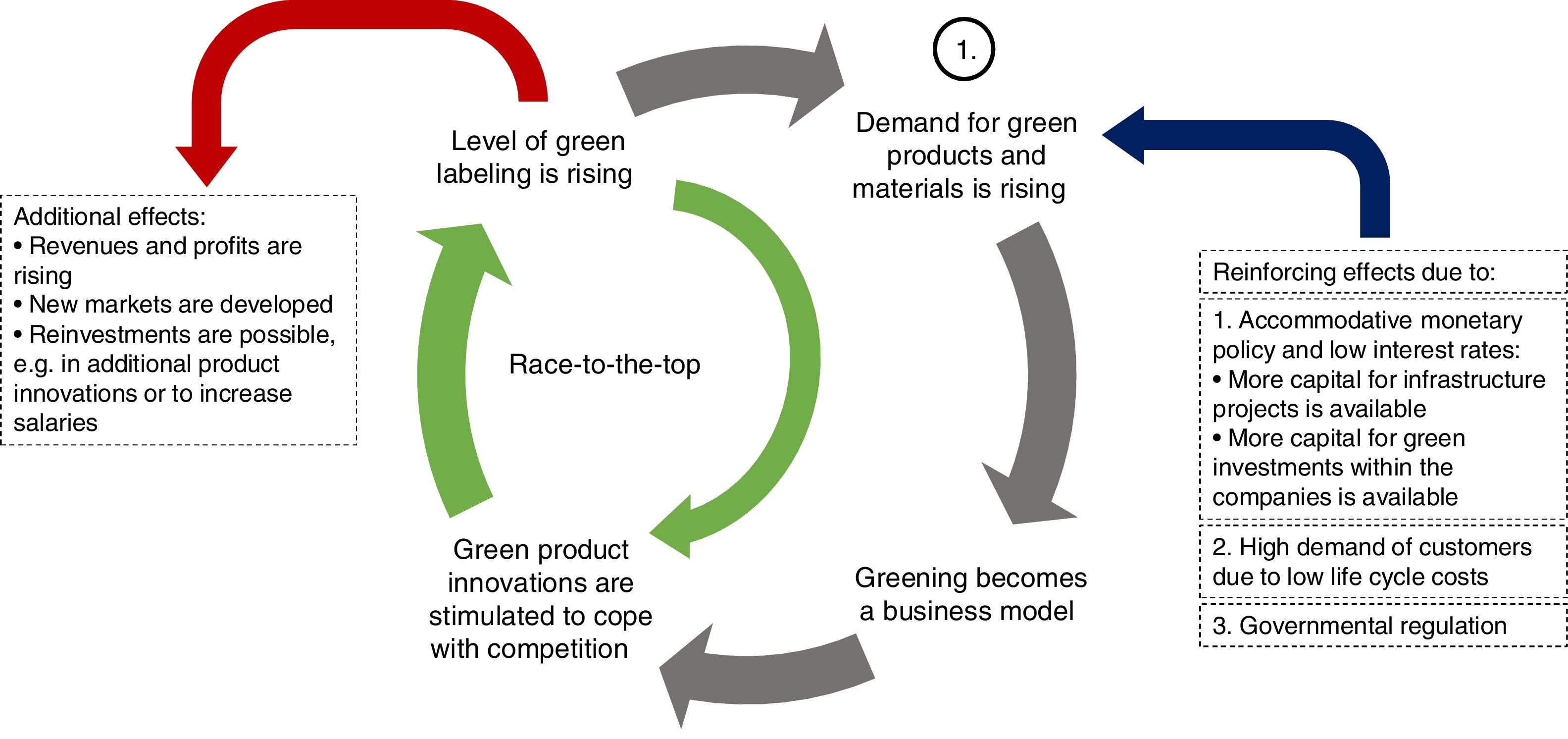

Regardless of recent developments, the real estate industry lags behind the sustainability movements of other business sectors (RREEF, 2010). The construction industry is still known to be among the least innovative industries and most conservative in terms of adaptation of innovation (Xue, Zhang, Yang, & Dai, 2014). Fig. 1 illustrates the designed virtuous circle that accelerates green project development and includes a self-enforcing greening process.

After a short overview of the entire circle, each step is described more in detail and backed up by literature and expert interviews.

Overview of the virtuous circleThe main virtuous circle (gray) for green products in the construction industry starts with a rising demand from customers that is reinforced by the current accommodative monetary policy and stringent governmental regulation (blue). As a result, competition within the sector intensifies and green becomes a business model (Castaño et al., 2016). In order to meet that surge of demand, new product innovations are stimulated. That results in greater efficiency and strengthens core competences. The entire construction industry subsequently greens as the share of green products rises. Similar to other industries, the number of labeling and certification standards multiplies to cope with new products (Harrison, 1999). Stricter government regulations and governmental infrastructure projects reinforce that issue (#25). The last two steps create a virtuous circle themselves and start a race-to-the-top (green). Only companies that incorporate this virtuous circle and invest in greener products will benefit from the circle and gain competitive advantage. In the long term, companies that do not adopt this circle will be pushed out of the market (Tatum, 1987). There are additional benefits not directly intended by the companies (red), such as higher revenues and profits due to larger market shares and the entrance to new markets. Finally, reinvestment in new product developments and payouts are the last part of the circle (Galindo & Méndez, 2014). Experts (e.g. #21; #25) agreed that the circle applies to the real estate industry in general, but fits best to the premium office market (#26; #27).

