The purpose of this paper is to examine the relationship among organisational unlearning, human capital and firm performance. In doing so, this paper comprehensively reviewed the literature on the unlearning concept, and developed and validated a model to measure unlearning in 112 companies listed on the Spanish Stock Exchange. The methodology involved the construction and analysis of a structural model using both subjective and objective criteria in our measurement variables, developed from a relevant literature review. Our findings show that managers need to develop an unlearning context process to create human capital, which is a primordial asset to improve firm performance.

Human capital can be defined as the stock of competencies, knowledge, social and personality attributes, including creativity, embodied in the ability to perform human labour so as to produce economic value (Bogdanowicz & Bailey, 2002). Human capital has been recognised as a key factor for maintaining company's positions and its improvement is linked to improved performance in both financial and non-financial dimensions (Cheng, Lin, Hsiao, & Lin, 2010). As Unger, Rauch, and Frese (2011) indicated, human capital increases employees’ capabilities of discovering and exploiting business opportunities, and such knowledge helps organisational members to identify and acquire other useful beneficial resources, such as related knowledge.

As talents, skills, abilities or experiences accumulate over the years, organisational members become so complacent in what they know that they barely learn anything new (Nystrom & Starbuck, 1984). However, in order to survive in an increasingly turbulent environment, such as the Spanish Stock Exchange sector (most studied companies were financial institutions and were more adversely affected by the economic crisis than others), organisations need to ‘unlearn’, or rule out, old knowledge or routines to make way for new ones (Hedberg, 1981; Tsang & Zahra, 2008). This study posits that an organisational unlearning context is necessary in order to develop and exploit employees’ capabilities and knowledge; i.e., create human capital and thus improve firm performance.

The success of creating an effective human capital depends on organisational unlearning because gaining new knowledge requires abandoning obsolete values or behaviours (e.g. Becker, Hyland, & Acutt, 2006; Becker, 2008; Becker, 2010). By way of example, when being promoted to higher positions, organisational members are asked to put aside the technical skills that were useful for previous situations, but are ineffective in a higher position. This suggests that one of the key factors that affects the extent and quality of a company's human capital is the degree to which it effectively updates knowledge structures.

Developing human capital, i.e. the knowledge, skills and abilities contained individually and collectively in the firm's human resources, directly influences performance outcomes (Buller & McEvoy, 2012). In a study of large Spanish firms, Lopez-Cabrales, Valle and Herrero (2006) found that valuable and unique core employees (i.e., those with firm-specific knowledge, skills, and abilities) were positively associated with the firm's competitiveness and efficiency.

The purpose of this paper is to examine the relationship that links organisational unlearning, human capital effectiveness and firm performance. To this end, our study addresses the following questions: What is the nature and strength of the relationship between the existence of an organisational unlearning context and human capital?” and “What is the nature and strength of the relationship between the existence of human capital and firm performance? These relationships are examined by empirically investigating 112 companies listed on the Spanish Stock Exchange. The theoretical framework is proposed in the next section. Details of the survey used to collect appropriate data to test the model are presented in Section 3 and the results of testing the model are shown in Section 4. Finally, the discussion is presented in Section 5.

2The conceptual frameworkUnlearning is a process that happens when people need to update knowledge structures (e.g. routines, processes or protocols) which have become outdated with time. It is similar to what happens to someone when (s)he buys a new coat and needs to make room for it inside his/her crammed wardrobe. When this happens, getting rid of unwanted stuff could be a prior step. Unlearning can be operationalised through three processes and one context (Cegarra & Dewhurst, 2006). Although each person can unlearn in a different way, researchers (e.g. Becker, 2010; Cegarra, Wensley, & Sanchez, 2014) have suggested that unlearning can be operationalised though three different processes: (1) awareness is the process by which someone becomes aware of outdated rules, routines or processes. This can be done by identifying his/her own mistakes or errors; (2) relinquishing allows people to stop remaking the same old mistakes, especially when they happen unwillingly; (3) relearning involves being able to learn new things, while someone is doing something new (e.g. a new routine); in fact (s)he is unlearning and putting aside what is old.