Demand for green products is risingThe rising demand for green materials and products can be nicely described by the “Push and Pull Model”. On one side, demand-pull derives from enlightened consumers who appreciate lower life cycle costs (#12; #13; #18; #22; #25). On the other side, consumer demand influences the direction and rate of technological development and leads to a technology push by suppliers (#4, #8). The push is fostered by stricter governmental green real estate regulation (ASBC, 2016; Morgan Stanley, 2016; USGBC, 2015a) based on international climate treaties and resource efficiency programs (BD&C, 2003; #28). This trend is supported by a survey of Dodge Data & Analytics (2016), where the importance of environmental regulations for green buildings jumped from 25% in 2008 to 35% in 2015.

The top trigger for green materials in absolute numbers for 2015 is client demand (40%). Client demand is highly connected to stakeholder expectations, either because they are clients or they benefit from high client demand (Morgan Stanley, 2016; #6; #8). Nowadays, clients not only want to feel better, but they are also aware that green buildings improve work performance (#4) and reduce operating costs (ASBC, 2016; #9). Moreover, green becomes more important as a marketing and reputational issue (#2; #4; #8; #12; #13; #22; #23).

The most acknowledged economic benefits are higher property values, lower vacancy, a rent premium, and higher productivity (#15). Among others, Eichholtz, Kok, and Quigley (2013) showed that green buildings have higher rental and occupancy rates (3–9%) than similar office buildings. However, some experts doubt these points (BD&C, 2006; #19). This might change in a down market where the demand for new flats and houses is low (#27). Other experts doubt that an increase in green real estate is based on an accommodative monetary policy for low and medium price housing (#3; #4; #5; #6; #10; #11; #16; #20), while others confirm a connection (#7; #27), with some only in refurbishment of existing buildings (#15). For high quality homes, an effect is more likely (#3; #12). Several experts confirmed that green construction outperforms conventional construction during economic crises (#6; #8; #9; #13; #20). Notwithstanding, investors, developers, and clients should keep in mind that a building without green certification might be outclassed by other properties at some time in the future (#7; #14; #15). Thus, some investors already ask for certificates (#13; #16; #21). Projects without certificates will have more problems getting financed by institutional investors (#8; #27; #25).

Ecological benefits increase the demand for green buildings as well, mainly because ecological benefits have a direct impact on the financial bottom line. For example, energy use can drop between 25 and 30%, water around 11%, and greenhouse gases can be lowered by 34% (USGBC, 2012).

Health and well-being of occupants (78%), indoor air quality (78%), employee productivity (74%), and satisfaction of employees and occupants (71%) are the most important non-financial factors (Turner Co, 2014). Moreover, it has been proven that employees in Leadership in Energy and Environmental Design (LEED) buildings show lower absenteeism and less sick leave (BD&C, 2006; UNEP, 2012). For investors and developers, social factors are important as they affect economic aspects. Tenant well-being and satisfaction are directly connected to turnover rates, letting and selling prospects, as well as the risk of losing the tenant (BD&C, 2006). A final social factor is the regional job market. ASBC (2016) expects that green construction will support more than 3.3 million jobs in the US by 2018, generating $190.3 billion in labor earnings.

All these benefits foster green construction and its growth rate eventually outpacing that of conventional construction (USGBC, 2015a), moving green projects from a niche market to a business model.