The problem with unlearning is that you cannot measure it (e.g. Howells & Scholderer, 2015). One of the rules of management is, if you cannot measure it, you cannot do it. The best way to address this problem is by an organisational unlearning context (hereafter OU context). As Azmi (2008) noted, an unlearning context can be embedded in the organisational structure by creating and supporting a culture in which people consciously acquire new skills and knowledge at the same time as they create both the time and opportunity to examine and explore existing and new knowledge.

Bringing unlearning into a context enables organisation to identify mistakes, errors or partial truths that may need to be put aside or ignored. For instance, when managers learn from their own mistakes and modify their decision-making patterns, they are ignoring their wrong or old patterns (Zhao, Lu, & Wang, 2013). In line with this, Cepeda, Cegarra, and Leal (2012, p. 1552) argue that “replacement of old knowledge could be essential for organisations which wish to create new products or services that require new points of view and ideas.” Therefore, organisational unlearning helps prepare the necessary groundwork to acquire and generate new knowledge (Wang, Lu, Zhao, Gong, & Bai, 2013).

2.1The effect of organisational unlearning on human capitalHuman capital refers to the (explicit or tacit) knowledge that individuals and teams have and is useful for the company, and to its ability to regenerate; that is, their capacity to learn (Bueno, 1998). Knowledge can be found in organisations in either a tacit or explicit form: (1) tacit knowledge: knowledge that is inimitable, valuable, underutilised, unarticulated, and lies in employees’ brains; (2) explicit knowledge: knowledge that is distributable, easy to handle, documentable and storable (Suppiah & Singh, 2011).

In order to enable inaccurate knowledge to be identified and replaced with new or modified knowledge, an OU context is necessary (Ortega, Cegarra, Cepeda, & Leal, 2015; Wensley & Cegarra, 2015). In this paper, we followed the suggestion of Cegarra and Sánchez (2008) by considering that an OU context requires the presence of three subdimensions: (1) an examination of lens fitting (ELF): this refers to a disrupting employees’ habitual state of comfort to raise awareness of new insights; (2) a framework to change individual habits (CIH): this refers to the challenge of inhibiting bad habits and inappropriate values when an individual has not only understood the new idea, but is quite encouraged to make the change; (3) a framework for consolidating emergent understandings (CEU): this refers to the organisation process that can free employees from applying their talents by implementing new ways of thinking based on adaptation to new knowledge structures.

According to Cepeda, Leal, Ortega, and Leal (2015), by means of the OU context, companies enable individuals to fit their thought patterns and the nature of the beliefs shared in order to break away from the modern workplace culture. As inappropriate and obsolete knowledge can hinder adaptation to new settings, managers need to create a continuous unlearning context. In this way, employees can unlearn outdated knowledge and be able to relearn and develop updated knowledge. So employees must have the ability to unlearn in order to learn something new (Durst & Edvardsson, 2012), which is the fundamental key for real learning that lie in reviewing and removing old habits and routines that are no longer suitable for the company (Grant, 1991).

It should be noted that, according to Nevis, DiBella, and Gould (1995), organisational learning is divided into three phases: acquisition, distribution and use of knowledge. Knowledge acquisition requires constant attempts and continual experimentation by all the employees of the organisation. When an employee acquires knowledge, the company has to promote the distribution of this knowledge among the other organisation members. This distribution consists in transmitting the acquired knowledge at an individual level, principally through individual dialogues, conversations and interrelations among the employees of the organisation, which are encouraged by managers (Kofman & Senge, 1993). Finally, in the knowledge use phase, individuals integrate aspects of knowledge that are not usual for them through shared understanding and coordinated decision making. Not only is knowledge acquisition important, but also the firm has to have up-to-date databases and processes in order to unlearn obsolete habits and routines.

On the basis of above ideas, companies must adopt different strategies in order to remove obsolete knowledge and to build new organisational knowledge by exploiting employees’ knowledge. The organisational learning literature states that organisational knowledge originates from an individual level (Birasnav, 2014). So people must consider the internal processes, such as reflection, intuition or interpretation, that are needed to satisfy workers if companies wish the desired exchange views and opinions that facilitate human capital creation to occur (Fornell, 2000). Consequently, the OU context contributes by preparing the ground for updating knowledge and knowledge structures (Wensley & Cegarra, 2015). Therefore, as employees learn and share knowledge with other employees, human capital is created and organisational learning emerges.

The above considerations led us to formulate the first hypothesis of our study:H1 The extent to which a company achieves an unlearning knowledge context will be positively associated with the extent to which human capital is created.

The question to consider now is whether human capital directly affects firm performance. About this matter, the relevant literature stresses that human capital is a fundamental and inimitable significant resource that helps companies maintain their competitive advantage (Chowdhury, Schulz, Milner, & Van De Voort, 2014). As a result of globalisation and technological advances, markets are becoming increasingly competitive, which is why companies need to improve the quality of their knowledge if they want to survive. It can be affirmed that knowledge has become one of the critical drivers for companies to succeed (Wong, 2005). Therefore, the human capital that consists of knowledge, capabilities and skills accumulated by employees through education, learning and experience can be considered an essential contributor to a company's skills (Chena & Huang, 2009). For instance, employees who are better able to acquire specific or general skills may have more career opportunities, better job security and stronger employability. Furthermore, they may be more motivated in their job and change their attitudes and behaviours. According to Boselie, Dietz, and Boon (2005), ‘better’ employee attitudes and behaviours contribute to deliver improved internal performance (i.e. through increased productivity and quality) and to achieve improved financial performance.

Considering these perspectives, one can argue that in order to be competitive and productive, it is absolutely necessary to share knowledge within the organisation (Suppiah & Singh, 2011). As Cepeda, Cegarra, Martinez, and Eldridge (2011) pointed out, companies must be able to renovate their knowledge bases to hold up quality in today's challenging environment. Consequently, new and renewed knowledge is essential to improve business performance and to enhance competitive advantages (March, 1991).

Several studies assert that a relationship exists between the knowledge created by individuals and business performance (Vijande, Pérez, González, & Casielles, 2005). As Zhao et al. (2013) noted, the emergence of new knowledge leads to changes in knowledge structures by creating new routines that can help them to improve their skills and performance. Therefore, managers must support new and renewed knowledge by encouraging employees to share their knowledge with other employees. In this way, they contribute to both update human capital and the goal of improving organisational performance (Birasnav, 2014).

The above considerations led us to put forward the second hypothesis of our study:H2 The extent to which a company develops human capital will be positively associated with the extent to which firm performance is achieved.

Fig. 1 illustrates our model:

3Method3.1Data collection

Like other studies in this domain, the present study was designed to cover a wide range of industries, but excludes the agricultural and construction sectors because the main outputs in these sectors are tangible and deliverable, while “information and knowledge” are the most important outputs in the Spanish Stock Exchange sector. It should also be noted that the sector of these companies is larger in size, has higher productivity, creates stable and qualified jobs, and their relative level of investment is also higher, especially for R&D (BME, 2015). We identified 360 companies from the SABI (Sistema de Análisis de Balances Ibéricos) database and invited them to participate in the study, of which 121 companies agreed. Each company was also informed by telephone of the research objectives and were assured that their data would be processed confidentially and anonymously. Surveys were administered over 2-month period, from October 2012 to November 2012. One hundred and twelve valid completed questionnaires were collected, which represents a response rate of 33.61% of the total number of companies invited to participate, with a factor of error of 7.7% for p=q=50% and a reliability level of 95.5%. We note that the response rate exceeds the typical 10–25 percent rate that has been proposed as the average response rate for surveys that involve senior management (Menon, Bharadwaj, & Howell, 1996). The responding companies were compared with those that did not respond in size and performance terms. No significant differences were found between these two groups, which suggests that there was no non-response bias.

3.2MeasuresThe literature review identified measures for each construct that account for validation. Churchill's (1979) approach to questionnaire development was followed by combining scales from several other relevant empirical studies with new items to make an initial list of 21 items. Several items were modified through interviews with colleagues and a first draft of the questionnaire was tested with three companies. The questionnaire constructs were operationalised and measured as follows (see Appendix for a list of items):

- (a)

The intentional unlearning context is assessed through items about lens fitting, changing individual habits and consolidating emergent understandings as three reflective dimensions (Cepeda, Cegarra, & Jiménez, 2012). The 7-point Likert scale from Cegarra and Sánchez (2008) was used for item measurements. Five items were about measuring lens fitting. These items recognise the support of policies, rules, reporting, structures and decision-making protocols that encourage problems, mistakes and new ways of performing tasks to be identified. Seven items were used to measure the framework to change individual habits. This scale focuses on employees’ self-awareness, mistakes, ways of thinking, and incorrect/inappropriate behaviours that guide everyday attitudes. Finally, six measures were used to measure the consolidation of emergent understandings. These items describe how management faces change, introduces changes into the company through projects, collaborates with other organisation members, and recognises the value of new information and risk taking.