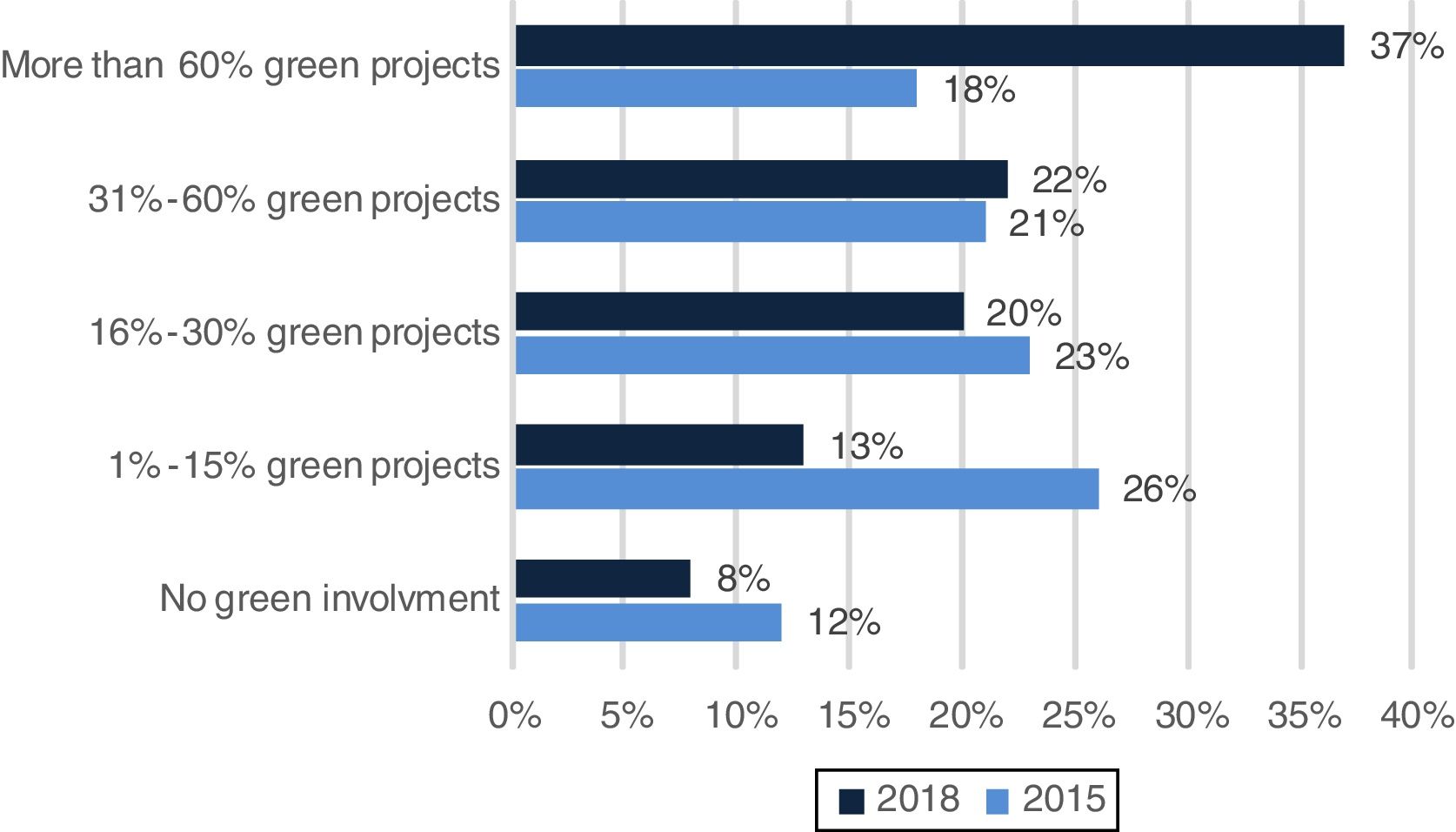

Green becomes a business modelAs a next step in the virtuous circle, green becomes a business model. US residential green construction spending is expected to grow by 24.5% from 2015 to 2018, while commercial green construction spending is estimated to grow by 9.76% at the same time (USGBC, 2015a). Asked about the willingness to participate in this booming market, 37% of executives are expecting more than 60% of their upcoming projects to be green (see Fig. 2). Additionally, most governmental projects in the western hemisphere ask for a certain type of green labeling of the companies and the projects as a prerequisite to participating in the bidding process (#22; #23; #24; #25).

.")

Expected growth in levels of green building activity (DODG, 2016).

One example of a company already using the business model is Turner Construction. They have generated more than half of their revenue (USD 5 billion in 2014) from green infrastructure projects each year since 2009. Another sign that green construction is turning into a business model are the offered products from the finance and insurance sector (BD&C, 2006), including funds being established with the single goal to invest in green buildings.

The importance of GPI for CFPOnce green becomes a business model, it is important for companies and their R&D units to keep up with that trend and foster GPI (#21). That is necessary as successful product and process innovation companies enhance competitiveness (Sexton & Barrett, 2003). In a changing economy, as the construction industry is, the introduction of innovation has been recognized as a central prerequisite to increased growth and productivity (Schmidt, 1995). In the long term, companies that do not adopt the circle will be pushed out of the market. Among others, Choi, Jang, and Hyun (2009) proved a direct and positive relation between innovation and financial performance. Those findings are supported by 61% of corporate leaders who believe that sustainability leads to market differentiation and improved financial performance (USGBC, 2015a).

Additionally, new green products play an important role for smaller construction companies and suppliers (#4; #23). For most executives, the level of a vendor's sustainable practices is very important when choosing a supplier of goods and materials or a service provider (Turner Co, 2014; #21; #22).

The level of green labeling is risingFollowing other industries, the number of labeling and certification standards will rise to cope with new products (Harrison, 1999). For example, the number of LEED-certified projects rose from 2009 to 2014 by about 518% (Turner Co, 2014) and was a main driver for companies to join the green building business (#22; #23; #24; #25). At the same time, spending on LEED-certified projects increased tremendously from USD 103 billion in 2012 to USD 288 billion in 2017 (USGBC, 2015a).

The last two steps create a virtuous circle themselves and start a race-to-the-top. Certificates demonstrate global industry best practices and thus prompt decision-makers to foster green real estate projects (DODG, 2016). High green labeling pays off, as higher ratings in certificates and energy efficiency are fully capitalized into rents and asset values (Eichholtz et al., 2013). Certificates are seen as a quality signal indicating who the market leaders are (#3; #16; #22). As long as major developers are convinced by this signal, the popularity of certificates will stay high (#27).

Barriers connected to a green construction industryAfter all steps of the virtuous circle are discussed in more detail, this section concentrates on the barriers that might occur while fostering GPI. Using the model of Hueske et al. (2015), barriers are categorized to external, organizational, and individual factors.

External barriers are mainly determined by third parties and secondary stakeholders. For the greening of the construction industry, three major barriers are identified.

First, the construction industry is project based: Loosely coupled firms, mostly small and medium enterprises, delivering “projects” through partial engagement. The co-development of construction innovation at the project level includes “the government, suppliers of building materials, private capital providers, vendors and distributors, educational institutions, [and] professional and certification bodies” (Davis, Gajendran, Vaughan, & Owi, 2016: 105). Often these various partners do not cooperate enough (Xue et al., 2014). Using RDT, an exchange of information and material takes place; however, the exchange is uncoordinated and important parts are held back to gain competitive advantages. Additionally, innovation has the largest impact if positioned at an early stage. However, for real estate projects, planning and design is often decoupled from the construction phase (Murphy et al., 2015) and the use of green material depends on these actors (#23; #24). Inexperienced owners and buyers find it hard to navigate an opaque marketplace, what results in poor project management, inadequate design processes, and underinvestment in skills development, R&D, and innovation (McKinsey Global Institute, 2017). Moreover, the fragmented characteristic of construction and its high degrees of specialization makes innovation and its controlling more difficult. Product and process innovations have to be managed across organizational boundaries and within networks of interdependent suppliers, customers, and regulatory bodies (#22; #24). These effects are reinforced by changing political structures and regulations or missing support (#1; #5; #10; #17; #19).