- (b)

Human capital was measured by asking managers to evaluate different questions about three items that related to lower turnover, satisfied employees and lower absenteeism rates, which are leading indicators of the quality and effectiveness of human capital (Bueno, 1998; Dyer & Reeves, 1995).

- (c)

Firm performance was evaluated by objective criteria, which involves using two variables related to firm performance: ROI (Return On Investment) and ROE (Return On Equity) of each participating company. These data were obtained from SABI after considering the year when the survey data were collected.

The data analysis was conducted with partial least squares (PLS), a structural equations modelling (SEM) technique commonly used in the business administration literature. The choice of PLS was for the following reasons (Roldán & Sánchez, 2012): firstly, the study focus was both explanatory and predictive of the main dependent variable; secondly, the sample (n=112) was not very large; thirdly, the research model was complex according to the type of relationships included in the hypotheses and the levels of dimensionality; finally, this study used latent variable scores in the subsequent analyses of predictive relevance, particularly to implement the two-stage approach for modelling multidimensional constructs. The first step required assessing the measurement model to allow the relationships between the observable variables and theoretical concepts to be specified. This analysis was performed in relation to the attributes of individual item reliability, construct reliability, average variance extracted (AVE), and the discriminant validity of the indicators of latent variables. In the second step, the structural model was evaluated in order to test the extent to which the causal relationships specified by the proposed model were consistent with the available data. For hypothesis testing purposes, we followed the bootstrapping procedure recommended by Chin (1998). This study uses the SmartPLS v. 3.2 software (Ringle, Wende, & Becker, 2015) for measurement model and structural model analyses.

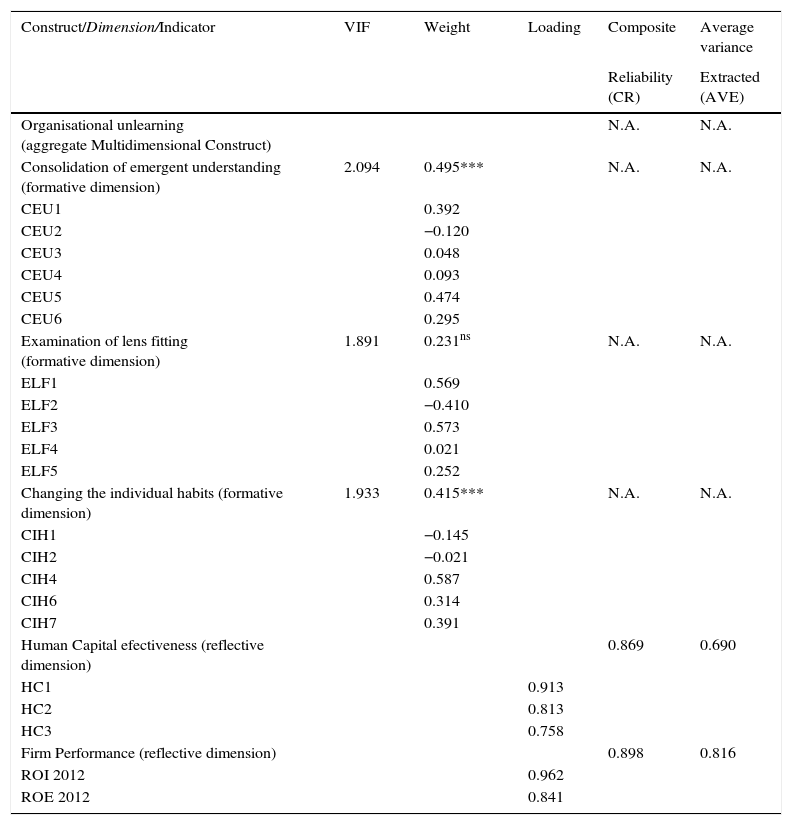

4Results4.1Measurement modelFirstly, the indicators and dimensions met the reliability and validity requirements, and the results showed that the measurement model met all the common requirements as the reflective individual items were reliable as all the standardised loadings were above 0.7 (Table 1). Consequently, individual item reliability was adequate (Carmines & Zeller, 1979). Secondly, all the reflective constructs met the construct reliability requirement as their composite reliabilities (ρc) were higher than 0.7 (Nunnally & Bernstein, 1994) (Table 1). Thirdly, these latent variables achieved convergent validity because their average extracted (AVE) surpassed the 0.5 level (Fornell & Larcker, 1981). It should be noted that the software package used to perform our data analysis was SMART PLS 3.2.4.

Measurement model.

| Construct/Dimension/Indicator | VIF | Weight | Loading | Composite | Average variance |

|---|---|---|---|---|---|

| Reliability (CR) | Extracted (AVE) | ||||

| Organisational unlearning (aggregate Multidimensional Construct) | N.A. | N.A. | |||

| Consolidation of emergent understanding (formative dimension) | 2.094 | 0.495*** | N.A. | N.A. | |

| CEU1 | 0.392 | ||||

| CEU2 | −0.120 | ||||

| CEU3 | 0.048 | ||||

| CEU4 | 0.093 | ||||

| CEU5 | 0.474 | ||||

| CEU6 | 0.295 | ||||

| Examination of lens fitting (formative dimension) | 1.891 | 0.231ns | N.A. | N.A. | |

| ELF1 | 0.569 | ||||

| ELF2 | −0.410 | ||||

| ELF3 | 0.573 | ||||

| ELF4 | 0.021 | ||||

| ELF5 | 0.252 | ||||

| Changing the individual habits (formative dimension) | 1.933 | 0.415*** | N.A. | N.A. | |

| CIH1 | −0.145 | ||||

| CIH2 | −0.021 | ||||

| CIH4 | 0.587 | ||||

| CIH6 | 0.314 | ||||

| CIH7 | 0.391 | ||||

| Human Capital efectiveness (reflective dimension) | 0.869 | 0.690 | |||

| HC1 | 0.913 | ||||

| HC2 | 0.813 | ||||

| HC3 | 0.758 | ||||

| Firm Performance (reflective dimension) | 0.898 | 0.816 | |||

| ROI 2012 | 0.962 | ||||

| ROE 2012 | 0.841 |

N.A., not applicable.

***p<0.001; ns, not significant (based on t(4999), two-tailed test).

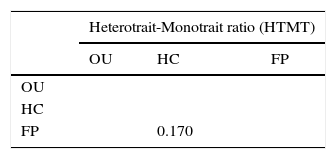

Finally, all the variables met the discriminant validity requirements. Confirmation of this validity came from an HTMT criterion reported in Table 2 which was clearly below 0.85 and provided discriminant validity (Henseler, Ringle & Sarstedt, 2015; Voorhess, Brady, Calantone & Ramirez, 2016). The evaluation of the formative measurement models at the indicator level involved test potential multicolinearity between items and weights analyses (Henseler, Ringle, & Sinkovics, 2009). The maximum variance inflation factor (VIF) values for the manifest variables that shaped the formative multidimensional construct OU were 2.09, 1.89 and 1.93, respectively, all within the acceptable threshold of 5 (Hair, Ringle, & Sarstedt, 2011) (Table 1). In this study, weights provided information about how each formative dimension contributed to the OU construct. Weights actually yielded a ranking of these dimensions according to their contribution (Henseler et al., 2009). Table 1 reveals that the framework for the consolidations of emergent understanding (0.49) and changing individual habits (0.41) were the most significant dimensions in the OU construct composition.