Second, the lack of public awareness and information is a further barrier for green real estate projects (#2; #4). A lot of clients are still concerned about the higher risk of green projects (Larsson & Clark, 2000; #22; #23; #24) based on new assembling techniques, higher costs for additional testing (#25), shortage of support during the use phase (#4; #11; #12), and missing performance information (Häkkinen & Belloni, 2011). As a result, misperceptions of higher capital costs and inadequate market values circulate in the media and general public (Bon & Hutchinson, 2000). Deficient knowledge among investors reinforces that effect (RREEF, 2010).

Finally, a major external barrier is the well-known agency problem. Investment costs are defrayed by investors and developers, whereas utility costs are paid by the owners and tenants. Landlords pay for the capital costs of efficiency improvements, while many of the benefits of green buildings accrue to the user of the property (RREEF, 2010). Thus, where property owners pass utility costs on to tenants, they have no incentive to integrate utility cost-saving technologies (Morgan Stanley, 2016; #2; #15).

Organizational barriers are mainly related to strategy, structure, resources, and organizational culture within the firm. First, culture in the construction industry is rather conservative (Xue et al., 2014; #21). Companies and managers are rather risk averse and are usually skeptical about new products and processes (Morgan Stanley, 2016; #15). A major reason for that risk aversion is the large investment sums and low profit margins (#26). Regarding RDT, financial resources are lacking. Mistakes and delays due to missing certification or low technological performance can derail entire projects, and create negative effects for future orders (Häkkinen & Belloni, 2011; #21; #28).

Second, current accounting methods within construction companies result in fewer green real estate projects. As annual budgets do not take account of savings over several years, efficient use and maintenance measures do not pay off. Half of the executives rated the accounting methods as an extremely or very significant obstacle (Turner Co, 2014).

Individual barriers are connected to attitudes of individuals, personal characteristics, and the lack of management support for innovation. Two main barriers were revealed on the individual level.

First, and similar to external barriers, higher perceived construction and first costs are a main hurdle for managers and developers (#21). Second, most managers (56%) argue that payback periods are too long (Turner Co, 2014; #2), although most executives are willing to accept an extended payback period if projects incorporate green features (Turner Co, 2014).

The mentioned barriers on the external, organizational, and internal levels are not written in stone, and adequate solutions do exist for most of them. These are presented in the next section.

Practical implications of fostering a green building industry and starting a virtuous circleSimilar to other industries, barriers of co-development can be solved by stakeholder collaboration and integration, a core concept of RDT. The construction industry has to increase both its collaboration with stakeholders and its absorptive capability. The former allows for the exchange of knowledge about new materials and technologies, while the latter refers to the incorporation of external knowledge for internal use in the organization. This can be achieved by effective information gathering (Veshosky, 1998), knowledge exchange (Xue et al., 2014), better communication and collaborative relationships (Davis et al., 2016), as well as cooperation between corporations and academia. Both aspects are in line with RDT and aim to reduce uncertainty by exchanging materials and information (Pfeffer & Salancik, 1978).

In order to make green real estate projects even more interesting, external effects during the construction and use phases should be internalized by governmental regulation (#26). By that, the biophysical sphere becomes incorporated in the valuation as requested in the NRDT (Tashman, 2011). Moreover, the shifting of certification schemes to more quantitative and intuitive control mechanisms would strengthen public awareness and empower consumers.

Connected to the first aspect, on an organizational level, the integration of planning and design at an early stage is important (BD&C, 2003; #1; #13; #16; #20). In these two stages, most of the economic and environmental impacts are determined. Moreover, the decision to build green has to be made as early as possible (#19; #23). The earlier green aspects are incorporated in the planning, the lower the cost difference between conventional and green building (#19; #20).

As mentioned above, some administrative procedures within companies block the development of green real estate projects. Innovative fiscal arrangements increase the acceptance of green real estate projects and reduce that barrier, e.g. longer pay back periods and the evaluation of individual targets on a project level rather than on an annual basis. Externally, financing arrangements could be recovered through increased rents (Häkkinen & Belloni, 2011) and an agreement between landlord and tenant on how the positive externality of lower operational costs can be internalized by the landlord (RREEF, 2010).

Finally, a comprehensive innovation management system is necessary (#24; #25). That includes feedback loops to control and steer the innovation process within the company, but also innovation management in singular construction projects (Murphy et al., 2015).

On the individual level, managers should encourage team members to visit trainings (BD&C, 2006). Motivated staff might start pilot projects and create spin offs for new divisions (#21). Following that, the power of these “leaders” can be used to shape an innovation culture (Xue et al., 2014) and to document and monitor the implementation of new technology (BD&C, 2003; Murphy et al., 2015).

Finally, and most importantly, strengthening the push and pull factors would provide the most impact. Using real cost data for a broad range of sustainability technologies and design solutions contradicts the assumption of high costs of green real estate projects and demonstrates the significant improvements in technological and environmental performance (#8; #11; #14). Moreover, it is necessary to communicate the life cycle cost (#13), provide live data, e.g. by smart metering (#27), and inform about technological benefits (#9). If large construction companies recognize these benefits, they will use certification schemes. As a result, other companies – competitors and suppliers – will follow as they are pulled by their market power (#26; #27). A reverse effect is also possible. Innovations can be pushed by suppliers. In the Netherlands, one of the most innovative construction sectors, suppliers accounted for about two-thirds of technological innovations (Pries & Doree, 2005). Both effects are in line with RDT as they prove the dependence of companies with their environment (Pfeffer & Salancik, 1978).

If institutional investors are convinced by the financial benefits and the quality improvement, they will accelerate the trend (#13; #27) by demanding certificates for their investments and thus use their financial power to green the real estate sector from a portfolio level (#6; #27).