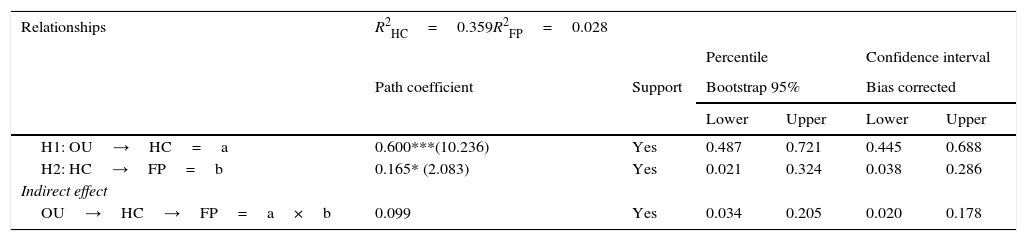

4.2Structural modelTable 3 shows the explained variance (R2) in the endogenous variables and the path coefficients for the three models under study. In a PLS analysis, the significance of the relationships among the constructs, R2, effect size f2 and Q2 are measures of how well a model performs (Chin, 1998). The structural model that resulted from the PLS analysis is summarised in Table 3. Firstly, the standardised path coefficients (β) and the associated t-values are shown. The path coefficients should be around 0.20 and ideally above 0.30 to be considered meaningful and economically significant (Chin, 1998). As observed, all the paths presented in the model were significant and were, therefore, verified. Secondly, any R2 values higher than 0.2 indicate the good explanatory power of the model's dependent variables (Chin, 2010). As observed, the model gave R2 values above HC. Thirdly, effect size f2 (e.g., 0.02, 0.15, 0.35 for weak, moderate, strong effects) is a measure that assesses the relevance of change in R2; that is, whether the impact of a specific independent variable on a dependent variable is substantive (Chin, 1998). In this study, OU→HC was 0.59 strong effects. Fourthly, the cross-validated redundancy index (Q2) has been proposed as a good index for evaluating the predictive capacity of models estimated by a PLS analysis. Q2 measures the goodness of fit with which the observed values are reconstructed by the model and its parameters (Chin, 1998). It is generally accepted that a model has predictive relevance when Q2>0 for its dependent variables. Following the blindfolding procedure, we estimated Q2 to be 0.20, which was above zero, as recommended. These values showed a more satisfactory predictive power for our model.

Structural model results.

| Relationships | R2HC=0.359R2FP=0.028 | |||||

|---|---|---|---|---|---|---|

| Percentile | Confidence interval | |||||

| Path coefficient | Support | Bootstrap 95% | Bias corrected | |||

| Lower | Upper | Lower | Upper | |||

| H1: OU→HC=a | 0.600***(10.236) | Yes | 0.487 | 0.721 | 0.445 | 0.688 |

| H2: HC→FP=b | 0.165* (2.083) | Yes | 0.021 | 0.324 | 0.038 | 0.286 |

| Indirect effect | ||||||

| OU→HC→FP=a×b | 0.099 | Yes | 0.034 | 0.205 | 0.020 | 0.178 |

Notes: OU, organisational unlearning; HC, human capital effectiveness; FP, firm performance; t values in parentheses. Bootstrapping 95% confidence intervals bias corrected in square brackets (based on n=5000 subsamples).

***p<.001; *p<.05 (based on t(4999), one-tailed test). t(0.05, 4999)=1.645; t(0.01, 4999)=2.327; t(0.001, 4999)=3.092.

Next the model (Table 3) includes the main direct paths. Model (Table 3) describes the significant effect. In this scenario, the results supported H1, which describes the direct relationship between organisational unlearning (OU) and human capital (HC) (OU→HC=0.60; t=10.23). As the direct effects were significant, this fact supports H1. Model (Table 3) describes the significant effect. In this scenario, the results support H2, which describes the direct relationship between human capital (HC) and firm performance (FP) (HC→FP=0.16; t=2.08). As the direct effects were significant, this fact supports H2.

SRMR is the square root of the sum of the squared differences between the model-implied and the empirical correlation matrix. A value of 0.058 for SRMR indicates a good fit. A recent simulation study has shown that even an entirely correctly specific model can yield SRMR values of 0.06 and higher (Henseler et al., 2014). Therefore as proposed by Hu and Bentler (1999), a cut-off value of 0.08 appears more adequate for the PLS path models.

As we can see, an indirect effect was found between organisational unlearning and firm performance through human capital (Table 3); in other words, organisational unlearning impacts not only human capital, but also indirectly impacts firm performance.

5DiscussionSince organisational unlearning is asserted and used repeatedly, without sourcing and without explaining how it differs in definition or practice from trivial ‘ask different questions’ (Howells & Scholderer, 2015), this paper aims to contribute to the understanding of the interaction that links human capital, firm performance and organisational unlearning. In this paper, the authors refer to ‘organisational unlearning’ as the process to make room for new understandings. In a turbulent changing environment like today's European context, achievement of higher performance levels requires detecting, interpreting and acting on ambiguous signals that come from outdated knowledge structures. Therefore, this organisational unlearning view is important for the ongoing debate about the importance of organisational unlearning to achieve objectives.