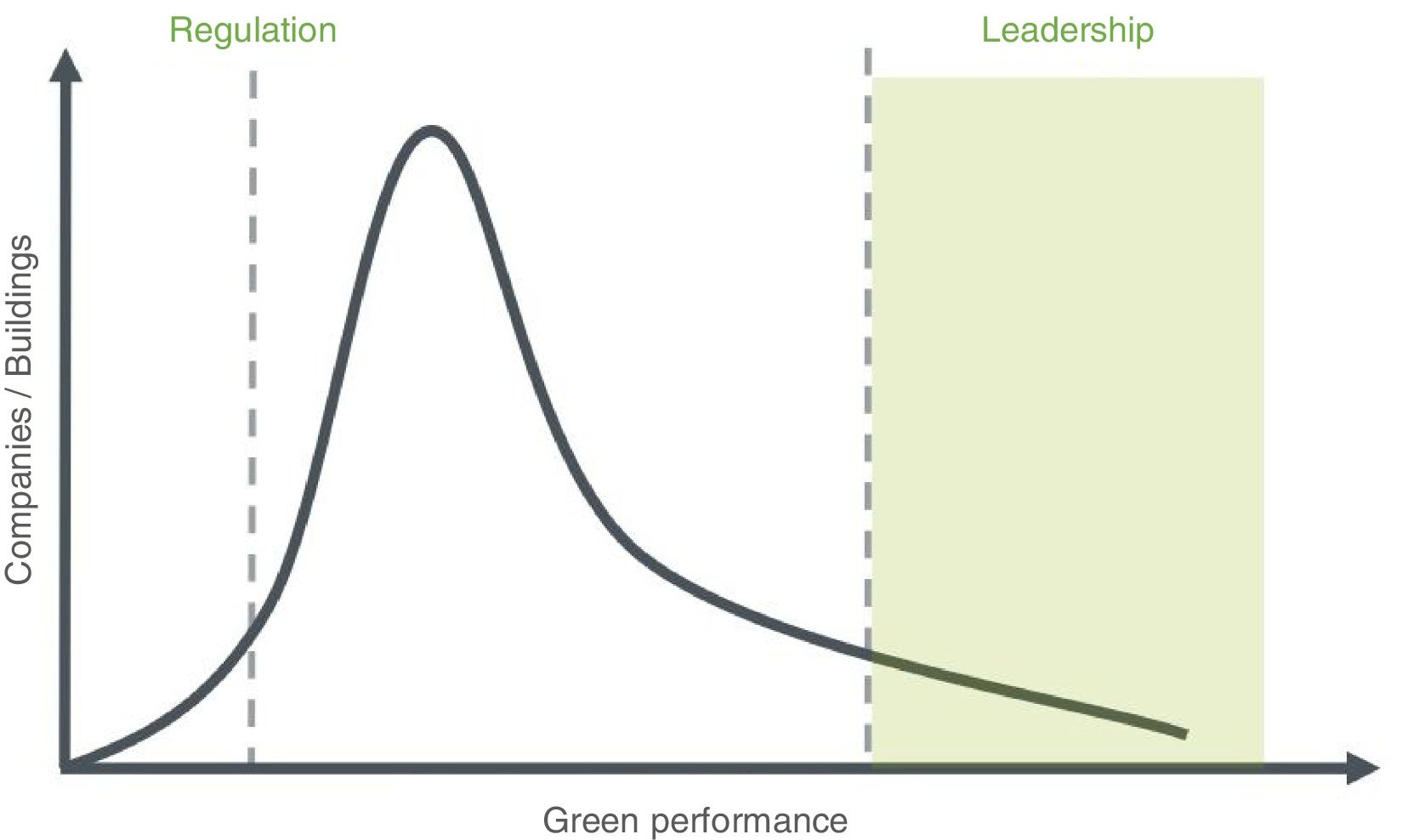

Finally, push factors can be strengthened by stricter regulations and the comprehensive application of green building standards for public projects (#1). As a result, the majority of real estate companies and their projects (peak of the curve in Fig. 3) are pushed by regulation and pulled by the market to the right.

Stimulation of push and pull factors to increase green real estate projects.

Skanska AB, an international development and construction company from Sweden, has been proactive in environmental management since the mid-1990s. The decision of “going green” was made by the former CEO after an environmental incident in 1996. Skanska produced its first environmental report in 1997 and one year later published its environmental policy. By 2000, all its business units were ISO 14001 certified. For its business plan 2011–2015, a set of seven Green Strategic Indicators (GSIs) was agreed upon by the Senior Executive Team. These are translated to regional goals and the progress is presented quarterly by the Business Unit President to the Senior Executive Team. In comparison to other construction companies, responsibilities related to green performance are located on a high management level.

Today there are two reasons why Skanska is increasing its share in green projects: First, the brand is valuable and highly connected to sustainable construction. Skanska is seen as a green leader with an excellent reputation in that market. Second, most of the investors ask for it. The business model concentrates on institutional investors (pension funds) that are interested in long-term benefits. These investors are not only interested in how Skanska creates profit, but also with which projects.

Skanska implements the green strategy through the “Journey to Deep Green”™ and the “Skanska Color Palette”™. Particularly, the second tool indicates Skanska's awareness of visualizing environmental performance and is used in every project as targets are set on the project level and aggregated later. Skanska obliges the internal construction and development units to design and build projects that beat local energy codes by a minimum of 25%. A good example of process innovation at Skanska is its frequent use of building information modeling software tools and radio frequency identification tag technology to eliminate waste and optimize logistics. Moreover, Skanska uses the tools to organize just-in-time delivery, e.g. from specially built off-site construction centers outside of cities. The transformation of innovation from project to corporate level is demonstrated by the use of carbon footprints. Apart from its objective to measure embedded carbon and carbon generated during construction for progressive customers, Skanska uses the information to modify the project and related construction processes in other projects.