The main contribution of this paper is that we use both subjective and objective criteria to operationalise the model presented in Fig. 1. The subjective methods determine weights solely according to decision makers’ preferences or judgements, while the objective methods are based on mathematical computation (Wang & Lee, 2009). The use of subjective and objective criteria can avoid the subjectivity of our study, and confirm the objectivity of our results. This adds value and strength to previous studies that only used subjective measures (e.g. Becker, 2008 or Becker, 2010). Our findings also validate previous research that supports the notion that in order to increase financial performance (e.g. Cepeda, Cegarra, & Jiménez, 2012), the primary knowledge that needs to be updated is knowledge from employees. For example, by not only updating relevant client contacts and preferences, but also by other resources, such as identifying either new routines or threats and opportunities in emerging markets, and organisations will provide fresh solutions for current and potential customers.

This second contribution of our research derives from the empirical test results of the hypotheses. The findings relating to H1 demonstrates that achieved organisational unlearning has a positive effect on human capital. One possible explanation is that organisational unlearning allows individuals to adjust their mental models and the nature of the assumptions they share to break with the current workplace culture and help employees explore issues more effectively with a view to solving problems and unforeseen circumstances. If employees are able to develop their personal skills by deliberate reflection on past, present and future decisions or through conversations with their managers, they can change attitudes and thoughts and develop new knowledge. It is in this direction that managers can develop human capital if they encourage employees to transfer their knowledge to other employees and apply their knowledge to apply new solutions and ideas.

The third contribution of our research is to question the relationship between human capital and firm performance. Our findings reinforce the literature which claims that improvements in human capital development and management may lead to improved firm performance. So if the organisation considers organisational unlearning to be a prior step in creating human capital, then the companies can improve firm performance by obtaining increased ROI and ROE. Moreover, our results demonstrated that organisational unlearning indirectly affects firm performance by developing and exploiting new capabilities and skills that increase the human capital value.

According to the results obtained, and in line with other authors such as Birasnav (2014) and Jiménez-Jiménez and Sanz-Valle (2011), we suggest the following managerial implications. Managers should promote an appropriate OU context to help to forget old habits and to implement new knowledge among their employees by making them attend meetings, conferences and fairs, making them talk to one other via teamwork; making them participate in projects and perform different critical jobs; making them responsible for collecting suggestions internally. Therefore, creating human capital is provided and the company can achieve better performance.

This study has some limitations. Firstly, the sample size of 112 companies may limit the generalisability of these results to a wider population in the financial sector. Secondly, the researchers only provided a snapshot of what are, by nature, ongoing processes. Thirdly, it is impossible for a model like that presented herein to capture all the possible moderating effects of environmental turbulence and uncertainty within organisations. Thus future research should include new objective measures to complement subjective information (e.g., company size and industry sector).