Similar to other companies, Skanska recognizes the importance of early green design. They use this opportunity in projects that they develop themselves. Here, Skanska is its own client and can demonstrate what is possible. With that, clients can be convinced more easily for future projects with green benefits. As the cash flow originating from construction is reinvested in Skanska development and construction units, the learning curve is pushed even further. As a side effect, the gained expertise is used to advise local construction companies that have no experience with green construction. A positive side effect which was not planned by Skanska.

High cooperation within and between units and business streams facilitates innovation and knowledge transfer. Moreover, Skanska works together intensively with customers and other value chain partners (around 100,000) in all Skanska markets (Carlén-Johansson, 2016). This action is in line with RDT as it reduces uncertainty and strengthens interfirm relationships. Additionally, each business unit has an environmental team that provides advice and professional support. Finally, Skanska is engaged in several international and national organizations to exchange knowledge and collaborate on future technologies, e.g. European Network of Construction Companies for Research and Development.

According to Elizabeth Heider, Chief Sustainability Officer for Skanska USA Inc., education of staff is one of the most successful drivers to becoming a green leader. On one side, it is important to develop awareness of practical opportunities to improve energy efficiency in the workplace, at home, and while commuting. On the other side, the workforce gets training in areas such as eco-design, LEED certification, energy modeling, and life cycle costing. This effect is fostered by a management that is highly committed to green and sustainable development.

Clark Construction is a building and civil construction firm in the United States with a strong emphasis on community values. Apart from high safety standards, they have been at the forefront of new technologies and evolving building trends. They started to deal with green buildings around 10–12 years ago, when LEED and other certification schemes started to become more prominent. While a sustainability strategy is still not included in the corporate strategy, a process manual provides guidance for all employees. In intensive communication with architects and clients, they always pursue the surpassing of legal requirements and being prepared for the future, while reducing environmental impacts. A sustainability department was created that supports the day to day work of other departments regarding certification, green building trends, and resource use. Moreover, they collect and cultivate best practices and include these ideas in new projects. To be up to date and collaborate with suppliers, Clark Construction is a member of several national and regional networks. Thereby, they are in line with the RDT, as they are very active regarding resource use and the exchange of material and information with the environment. Finally, they developed a handbook on sustainable issues that should be considered in every project. Apart from the external sustainability issues, internal processes are also reviewed regarding ecological and social impacts. According to Chip Hastie, Senior Vice President – Operations, passionate employees are the most important assets in the transformation of a conservative company into a green and innovative company. Once this internal transformation has taken place, green products and external sustainability are just a matter of time.

Southern Development Homes is a regional construction company offering EcoSmart homes with high comfort, energy efficiency, healthy air, and superior durability. Moreover, they are recycling the construction waste at a local facility that they helped to create. The decision to offer green products and housing was made around 12 years ago when consumer demand on these issues rose and green construction became more important.

To ensure knowledge transfer within the company, an IT database was installed in which every building was entered, including individual customer requests. Four times a year, these entries are evaluated to analyze customers’ preferences and new innovative concepts established in the community. Additionally, the staff is present in regional networks, e.g. the Blue Ridge Home Builders Association, and national exhibitions where they get in contact with competitors and suppliers and discuss current trends and barriers in the construction industry.

All examples demonstrate solutions and tools presented in the previous section and thus support the concept of the virtuous circle developed in this article. Moreover, the best practices show what first steps in the direction of a green leader on the international, national, and regional level look like.

ConclusionThe article presents solutions for the theoretical transformation of an inert sector, in this case the construction industry, into a green and innovative sector. First, a virtuous circle which greens the industry is designed. Second, a detailed discussion of each step is presented. Afterwards, barriers and practical implications for a green construction industry are analyzed. Finally, three case studies present best cases for determining what innovative companies are.

Results, based on surveys and expert interviews, have shown that higher first costs, outdated accounting methods, and complex projects are perceived as the largest barriers. Noteworthy solutions to these barriers are, first, raising awareness, as real cost data contradicts the assumption of high costs of green real estate projects. Second, large construction companies have to appreciate the financial and environmental benefits of green real estate projects and the market advantages of being a green leader. Finally, investors should acknowledge that rents and occupancy rates of green projects are higher than those of comparable properties. This supports the creation of a business model based on green technologies that shapes the real estate market in the coming years. The designed virtuous circle accelerates this process and prepares the sector for a sustainable and innovative friendly future.

The practical implications and the investigation of the green leaders studied in the case studies support RDT. The results show the relevance of RDT in explaining current trends in the construction industry and the importance of the external environment on companies.

Although the findings are supported by literature and expert interviews, they are based on a qualitative study. The topic could be elaborated by further case studies and by additional quantitative research that backs the presented findings, thereby enhancing the internal validity, generalizability, and theoretical level of the results. Most implications and examples in the case studies are related to RDT. However, effects of the external environment, e.g. extreme weather events, might have an influence on the use of innovative material as well. Future research should investigate that relationship and its impact on the financial performance. Moreover, water efficiency emerged as an increasingly important topic (Turner Co, 2014). Future research should concentrate on the importance of water efficiency for green buildings and its impact on the triple bottom line.

By identifying crucial barriers for a green transition and pointing out further research, the article adds value to the scientific discussion regarding the relationship between business (in this case the construction industry), GPI, and CFP. Moreover, it connects findings from expert interviews and case studies and thus provides a base for future quantitative research.

Practical implications include examples on how construction companies can expand their green product line and thereby improve financial performance. Additionally, the article identifies barriers and practical implications for the greening process and thus facilitates the entrance to green construction and internal decision-making. The findings will guide construction companies on their way to becoming green and demonstrate how to optimize their innovation process. Finally, the barriers provide starting points for governments to adjust legislation and regulation if more green construction is desired. If all the barriers and their solutions are heeded, the construction industry has the potential to become a leading green sector and will have a larger impact on the ability of future generations to meet their own needs.