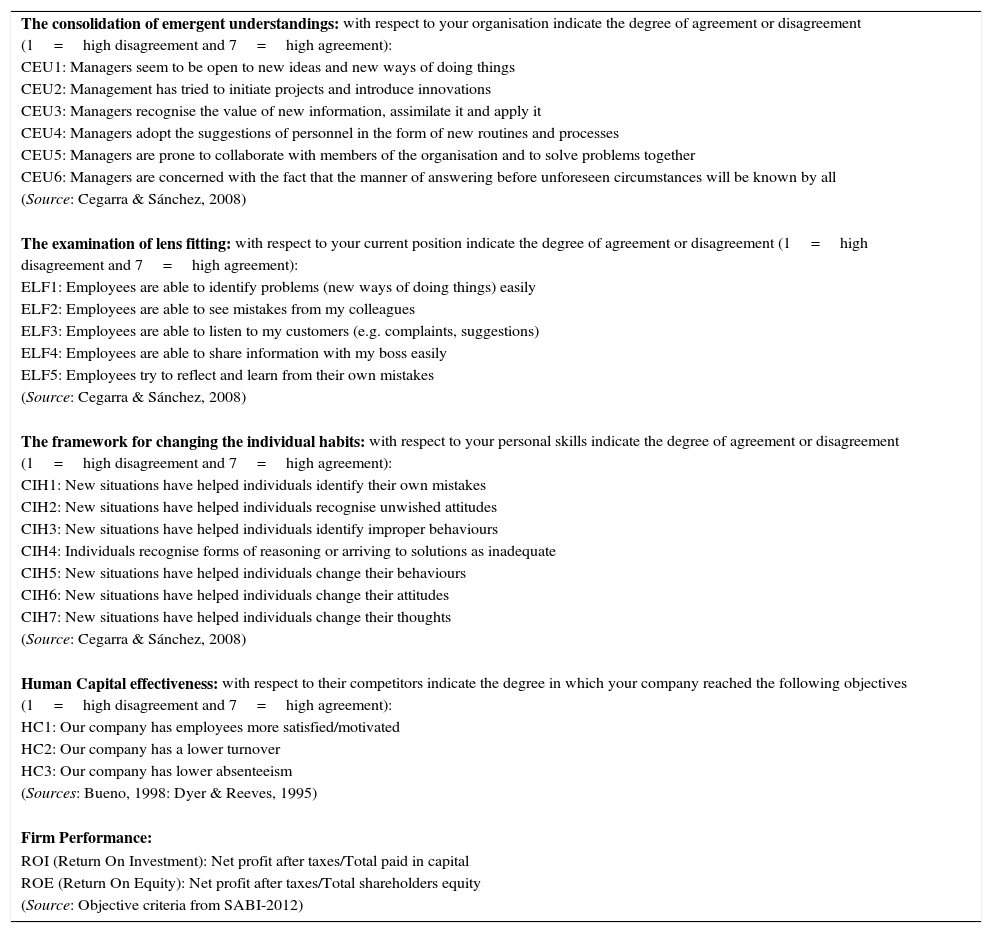

| The consolidation of emergent understandings: with respect to your organisation indicate the degree of agreement or disagreement (1=high disagreement and 7=high agreement): |

| CEU1: Managers seem to be open to new ideas and new ways of doing things |

| CEU2: Management has tried to initiate projects and introduce innovations |

| CEU3: Managers recognise the value of new information, assimilate it and apply it |

| CEU4: Managers adopt the suggestions of personnel in the form of new routines and processes |

| CEU5: Managers are prone to collaborate with members of the organisation and to solve problems together |

| CEU6: Managers are concerned with the fact that the manner of answering before unforeseen circumstances will be known by all |

| (Source: Cegarra & Sánchez, 2008) |

| The examination of lens fitting: with respect to your current position indicate the degree of agreement or disagreement (1=high disagreement and 7=high agreement): |

| ELF1: Employees are able to identify problems (new ways of doing things) easily |

| ELF2: Employees are able to see mistakes from my colleagues |

| ELF3: Employees are able to listen to my customers (e.g. complaints, suggestions) |

| ELF4: Employees are able to share information with my boss easily |

| ELF5: Employees try to reflect and learn from their own mistakes |

| (Source: Cegarra & Sánchez, 2008) |

| The framework for changing the individual habits: with respect to your personal skills indicate the degree of agreement or disagreement (1=high disagreement and 7=high agreement): |

| CIH1: New situations have helped individuals identify their own mistakes |

| CIH2: New situations have helped individuals recognise unwished attitudes |

| CIH3: New situations have helped individuals identify improper behaviours |

| CIH4: Individuals recognise forms of reasoning or arriving to solutions as inadequate |

| CIH5: New situations have helped individuals change their behaviours |

| CIH6: New situations have helped individuals change their attitudes |

| CIH7: New situations have helped individuals change their thoughts |

| (Source: Cegarra & Sánchez, 2008) |

| Human Capital effectiveness: with respect to their competitors indicate the degree in which your company reached the following objectives (1=high disagreement and 7=high agreement): |

| HC1: Our company has employees more satisfied/motivated |

| HC2: Our company has a lower turnover |

| HC3: Our company has lower absenteeism |

| (Sources: Bueno, 1998: Dyer & Reeves, 1995) |

| Firm Performance: |

| ROI (Return On Investment): Net profit after taxes/Total paid in capital |

| ROE (Return On Equity): Net profit after taxes/Total shareholders equity |

| (Source: Objective criteria from SABI-2012) |