The author thanks the German Federal Ministry of Education and Research for funding the program “Twenty20 – Partnership for Innovation” and the entailed project “Carbon Concrete Composite”. Moreover, the author thanks Gerardo González Martín for the valuable feedback on a first version of this article.

Im vorliegenden Projekt wird das Risikomanagement bei der Projektentwicklung von Immobilien untersucht. Die identifizierten Risiken werden anschließend in einer stochastischen Discounted Cash Flow Berechnung verwendet. Ziel ist es, den optimalen Cash Flow sowohl für konventionelle als auch für innovative Materialien zu berechnen und außerdem damit verbundene Unsicherheiten zu visualisieren.

Konventionelle Materialen werden in diesem Zusammenhang als Standardmaterialien definiert, die bereits seit mehreren Jahren/Jahrzenten Anwendung finden und zum günstigsten Preis zu haben sind. Hierfür existieren Normen sowie Prüf- und Vorsorgestrategien.

Unter innovativen und langlebigen Materialien werden dagegen Materialien mit geringeren Umweltauswirkungen verstanden, die bisher nur selten im Baubereich Anwendung finden. Diese Materialien weisen außerdem eine höhere Nutzungs- und Lebensdauer (z.B. Carbonbeton) auf und lassen sich einfacher recyceln oder entsorgen.

- 1)

Definitionen

- a)

Haben Sie noch Ergänzungen oder Anregungen zu den Definitionen von konventionellen bzw. innovativen Materialien?

- a)

- 2)

Einsatz der Materialien

- a)

Wie schätzen Sie die aktuelle Verwendung von konventionellen und innovativen, langlebigen Materialien in Deutschland ein?

- b)

Wie schätzen Sie die aktuelle Verwendung von konventionellen und innovativen, langlebigen Materialien in Ihren Projekten ein?

- a)

- 3)

Verwendung konventioneller Materialien

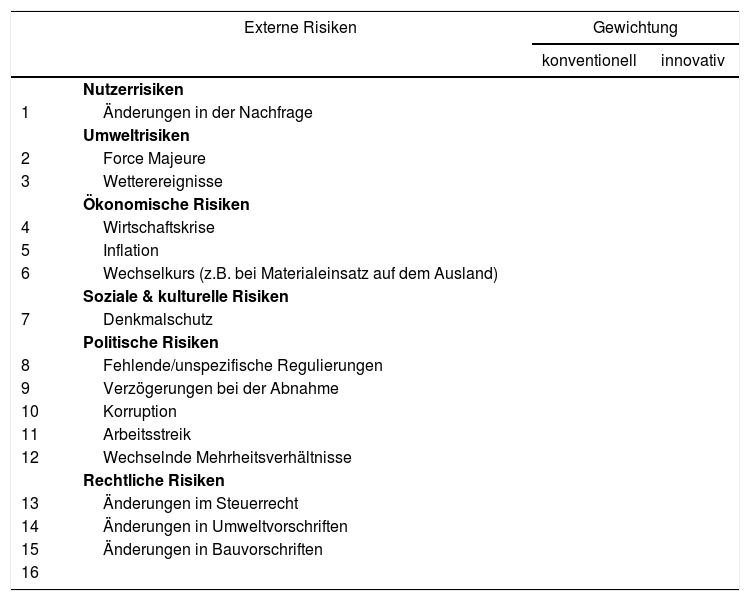

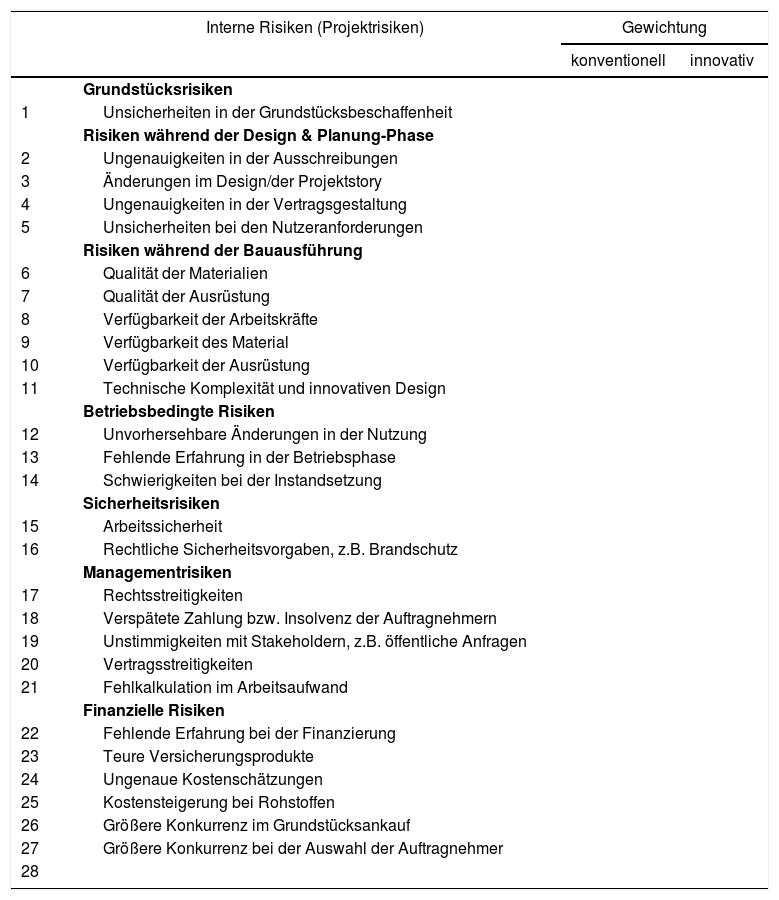

Bitte sehen Sie sich in den folgenden Tabellen die von uns identifizierten externen und internen Risiken an. Fügen Sie anschließend fehlende Risikoklassen hinzu.

Bitte gewichten Sie danach jeweils die 10 wichtigsten externen und internen Risiken, bei der Verwendung konventioneller Materialien und innovativer Materialien, von 1 (geringes Risiko) bis 10 (hohes Risiko) in der rechten Spalte. Nutzen Sie dabei auch die von Ihnen hinzugefügten Risiken!

Externe Risiken Gewichtung konventionell innovativ Nutzerrisiken 1 Änderungen in der Nachfrage Umweltrisiken 2 Force Majeure 3 Wetterereignisse Ökonomische Risiken 4 Wirtschaftskrise 5 Inflation 6 Wechselkurs (z.B. bei Materialeinsatz auf dem Ausland) Soziale & kulturelle Risiken 7 Denkmalschutz Politische Risiken 8 Fehlende/unspezifische Regulierungen 9 Verzögerungen bei der Abnahme 10 Korruption 11 Arbeitsstreik 12 Wechselnde Mehrheitsverhältnisse Rechtliche Risiken 13 Änderungen im Steuerrecht 14 Änderungen in Umweltvorschriften 15 Änderungen in Bauvorschriften 16 Interne Risiken (Projektrisiken) Gewichtung konventionell innovativ Grundstücksrisiken 1 Unsicherheiten in der Grundstücksbeschaffenheit Risiken während der Design & Planung-Phase 2 Ungenauigkeiten in der Ausschreibungen 3 Änderungen im Design/der Projektstory 4 Ungenauigkeiten in der Vertragsgestaltung 5 Unsicherheiten bei den Nutzeranforderungen Risiken während der Bauausführung 6 Qualität der Materialien 7 Qualität der Ausrüstung 8 Verfügbarkeit der Arbeitskräfte 9 Verfügbarkeit des Material 10 Verfügbarkeit der Ausrüstung 11 Technische Komplexität und innovativen Design Betriebsbedingte Risiken 12 Unvorhersehbare Änderungen in der Nutzung 13 Fehlende Erfahrung in der Betriebsphase 14 Schwierigkeiten bei der Instandsetzung Sicherheitsrisiken 15 Arbeitssicherheit 16 Rechtliche Sicherheitsvorgaben, z.B. Brandschutz Managementrisiken 17 Rechtsstreitigkeiten 18 Verspätete Zahlung bzw. Insolvenz der Auftragnehmern 19 Unstimmigkeiten mit Stakeholdern, z.B. öffentliche Anfragen 20 Vertragsstreitigkeiten 21 Fehlkalkulation im Arbeitsaufwand Finanzielle Risiken 22 Fehlende Erfahrung bei der Finanzierung 23 Teure Versicherungsprodukte 24 Ungenaue Kostenschätzungen 25 Kostensteigerung bei Rohstoffen 26 Größere Konkurrenz im Grundstücksankauf 27 Größere Konkurrenz bei der Auswahl der Auftragnehmer 28 - 4)

Entwicklung grüner Bauwerke

Sind Sie der Meinung, dass die expansive Geldpolitik und daraus folgende niedrige Zinsen die Entwicklung nachhaltiger Immobilienprojekte beschleunigt?

- 5)

Abschluss

Vielen Dank für das Gespräch und Ihre Einschätzung zum Thema Risikomanagement bei der Bewertung konventioneller und nachhaltiger Immobilien!

- a)

Wie viele Mitarbeiter arbeiten in Ihr Unternehmensbereich?

- b)

Welchen Umsatz hatte Ihr Unternehmensbereich ungefähr im vergangenen Geschäftsjahr?

- c)

Können Sie uns weitere Experten empfehlen, die wir in unserer Befragung mit aufnehmen sollten?

- a)

Dear [company],

As mentioned in the email, we are currently investigating the sustainability strategy of green construction companies. While those companies serve as best cases, they are of high importance for science and practice as they help to alleviate the transition into a sustainable future.

I would like to conduct an interview with you in order to deepen the understanding of the strategic decisions regarding the application of green materials and products at [company]. We hypothesize that large revenues in green real estate projects increase innovativeness and thus profit and market share, leading to positive long-term corporate financial performance. The three main objectives are:

- •

the motivation of [company] to deal with green real estate projects

- •

how sustainability is integrated in the corporate strategy

- •

the barriers that were/are connected to green real estate projects

Patrick Ilg, M.Sc.

PhD student at Technische Universität Dresden

Visiting Scholar at University of Virginia

Questions about the virtuous circle:

- a)

What is your opinion about the virtuous circle we designed?

- •

Does it work?

- •

Are there mistakes/fallacies?

- •

How can a virtuous circle be started?

- •

E.g. by a green building barometer?

- •

…

- •

- b)

What are barriers of the virtuous circle?

- c)

What are drivers of the virtuous circle?

Questions on going green

- a)

What is the motivation of [company] to increase the share of green real estate projects?

- b)

How is sustainability/greening incorporated in the corporate strategy?

- c)

How important are certifications, e.g. LEED, for green projects?

- d)

Were new materials or products developed in the context of this green strategy?

- e)

What were the barriers connected to the implementation of this green strategy?

- f)

How are project innovations, e.g. in green projects, transferred to corporate innovation and thus applied to other projects?

- g)

Did you collaborated with other/new partners or competitors in order to share and create the green strategy?

- h)

When where first results of the new strategy visible, e.g. in number of projects, market share, and profit?

- i)

How is the gained money reinvested?

Thank you very much for the interview and your viewpoints on the topic of green real estate projects!

Patrick Ilg, M.Sc.

PhD student at Technische Universität Dresden

Visiting Scholar at University of Virginia